RESULTS AND DISCUSSION

Following the methodology regarding the examination of the natures of time series on C/D ratio and credit share of states and the graphical view of the series we have tested first whether the series are stationary or not.

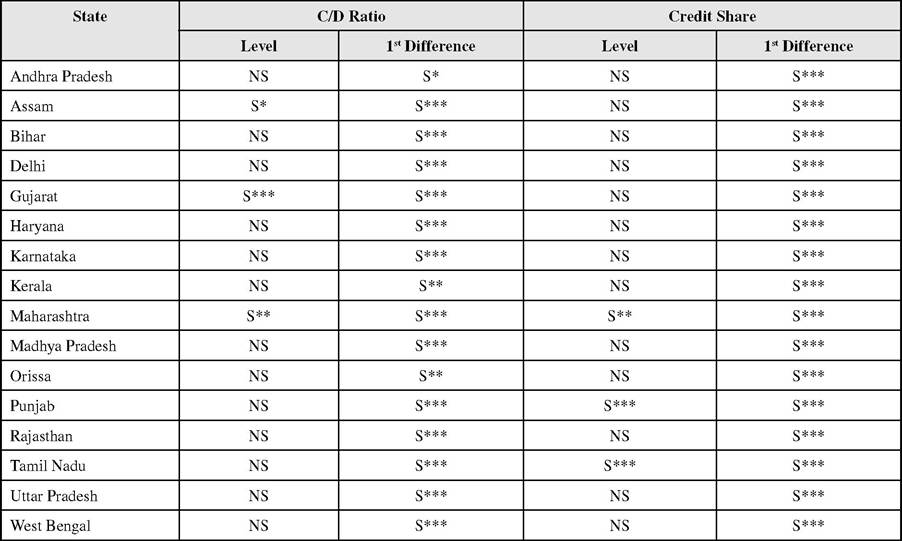

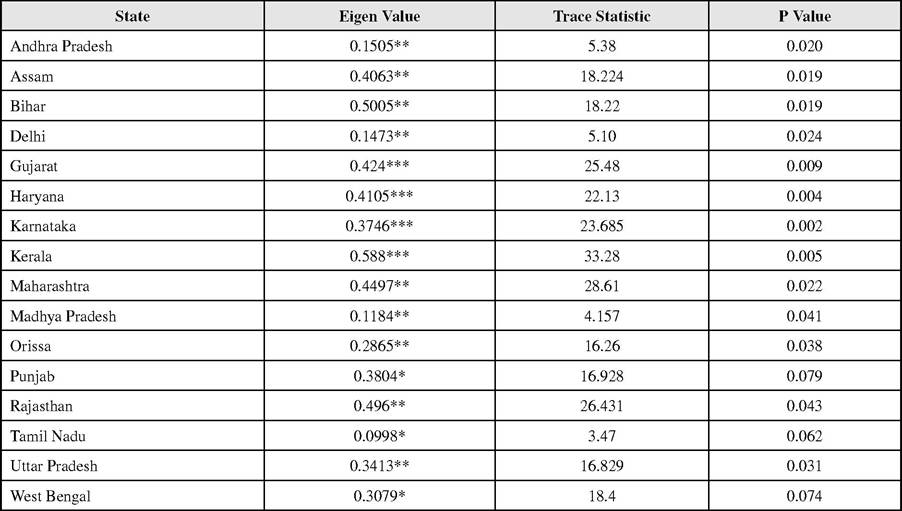

In other words, we have first run the unit root test of both the series for all the selected states for the entire period. The results are presented in Table 2. It is observed that all the series, except a few one, are non stationary at their levels but they are all I(1) series. This means their first difference series values will be stationary. The regression analysis for two first differenced series will not produce any spurious results. At the same time, if two series of a particular state are I(1) series then their errors will be stationary that means the series will be cointegrated to each other.The Johansen cointegration results and the associated Eigen values and Trace statistics are given in Table 3. In major Indian States, Credit deposit ratio and credit share are cointegreted of order one, i.e., I(1). Significance level is high (5% and above) in almost all states except Punjab, Tamil Nadu and West Bengal.

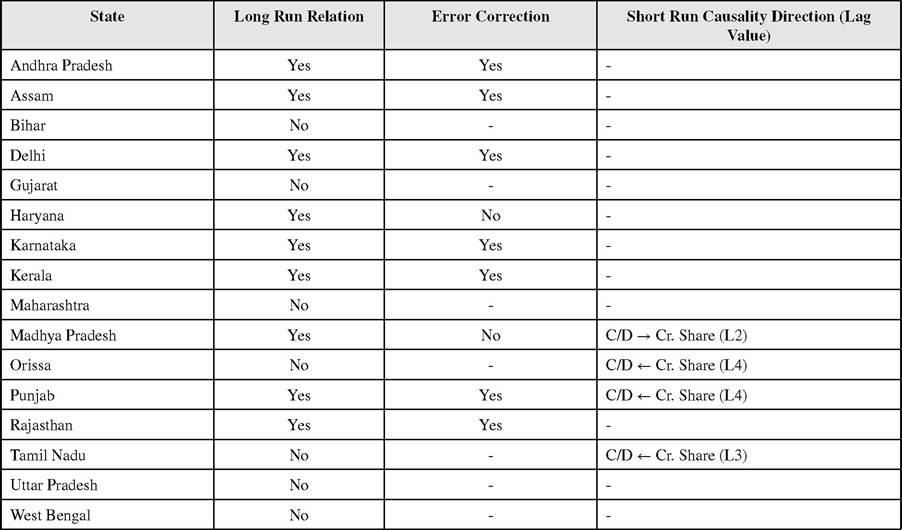

For long run time series on C/D ratio and credit share with I(1) property there should be at least one equilibrium relation and short run deviation from the equilibrium is corrected by the ECM. After incorporation of the estimated values of the error correction term of each of the states we have run

Table 2. Results of unit root test (during 1972-2008)

Note: ***, ** and * represent significant results at 1%, 5% and 10% respectively. S stands for stationary and NS stands for non stationary.

Table 3. Results of cointegration test

Note: ‘***', ‘**’ and ‘*’ denote level of significance at 1%, 5% and 10%, respectively.

Table 4.

Results of causality during 1972 -2008

Note: The → sign represent the unidirectional causality

the Granger causality test for the long run period 1972-2008. The results are presented in Table 4.

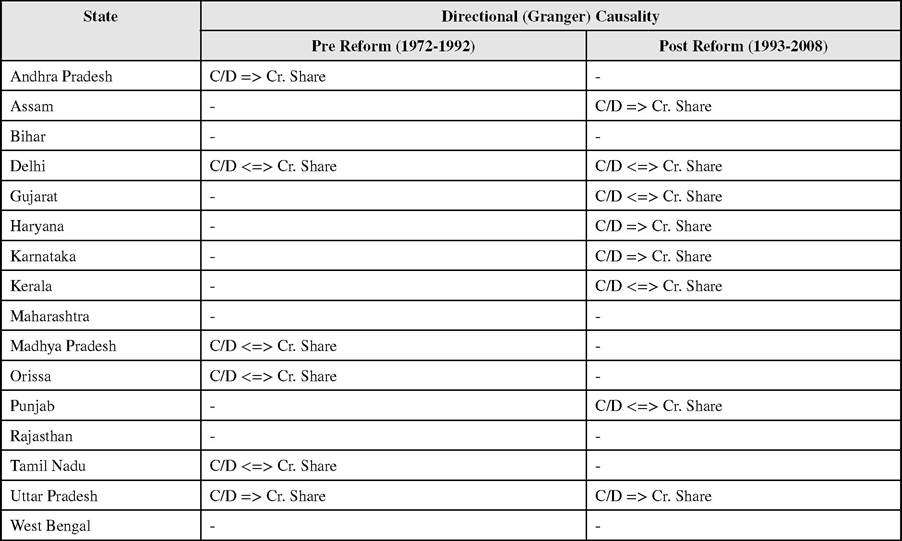

Table 4 provides the results of (i) existence of long run relationship between credit deposit ratio and credit shares of the states during the period 1972 -2008, (ii) short run causality direction between credit deposit ratio and credit share and (iii) finally, error adjustment if any departure from long run equilibrium occurs. Causality direction results are not clear for all major states in India in Table 4. It is may be due to major break in the name of economic reforms in India in 1990s and onwards. Since economic reform starts in India during 1991-1992 we divide the whole period into two sub-periods - pre and post reform period. Pre-reform period is 1972 -1992 and post reform period is 1993-2008. Now we apply the Granger causality test and results are given in Table 5.

The causality direction is running from credit deposit ratio to credit share in Andhra Pradesh and Uttar Pradesh in the pre-reform period. This means falling trends of credit deposit ratio of both Andhra Pradesh and Uttar Pradesh are causing the rising trends of credit share (refer to Figure 1 and 3) of the states. It implies that for these states falling efficiency leads the banks to invest their funds in other areas like government securities other than to give credit to the productive private sectors and as a result rise in volume of credit share leads further for supply of credit for safe investment like securities. There is bidirectional causality in Delhi, Madhya Pradesh, Orissa and Tamil Nadu in pre-reform period (1972-1992). Out of the four states positive direction of feedback causalities are found in Orissa, Madhya Pradesh and Delhi where rising trends of credit deposit ratio are causing rising trends of credit share for Orissa and Madhya Pradesh.

That means both the states of Orissa and Madhya Pradesh have improved in the pre reform phase in both the credit aspects and both are causing the both. But for Delhi, falling credit deposit ratio is causing falling credit share and vice versa.Table 5. Results of causality in pre and post reform period

Note: The => sign represent the unidirectional of causality, represents bidirectional causality

The state is declining in both aspects. The case for Tamil Nadu is different. Its falling trend of credit deposit ratio is causing rising trend of credit share and at the same time the rising credit share is causing to falling credit deposit ratio. It may so happen that the state started its journey from a very high credit deposit ratio and as a result of natural law on diminishing productivity the ratio is falling but the credit share is rising because of rising economic activities and good perceptions of the bankers regarding the state. Causality is absent in Assam, Bihar, Gujarat, Haryana, Karnataka, Kerala, Maharashtra, Punjab, Rajasthan and West Bengal during 1972-1992. That means the majority of the states are with no such causal relation between the two variables.

The results of causality are to some extent different for the post reform period with half of the total numbers of states are producing any sort of direction of causality. The causality direction is running from credit deposit ratio to credit share in Assam, Haryana, Karnataka and Uttar Pradesh during post reform period (1993-2008). The results for relatively developed states Haryana and Karnataka are similar as their rising trends of credit deposit ratio are leading to rising trends of credit share but the difference of results with the relatively backward states like Assam and Uttar Pradesh that their rising trends of credit deposit ratio are leading to fall in credit share. Bi-directional causality is observed in Delhi, Gujarat, Kerala and Punjab during post reform period. Directional causality is absent in AP, Bihar, Maharashtra, MP, Orissa, Rajasthan, Tamil Nadu and West Bengal. Causality is absent in several states during both the pre-reform period and post reform era (viz, Bihar, Maharashtra, Raj asthan and West Bengal), but individually, credit deposit ratio and credit share follow AR (1) process. Hence, we have a mixed result of short run causality between credit deposit ratio of the states in both the pre and post reform periods. One thing common in the short run results that whenever unidirectional causalities are present they are always running from credit deposit ratio to credit share, no reverse causation works. But for a long run period from 1972 to 2008 there are only three states namely, Orissa, Punjab and Tamil Nadu, for which the causality runs from credit share to credit deposit ratio (Table 4).