PRO FORMA FINANCIAL STATEMENTS

Another way that the analyst can look forward with financial statements is to construct pro forma statements that reflect significant developments, prior to reflection of those developments in subsequent published statements.

It is unwise to base an investment decision on historical statements that antedate a major financial change such as a stock repurchase, writeoff, acquisition, or divestment. By the same token, it can be important to determine quickly whether news that flashes across the screen will have a material effect on a company’s financial condition. For example, will a just- announced repurchase of 3.5 million shares materially increase financial leverage? To answer the question, the analyst must adjust the latest balance sheet available, reducing shareholders’ equity by the product of 3.5 million and an assumed purchase price per share, then reduce cash or increase debt as the accounting offset.Pro Forma Statements for Divestments

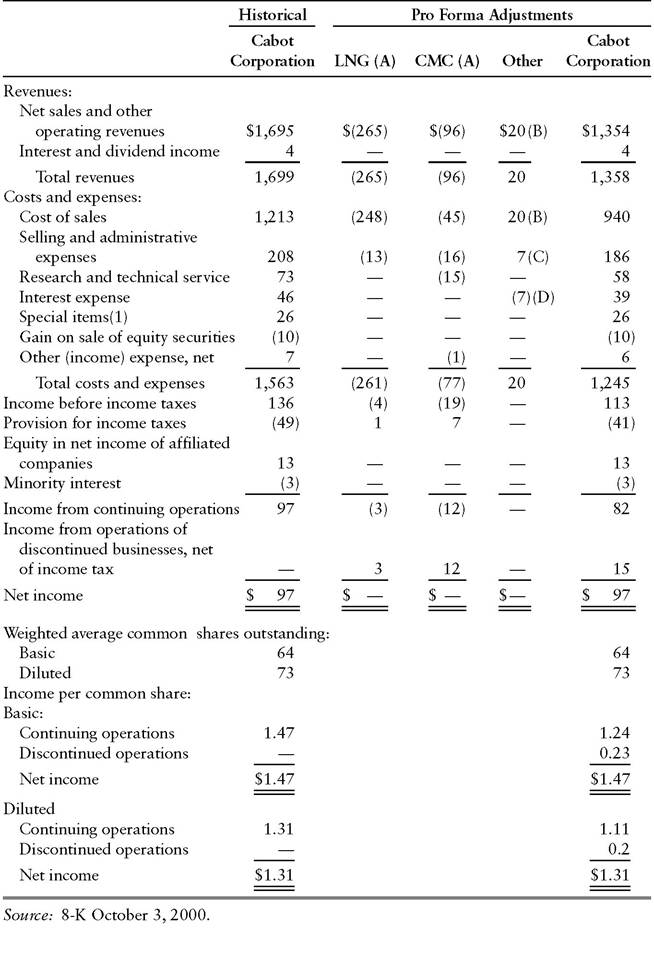

Exhibit 12.15 presents a pro forma income statement dealing with a more complex set of circumstances. As detailed in Exhibit 12.16, on September 13, 2000, specialty chemical producer Cabot Corporation spun off its

Unaudited Pro Forma Consolidated Statement of Income for the Year Ended September 30, 1999 (in millions, except per Share Data) (Unaudited)

EXHIBIT 12.16 Cabot Corporation Details of Divestments

Sale of Liquefied Natural Gas Business

On September 19, 2000, Cabot Corporation (“Cabot” or “registrant”), through a subsidiary, sold all of the outstanding shares of Cabot LNG Business Trust (“Cabot LNG”) to Tractebel, Inc.

(“Tractebel”). The agreement of sale was previously reported in Note C to the Consolidated Financial Statements and in the Management’s Discussion and Analysis of Financial Condition and Results of Operations in Cabot’s Form 10-Q for the quarter ended June 30, 2000. Cabot LNG is engaged in the liquefied natural gas (“LNG”) business. The assets of Cabot LNG included the LNG terminal in Everett, Massachusetts, the LNG tanker “Matthew,” Cabot’s equity interest in the Atlantic LNG liquefaction plant in Trinidad, and all related properties and equipment. The purchase price was $688 million in cash. The price was determined through a bidding process. There is no material relationship between Tractebel and Cabot or any of its affiliates, directors and officers or any associate of any such director or officer. A copy of the registrant’s press release dated September 19, 2000 relating to this sale is filed herewith as Exhibit 99.1. A copy of the Stock Purchase and Sale Agreement, dated as of July 13, 2000, by and among Cabot Business Trust, Cabot Corporation, Tractebel, Inc. and Tractebel, S.A. is filed herewith as Exhibit 2 and is made a part hereof. Registrant agrees to furnish supplementally a copy of any omitted schedule to the Commission upon request.Spin-Off of Cabot Microelectronics Corporation Stock

As previously reported in registrant’s Form 8-K dated September 14, 2000, on June 25, 2000 a committee of the Board of Directors of Cabot voted to spin-off its remaining 80.5% equity interest in Cabot Microelectronics Corporation (“CMC”) by distributing a special dividend of its equity interest in CMC to Cabot’s shareholders of record as of 5:00 p.m., Eastern time, on September 13, 2000. Cabot owned 18,989,744 shares of common stock of CMC on the September 13, 2000 record date. The tax-free distribution took place on September 29, 2000. The basis for the distribution to Cabot’s shareholders was approximately 0.280473721 shares of CMC common stock for each share of Cabot common stock owned.

Fractional shares were not distributed, but were to be sold and the net proceeds distributed to Cabot shareholders on a pro rata basis. A copy of the registrant’s press release dated October 2, 2000 relating to this spin-off is filed herewith as Exhibit 99.2.remaining 80.5% equity interest in Cabot Microelectronics (CMC), a producer of compounds used to polish semiconductors. Cabot implemented the spin-off by distributing its equity interest as a special dividend to its shareholders. Separately, on September 19, 2000, Cabot sold all outstanding shares of its liquefied natural gas (LNG) business to Tractebel, Inc. for $688 million in cash. By making pro forma adjustments to its fiscal 1999 income statement, Cabot gives analysts a basis from which they can project the performance of the businesses that constitute the ongoing company.

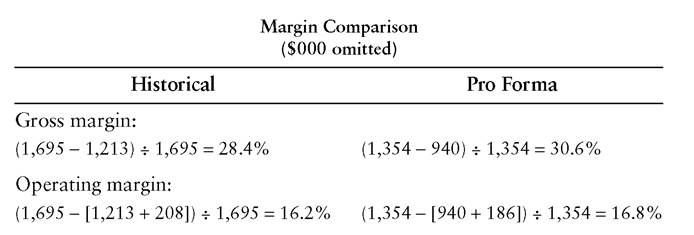

In principle, the pro forma adjustments are straightforward. If Cabot had not owned LNG and CMC during fiscal 1999, its sales would have been lower by $265 million + $96 million = $361 million, less $20 million of intercompany sales,2 for a net reduction of $341 million. Similar adjustments isolate the costs and expenses attributable to continuing operations from those being shed by Cabot. The pro forma statement enables analysts to make several useful observations. For example, they can infer that the stripped-down Cabot will have a higher gross margin and operating margin than its more widely diversified forerunner, as shown in the following calculations. (Note that in accordance with the formulas presented in Chapter 13, the calculations are based on net sales, rather than total revenues, which include interest and dividend income.)

Chucking low-margin operations is often the motivation for a corporation’s disposal of a business.

In the case of a spin-off, however, the goal may be to increase shareholders’ wealth by unlocking the value in a rapidly growing subsidiary that would receive a high price-earnings multiple as a stand-alone public company. Theoretically, a corporation consisting of two subsidiaries, one with high and one with low earnings growth, may be priced at a multiple that represents a blend of the multiples that the two subsidiaries would garner if they traded as separate companies. Many market participants, however, believe that the whole represents less than the sum of the parts in such situations. They therefore advocate the maneuver that Cabot used with its microelectronics business—establishing a multiple by selling a minority interest of the high-growth subsidiary in an initial public offering, then distributing the remainder to shareholders as a special dividend.In Cabot’s case, the subsequent stock performance vindicated the decision to spin off CMC. Shortly before the transaction, Cabot had a market capitalization of around $2 billion. Six months later, the combined market capitalization of Cabot and Cabot Microelectronics was $4 billion.

To be sure, several factors affected both companies’ valuations following the spin-off. The essential point for analysts, though, is that a pro forma income statement for a single year provides no information about the historical growth in sales and earnings of the subsidiary that is being spun off. To gauge the spin-off’s potential impact on aggregate market capitalization, it is important to examine as well the prospectus for the subsidiary’s initial public offering.

A pro forma income statement for one year likewise gives no information about year-to-year variability in the earnings of the operations being sold or spun off. Although the business that is being discarded may have dragged down margins in the past few years, it also may have been more stable during recessions than the rest of the company’s operations.

The new, trimmer corporation may therefore experience wider cyclical profit swings than in the past.Finally, pro forma adjustments for a divestment do not capture the potential benefits of increased management focus on the company’s core operations. The entity being disposed of may be the remnant of a long- abandoned plan to expand aggressively in a particular region or a line of business tangential to the corporation’s primary activity. By eliminating the distraction, the senior executives may be able to boost profits more substantially than the pro forma statements suggest. The pro forma adjustments simply attribute to the discarded unit a share of corporate overhead proportional to its size.

Pro Forma Statements for Acquisitions

Just as pro forma statements provide a useful basis for forecasting a company’s results following a major divestment, subject to certain caveats, they are helpful in the context of acquisitions when used judiciously. If anything, though, analysts must exercise greater care in extrapolating from an acquisition- related pro forma income statement. The effects of shedding a business are highly predictable compared with the uncertainties inherent in combining companies. Mergers of companies in the same industry often work out poorly due to clashes of corporate culture. When a corporation acquires a business in the belief that it will be complementary to its existing operations, it runs the risk of inappropriately applying its own management style to an industry with very different requirements. Moreover, the acquired company’s owners may be shrewdly selling out at top dollar, anticipating a deceleration in earnings growth that is foreseeable by industry insiders, but not to the acquiring corporation’s management. For all of these reasons, the earnings shown in a merger-related pro forma income statement may be higher than the company can sustain.

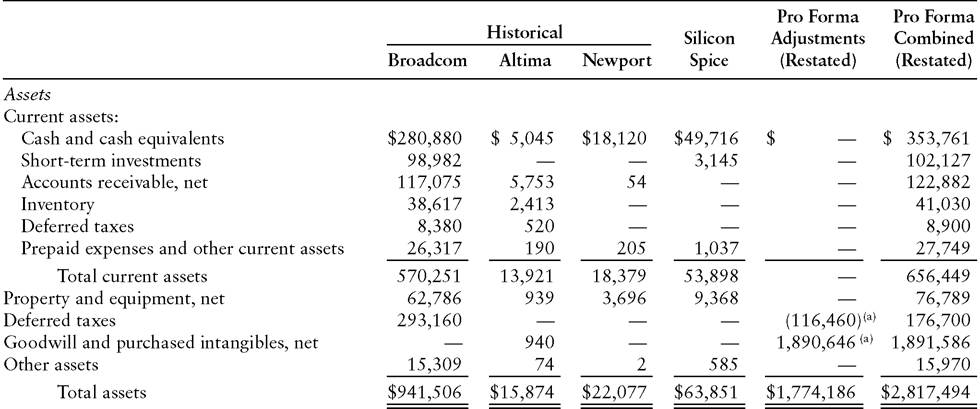

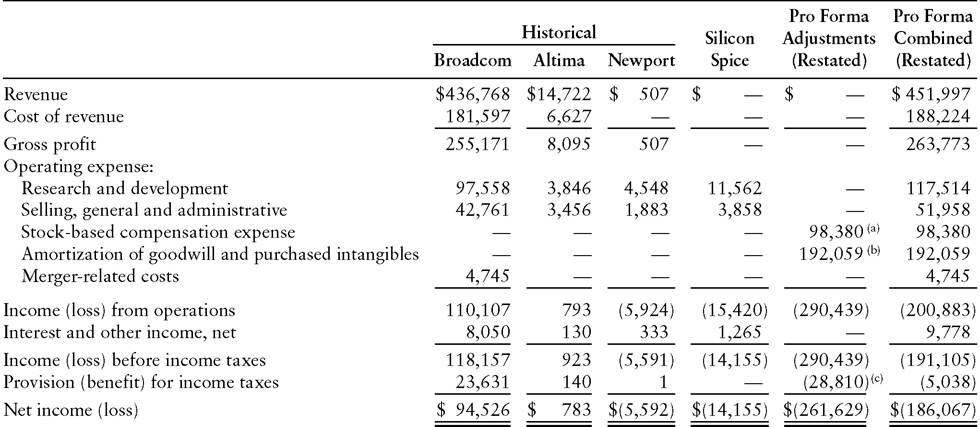

On the other hand, GAAP does not allow management to make pro forma statements reflect all of the cost savings that might be achievable in a merger. In some instances, projections that merely extrapolate from the pro forma income statement will prove too conservative.Exhibits 12.17 and 12.18 are, respectively, semiconductor manufacturer Broadcom’s balance sheet for June 30, 2000, and income statement for the six months ended June 30, 2000, with pro forma adjustments for three acquisitions completed during September-October 2000. The adjustments are explained in accompanying notes a through h.

As a result of using a combination of its own shares and stock options to acquire three companies with aggregate shareholders’ equity of $77.5 million, the shareholders’ equity on Broadcom’s balance sheet swells by $1,8378.9 million to $2,681.7 million. At the same time, the company’s long-term debt (including current portion) rises only slightly, from $2.1 million to $14.6 million. Seemingly, a company can reduce its credit risk, measured by the ratio of long-term debt to the sum of long-term debt and shareholders’ equity, by acquiring other companies for stock (see Chapter 13). According to this logic, Broadcom’s credit quality would have improved even more if instead of shelling out $2,941.2 million worth of shares and options for Altima, Newport, and Silicon Spice (this figure appears in the pro forma adjustments column of Exhibit 12.17), the company had paid $4 billion. Seemingly, a company can strengthen its balance sheet by drastically overpaying for acquisitions.

class=a7 style='text-indent:18.0pt'>The resolution of this paradox lies in the $1,891.6 million of goodwill added to Broadcom’s balance sheet through the transactions. As discussed in Chapter 2, credit analysts take a skeptical view of the debt protection afforded by intangible assets such as goodwill. Increasing the size of the intangibles by paying more than fair value in an acquisition does not, in practice, raise a company’s perceived credit quality.In fact, one aspect of the pro forma income statement (Exhibit 12.18) suggests that Broadcom has become a worse credit risk as a result of the three acquisitions. On a historical basis, the company had $110.1 million of operating income during the first half of 2000. The pro forma adjustments produce an operating loss of $200.9 million. Again, the effect of goodwill

Unaudited Pro Forma Condensed Combined Balance Sheet

June 30, 2000

(in thousands)

Liabilities and Shareholders’ Equity

Current liabilities:

(a) To record the preliminary allocation of the purchase price to goodwill and purchased intangibles, deferred tax liabilities and deferred stock-based compensation.

(b) To accrue estimated transaction costs.

(c) To eliminate the Acquired Companies’ common stock and retained earnings accounts.

(d) To record the acquisitions of the Acquired Companies’ equity securities by the issuance of the Company’s common stock, restricted common stock and the assumption of employee stock options.

(e) To record the allocation of purchase price to in-process research and development.

Source: 8-K/A March 30, 2001.

Unaudited Pro Forma Condensed Combined Statement of Operations for the Six Months EndedJune 30, 2000 (in thousands, except per share data)

(a) Ňî record amortization expense for goodwill and purchased intangibles over an expected estimated period of benefit ranging from two to five years.

(b) To record stock-based compensation expense generally over a three- to four-year period.

size=1 color=black face=Cambria>(c) Reflects the estimated tax effects of the pro forma adjustments. The pro forma adjustments for the amortization of goodwill and purchased intangibles, in-process research and development, and certain stock-based compensation are excluded from such computations, as the Company does not expect to realize any benefit from these items.

Source: 8-K/A March 30, 2001.

creation modifies the analytical conclusion. Roughly two-thirds ($192.1 million) of the pro forma adjustment to reported earnings is amortization of goodwill, a noncash expense that credit analysts will downplay.

The remaining pro forma adjustment to operating income (a $98.4 million reduction) reflects the recording of stock-based compensation over three to four years. Note that the recognition of the cost of employee stock options has been a contentious issue in the determination of financial reporting principles. Corporations have lobbied hard and, so far, successfully, to avoid showing the cost of employee stock options on the income statement, even though it reduces income available to shareholders just as ordinary wages and salaries do. Understandably, corporations would prefer to report higher net income by disclosing the impact of stock options only in the Notes to Financial Statements. In October 2001, Representative Michael Oxley, chairman of the House Committee on Financial Services, advocated that approach to the likes of Securities and Exchange Commission Chairman Harvey Pitt and Paul Volcker, chairman of the board of trustees of the International Accounting Standards Board.3

Notwithstanding a general reluctance to display the cost of employee stock options on its income statement, Broadcom had no choice about it. In acquiring Altima, Newport, and Silicon Spice, Broadcom assumed the companies’ obligations under employee stock option plans. The accounting rules required Broadcom to begin recognizing the expense.

Incidentally, the acquisitions of Altima and Silicon Spice involved one additional stock-related instrument. Broadcom assumed the two companies’ obligations under arrangements whereby customers earned warrants to buy stock, generally for $0.01 a share, on fulfillment of requirements for minimum purchases of goods. Initially, Broadcom recorded the assumed agreements as purchased intangible assets and goodwill, which set in motion annual amortization charges. After reevaluating the accounting with its outside auditor, the company switched to a method of recording no assets on its balance sheet and recognizing the warrants as reductions of revenue as they are earned by customers.