SIMULATING PAYMENT SYSTEMS BY AGENT BASED MODELING

A promising way to introduce endogeneity in payment system analysis and at the same time to reproduce the complexity that microfounded models are not able to tackle is by employing Agent Based Models (ABM).

In fact, Agent Based Modeling allows for the presence of multiple agents, to whom behavioural rules are assigned. These decisional rules can determine behaviours both in isolation as well as in interaction with other agents; they can depend either on agent’s characteristics and being periodically activated or on the prevailing market conditions and being triggered according to the evolution of some market variables (e.g., the imbalance on the own cash account, the interest rate dynamic, and so on). The interactions of different agents determine the market conditions, which in turn will affect the subsequent behaviour of the agents. In applying ABM to the payment system, it is possible to assign behavioural rules also in the field of liquidity management, defining the way agents choose liquidity sources as well as the lending or borrowing timing and conditions. Agent Based Models allow therefore to endogenise the liquidity issue in simulations.Although the ABM literature dealing with the payment systems is still scarce, the few contributions produced so far show that there are several fields where ABM may prove to be able to be a useful simulation tool for payment system analysis, which allows for an endogenous liquidity management8.

First, ABM may be used in payment system analysis to deepen the understanding of the funding strategies in an RTGS system as well as well as to evaluate the system’s efficiency: Galbiati and Soramaki (2011) analyse the trade off that treasurers face whenever the alternation of in- and outflows makes their cash balances insufficient to settle immediately the due amounts9.

Banks have to choose between borrowing liquidity or queuing payments, waiting for incoming funds. In both cases, agents bear costs: if they borrow money, they have to pay interests on their loan, if they delay payments, they have to face indirect delay costs arising from the loss of reputation or explicit penalties applied by their counterparties. Since the delay of a participant may cause a liquidity problem of its counterparty, simulations allow to discover the interactions of such individualist strategies that are strictly interconnected one to another. Agent Based Modeling allows in this case to endow participants with behavioural rules that determine their choice between turning to an external liquidity provision or queuing and waiting for internal liquidity to arrive.The simulations rely on a cost function, which provides the overall cost borne by the bank for each level of externally borrowed liquidity. It is assumed that the participant can opt only once a day for external liquidity, namely at the beginning of the day, so that before the onset of the settlement process, it has to decide how much funds it wants to raise. The overall bank’s cost is, therefore, given by the penalties for delays as well as by the cost of raising external liquidity at the beginning of the day. Rather than taking each day as a separate experience, a repeated game is introduced in which the daily initial level of liquidity chosen by each bank depends on its expectations of the others market participants’ choice (fictitious play).

The authors find out that for intermediate levels of unit delay costs, the aggregate external liquidity level in equilibrium is lower than the optimal one. The inefficiency of the system results from its comparison with a social optimal equilibrium, where agents minimise the total social costs of all market participants instead of their own one. An inefficient level of liquidity absorption seems to be caused by relative low delay cost per each unit of liquidity in comparison to the cost of external liquidity, which fosters free-riding and determines a suboptimal funding of external liquidity.

For those critical levels of unit delay costs the authors investigate whether in a smaller and simpler network, greater efficiency can be expected. A proportional increase of system’s size (total value of payments) and complexity (number of participants) determines an efficiency reduction: it is speculated that since the internal liquidity sources are more variable and therefore, less reliable, agents recur to higher levels of external liquidity per payment. A decrease in the number of participants, while keeping the system’s size constant, would increase the efficiency even more, since the liquidity provision would benefit from ‘liquidity pooling’ effects.

Secondly, ABM can be employed to draw lessons to shape the design of Large Value Payment System. ABM can, in fact, facilitate the evaluation of the either new policies’ or functioning rules’ effects that directly involve or have impacts on the participants’ endogenous funding decisions, since it allows to assess their impact on the functioning of the system and on the participant’s behaviour. The policy maker can therefore test second round effects, which might arise from market participants’ behaviours interaction and which otherwise might be difficult to gauge in advance.

The ABM usage for such purpose is exploited by Markose et al. (2011), who uses an Agent Based Model to evaluate the introduction of a policy rule that allows banks to borrow uncollateralized funds, against the payment of interests, from the Central Bank at any time during the day. Since this work investigates the impact in terms of liquidity circulation of different policy rules, the paper can be collocated in the stream of the “policy oriented” contributions.

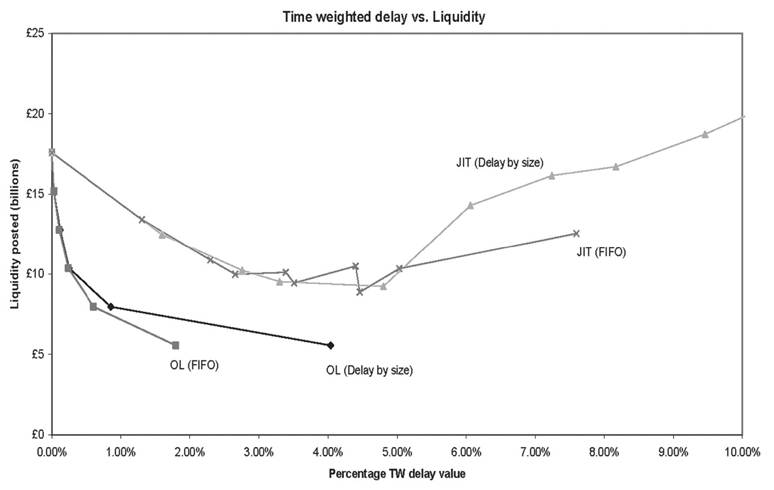

Two alternative frameworks are simulated: in the first group of simulations, falling into the so-called “opening liquidity” framework, banks can withdraw collateralised liquidity from the Central Bank only at the beginning of the day; in the second group, “the just-in-time liquidity” set up, banks can borrow uncollateralized funds at any time during the day according to their needs, against the payment of interests.

No repeated game is foreseen; each day represents a separate simulation with new exogenously set opening liquidity level or new parameters of the intraday borrowing cost function. Each of the two alternative systems has their own behavioural rules, which are kept constant across simulations. More specifically, the banks’ decision regarding the starting liquidity level to be pledged in the morning is not modeled and different initial values for opening balances on each independent one-day simulation are set exogenously; behavioural rules are introduced to define the trade-off between queuing a payment and requiring intraday extra external liquidity. Banks’ optimal delay is determined by minimising this total cost. For the sake of simplicity, the decision rule between delaying or raising funds does not take the possibility into account to reuse incoming payments to settle queued payments and reduce delays, so that the banks’ choice is a gross rather than a net liquidity decision.Comparing the two frameworks for the same amount of external liquidity, the “opening liquidity” system appears more liquidity efficient than the “just-in-time liquidity” one, since the cumulated percentage of settled payments’ value for each given time during the day is higher when liquidity is borrowed intraday according to the banks’ needs10. This result might be addressed to the fact that in the second framework, banks borrow more money than effectively needed, since the incoming payments are not netted (see Figure 1).

Furthermore, within each of the two frameworks (“opening liquidity” and “just-in-time liquidity”), the performance of the system is tested for two queue processing rules: a FIFO approach (first in first out) minimising the value of delayed payments and a size priority criterion (first the smallest) minimising their volume. Gridlock effects are proven to be more likely to occur in the second case.

A third rational for Agent Based Modelling in payment systems lies in the field financial stability assessment.

Since the outburst of the 2007 financial crisis, and even more after the Lehman’s collapse, policy makers have devoted more and more attention to financial stability issues. The interdependences between intermediaries have been clearly recognised as a contagion channel and, therefore, as a main source of systemic risk. In particular, systemically important participants and market infrastructures have been indicated as the connection point of several flows in the economy and consequently as particularly exposed to systemic risk. Policy makers around the world have been reinforcing macroprudential supervision and market infrastructure oversight with the aim to keep the level of systemic risk under control in order to take preventive interventions whenever potential risk materialises.Figure 1. Trade off between liquidity posted and time weighted delays (2011 Bank of England)

Large value payment systems-which link together intermediaries, infrastructures, and post-trading platforms-represent one of the most critical market infrastructure since possible delays or settlement failures from one or more participants can have a snowball effect due to the strict interdependencies within its participants.

As mentioned in the previous paragraph, a large body of literature using simulation has emerged to assess the resiliency of the system in case of shocks that affect the available liquidity of payment system participants.

In these stress testing exercises, payments executed from a bank hit by an either financial default or an operational outage, are simply dropped. To introduce a participant reaction, it is usually assumed that after a given time, the other banks become aware of the difficulties of the defaulted participant and stop sending payments: the incoming payments of the defaulted bank from any other market participant are therefore deleted as well. However, the residual liquidity flows, between banks that have not been affected by the outage, are kept unchanged.

Even those banks, that would have received incoming payments from the defaulted participant, are not supposed to change their payment behaviour towards the rest of the market, which is a rather restrictive and counterintuitive assumption.This kind of stress testing is a sort static simulations of defaults and does not capture the impact of critical events like a bank’s default on the behaviour of other market participants. In this vein, it could be speculated that the effects captured by these simulation are biased, since they omit to consider “by side” effects of the event, incurring in the risk of overestimating the resiliency of the payment system under assessment.

Agent Based Modeling may be used to take into account that, in case a market participant defaults, the behaviour of the other banks could be affected since they do not receive incoming payments that in the actual world they would have received and that contributed to fund their outgoing payments. In the absence of such incoming payments, banks would have been likely to change their behavioural strategies, modeled in terms of cost functions and trade-offs between raising liquidity and delaying payments.

For example, Arciero et al. (2009) use an ABM to execute a simulation of a default, in a model that takes both the payment system and a stylised money market into account. They simulate a direct-debit based system with very few market players, in which each participant is endowed with daily initial cash and collateral balances. The model is calibrated with BI-REL’s data, the Italian gross settlement system in 2007: the five banks of the model are generated by collapsing a higher number of participants. The initial cash balances stem directly from the opening balances held at the RTGS system, while the opening collateral balances are estimated starting from the maximum collateral pledged at the central bank for intraday credit purposes. Payments between banks are generated for each participant through three random draws from a uniform distribution: the first determining whether a payment is executed or not, the second its exact quantity and the third one the receiver.

The behavioural rule of any agent requires him to compute the expected end-of-day balance at each tick of an internal clock of the model, i.e. the liquidity that the participant expects to hold at the closing of the trading day on the own cash account. It includes: 1) the initial liquidity level; 2) all the in- and outflows already settled; 3) all the pending in- and outgoing payments.

If the value of a due obligation is higher than the actual balances, so that it cannot be immediately settled, the agent can pledge collateral at the Central Bank to receive intraday credit as long as it has enough collateral. After having consumed its whole collateral endowment and provided that the outgoing payment value is higher than the current and expected end-of-day balances, the bank turns to the money market in order to raise the missing funds. The matching of opposite intents on the money market is only quantity-based: in case the expected liquidity of a randomly selected market participant is equal or higher than the requested deposit, the money market deal is executed; otherwise, the payment transaction is delayed and the deposit request is turned to a further randomly chosen bank. After a specific number of bounces, the payment is considered unsettled and is removed from the expected end-of-day balance. If the value of the due payment is higher than the current balances but lower than the expected end-of-day liquidity, the payment will be delayed and queued, waiting for new incoming funds to replenish the expected liquidity. The payment will be automatically resubmitted to settlement process in the following tick, when the current cash balance may have varied for effect of incoming payments: if liquidity is now available, the delayed payment will be automatically settled.

A default is introduced by simply letting a bank switch from this normal operational behaviour to inactivity. At the beginning, other market participants are not aware of the event: they continue sending payments to the defaulted bank and including the future incoming payments from that bank in their liquidity expectations. After a certain amount of time, namely half an hour, the participants gain knowledge of the failure, stop sending payments to that participant and update their end-of-day balance eliminating the pending payments from the defaulted agent. Since the end-of-day balance affects the behaviour of a participant towards any market participant, the default of a bank that causes a readjustment of the expected end-of-day balance has also effects on the behaviours towards the rest of the market.

The authors find out that immediately after the default the expected end-of-day balances of other market participants are inflated by the pending inflows, which are expected to come from the defaulted bank. To face the own outgoing payments, after having used the whole endowment of collateral to get intraday credit from the Central Bank, money market activity is enhanced. Delays on the expected incoming payments from the defaulted bank start cumulating, up to the moment in which, through a random process, the other agents start becoming aware of the default. Pending inflows are switched to defaulted credits and eliminated from the expected end-of-day balances.

Interestingly in the simulations, an intervention from a lender of last resort is needed to help survived market participants to overcome the stress conditions and the losses, avoiding consequential defaults in a contagion whirl. A possible explanation for inability of the system to return automatically to an equilibrium without external interventions is that the number of agents in the simulated model is very restricted; since so that the relative importance of a single bank is on average 20% of the whole payments, the failure of one of them would therefore imply the default of a relatively high percentage of payments, which would be hard to overcome by the remaining banks.

4.