International Studies of Consumer Adoption of E-Banking

Banks implementing e-banking services may benefit by better understanding their customers’ attitudes towards technology. If banks are successful in doing so, they may be able to positively impact and even determine consumer behavior, thereby gaining a competitive advantage.

There have been so far a significant number of discussions in the literature about the adoption process of e-banking services. The Appendix summarizes the results of such studies. These research studies utilized theory of planned behavior (TPB), theory of reasoned action (TRA), technology acceptance model (TAM), and decomposed theory of planned behavior (DTPB) to investigate the e-banking adoption construct. However, such studies have not examined any moderating effects on the relationship between perceived benefit and intention to use.A Conceptual Model for E-Banking Adoption in Vietnam

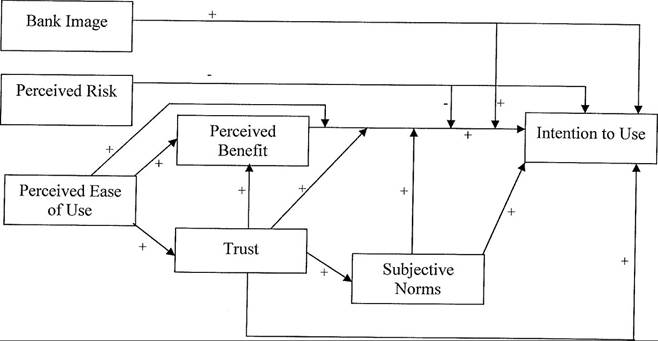

Based on an integration of the innovation theories, trust, perceived risk, bank image, and perceived benefit, a conceptual model for e-banking adoption in Vietnam is built in Figure 1.

The following are theoretical support and resulting hypotheses that elicit causal relationships postulated in the model.

Corporate image refers to the extent to which reputational knowledge of an organization has been accumulated and developed by customers. Such a reputational knowledge is rooted in the minds of the customers. Specifically, reputational knowledge can be represented by a distinctive reputation

Figure 1. A conceptual model for e-banking adoption in Vietnam

by a firm in offering products/services with very high quality (Olavarrieta and Friedmann, 1999). Gronroos (1984) argues that corporate image is very likely to make significant contributions to the development of service quality.

Image is believed to function well to overcome complexities generated by distinct attributes of service and when small problems occur from functional and technical aspects of quality. In addition, the results of a study conducted by Kang and James (2004) revealed that corporate image plays as a mediator between service quality dimensions and the overall service quality, and the overall service quality is positively related to customer loyalty.Furthermore, corporate image can be understood as customers’ affective preconceptions towards the service provider, accumulated and developed via continuous service experiences (Zins, 2001). Based on this definition, a bank image plays a vital role in the adoption of e-banking. Thus, under Vietnam’s e-banking setting, we hypothesize that:

Hypothesis 1: Bank image will have a positive direct relationship with intention to use e-banking.

An e-banking transaction is considered as a mode of trusting behavior due to the fact that customers are themselves engaging in vulnerable situations regarding such e-banking transactions. Customers are willing to utilize e-banking as long as they believe that e-banking functions well and performs what they expect it to do.

In e-settings, people from almost everywhere in the world are easily to get access to documents stored on computers and in the same vein, information is easily to be transferred through e-technologies with computer networks. That is why under the security perspective, e-banking is considered as being risky. In addition, e-banking is characterized by highly uncertain transactions since people who make such transactions very often come from different places in the world. The utilization of e-banking can be considered as a new information and communication technology and under the marketing perspective, it is also viewed as a new distribution channel technology based on which customers can easily contact with their bank. In the marketing field, a number of empirical studies have been conducted to show that perceived risk is a very important construct (Gefen, 2004).

In such studies, perceived risk is shown to have significant effects on customer loyalty. Thus, under Vietnam’s e-banking setting, we hypothesize that:Hypothesis 2: Perceived risk will have a negative direct relationship with intention to use e-banking.

Perceived benefit is, in the literature of technology acceptance, defined as an individual’s positive or negative evaluation of performing a type of behavior (Chau & Hu, 2001). Hansen et al. (2004) found a significantly positive association between perceived benefit and behavioral intention to use online shopping for groceries. Similarly, other prior research has indicated that perceived benefit has strong impacts on behavioral intention to utilize an innovation, for example, word processing software (David et al., 1989) or spreadsheet software (Mathieson, 1991). If someone has a feeling that utilizing e-banking will bring about positive outcomes, then such a person may have more intention to adopt e-banking. In contrast, if someone has a negative feeling of outcomes resulting from utilizing e-banking, he or she may have a lower adoption intention. Thus, under Vietnam’s e-banking setting, we hypothesize that:

Hypothesis 3: Perceived benefit will have a positive direct relationship with intention to use e-banking.

Subjective norms refer to the person’s perception that most people who are important to him think that he should or should not perform the behavior in question (Ajzen & Fishbein, 1980). Several theories suggest that subjective norms are important in shaping user behavior. For example, TPB suggests that subjective norms influence a person’s behavioral intention. Venkatesh and Davis (2000) explain the effect of subjective norms on behavioral intention to use in the way that potential users may choose to use the technology if the people who are important to them say that they should use it. Thus, under Vietnam’s e-banking setting, we hypothesize that:

Hypothesis 4: Subjective norms will have a positive direct relationship with intention to use e-banking.

Trust has been shown to have a mediating role in IS adoption models (Gefen et al., 2003; Ribbink et al., 2004; Chen & Dhillon, 2003; Jar- venpaa et al., 2000; Rotter, 1971). Trust plays an important role in many transactional buyer-seller relationships, especially in settings containing risks (McKnight et al., 1998). It is argued that trust serves a critical role under online business settings where it is impossible to have face-to- face interaction with staff. In general, trust can be defined as an expectation one has that others will not behave opportunistically. Alternatively, trust can be defined as one’s belief that others are going to behave in a dependable, ethical, and socially desirable manner (Rousseau et al., 1998). Moreover, trust can be conceptualized as a combination of such factors as trustworthiness, integrity, honesty, and benevolence of e-vendors that are expected to escalate behavioral intentions via reduced risks among potential but inexperienced customers (Jarvenpaa & Todd, 1996; Gefen et al., 2003). Thus, under Vietnam’s e-banking setting, we hypothesize that:

Hypothesis 5: Trust will have a positive direct relationship with intention to use e-banking.

The relationship between trust and perceived benefit has been widely discussed in a variety of contexts including online based business settings (Gefen et al., 2003; Pavlou, 2003; Saeed et al., 2003; Gefen, 2004). Specifically, trust and TAM is well integrated in the online shopping setting (Gefen et al., 2003). Such an integration showed that trust is an antecedent of perceived benefit.

Trust is contended to serve as an important determinant of perceived benefit, especially in the online environment due in part to the guarantee that consumers expect the perceived benefit from the website with the sellers behind it. Furthermore, trust is strongly believed to have positive impacts on perceived benefit on the ground that trust makes favorable conditions for consumers to be vulnerable to e-vendor to ensure that they achieve expected useful interactions and services (Pavlou, 2003).

While consumers initially trust their e-vendors and have a feeling that online service adoption is efficient to their job performance, they intend to believe that such online services are useful (Gefen et al., 2003). Thus, under Vietnam’s e-banking setting, we hypothesize that:Hypothesis 6: Trust will have a positive direct relationship with perceived benefit.

Many studies have been conducted and found that there is a strongly positive correlation between users’ and IS units’ mutual trust and mutual influence (Nelson & Cooprider, 1996). Moreover, it is elicited by Decomposed TPB that users can be influenced by their peers and superiors in determining subjective norm towards the IS utilization (Taylor & Todd, 1995). To put it another way, it is very possible that trust in peers and superiors regarding their beliefs of the IS utilization plays an important role in determining subjective norm. In a similar vein, trust in e-vendors regarding their reputation, brand name, and service might have positive impacts on subjective norm over online transactions’ behavior. Additionally, aspects of reputation, brand name, and service might elicit certain relationships between trust in peers and superiors and trust in vendors. Hence, whatever types of trust are with direct and indirect impacts on subjective norm, they are all serving as important antecedents of subjective norm in the online setting. Thus, under Vietnam’s e-banking setting, we hypothesize that:

Hypothesis 7: Trust will have a positive direct relationship with subjective norms.

The relationship between perceived ease of use and perceived benefit can be explained in the manner that if other things are equal, the easier the technology is to use, the more beneficial it can be (Venkatesh & Davis, 2000). If using the technology is easy, potential users do not have to spend too much time to learn how to use the technology; this may influence the performance of the user. Besides, TAM has verified the effects of perceived ease of use on perceived benefit (David, 1989; David et al., 1989).

Extensive research has shown significant effects of perceived ease of use on perceived benefit (e.g., Chan & Lu, 2004). Thus, under Vietnam’s e-banking setting, we hypothesize that:Hypothesis 8: Perceived ease of use will have a positive direct relationship with perceived benefit.

Perceived ease of use is, in many studies, found to have positive impacts on trust since perceived ease of use is very likely to escalate customers’ favorable impressions towards e-vendors in the online service initial adoption and lead customers to be willing to make investments and commitments in buyer-seller relationships (Gefen et al., 2003). Under the view of social cognitive theory, perceived ease of use is strongly contended to have positive impacts on an individual’s favorable outcome expectation towards an innovative technology adoption (Bandura, 1986). Such a contention is based on the fact that cognition-based trust, as mentioned above, is primarily constructed on the first impression of the individual towards a certain behavior. Specifically, perceived ease of use under the online service setting is viewed as the first feeling or expectation set up for continued online transactions. Thus, under Vietnam’s e-banking setting, we hypothesize that:

Hypothesis 9: Perceived ease of use will have a positive direct relationship with trust.

Theories of reasoned action (TRA) and planned behavior (TPB) and their derivatives have been utilized to predict possible adoption of information technology (Benbasat and Barki, 2007). While such studies have escalated our understanding of how the theories’ main contructs have effects on IT adoption, they ignore nonlinear relationships among the constructs. The fact that ignoring the nonlinear effects is very likely to either understate or overstate the main effects which might lead to erroneous, partial, or incomplete interpretations (Ping, 2002). That is the reason Ping (2002) strongly argue that investigating complicated and contingent relationships among the main constructs will bring about finer grained knowledge about determinants of individual IT adoption. Thus, under Vietnam’s e-banking setting, we hypothesize that:

Hypothesis 10: The relationship between perceived benefit and intention to use e-banking will be positively moderated by perceived ease of use.

Hypothesis 11: The relationship between perceived benefit and intention to use e-banking will be positively moderated by trust.

Hypothesis 12: The relationship between perceived benefit and intention to use e-banking will be positively moderated by subjective norm.

Hypothesis 13: The relationship between perceived benefit and intention to use e-banking will be negatively moderated by perceived risk.

Hypothesis 14: The relationship between perceived benefit and intention to use e-banking will be positively moderated by bank image.