AGENT BASED MODELING IN MARKETS AND PAYMENT SYSTEMS: WHICH WAY FORWARD?

The three contributions on ABM reviewed in the past paragraph witness the huge potentialities of this approach, but are still affected by weaknesses limiting their usage on a more practical ground.

In the following, some hints are discussed on how the models could be extended.The interesting efficiency exercise of Galbiati and Soramaki could be extended by allowing market participants to recur to external liquidity more than once per day, relying on sources that are available at any time during the operational day. Among the possible options, the authors could choose either the Central Bank’s intraday credit or the mobilisation of reserves. Switching from an intraday to an overnight horizon, they could explore the possibility to commute intraday credit into standing facilities or to turn to the interbank money market. Especially, the linkage with an interbank market would introduce the concept of liquidity circulation, so that the model could be successfully used to assess the system’s redistribution efficiency. In this way, the simulated system could be less isolated from the rest of the liquidity sources that are at banks disposal.

Additional developments of the paper could be also imagined with a view to shed further light on the two main results: 1) the lower efficiency of the individualistic approach to liquidity towards the minimisation of the total social liquidity costs; 2) the reduction of efficiency which takes place when increasing the size and the number of participants of the Payment System.

Referring to the first outcome, given the progressive increase of settled flows in LVPS, it would be interesting to test whether and to what extent an increasing number of payments worsens the outcome of individualistic behaviours in comparison to the social optimal equilibrium. The model could contribute in case any policy maker should be intended to calibrate the exact level of incentives to be introduced in Payment Systems to stimulate participants to manage liquidity according to a collective rather than an individualistic optimisation function.

Since the reduction of the number of participants to a Payment System, while keeping the total turnover unchanged might be due to an increase in the tiering of the system, namely to the decision of some banks not access the LVPS directly but indirectly through a direct participant who acts as the agent, the model could also be interestingly extended in order to include this second kind of indirect participants. In this way, it would be possible to test if the “liquidity pooling” effect of the second result of the paper still holds or whether the tiering introduces some new aggregate effects.

Extensions of the Markose et al. model could be imagined in several directions. A first stream of development could lie in switching from a gross to a net liquidity regime: the decision rule between delaying or raising funds should take the possibility into account to reuse incoming payments to settle queued payments and reduce delays. This would depart from the simple rule of thumb by which the optimal delay is fixed, which currently relies only on the liquidity available at the moment the payment comes due: even if it is not the optimal rule “since none will be optimal in general,” as the authors state, it would be a more realistic assumption. The optimal time of delay modeled in the JIT set up could be reliant not only on the available liquidity at the moment when an obligation comes due, but also on the value of the expected flows given by the sum of the expected incoming payments and the future outgoing payments. This would make each participant’s decision reliant on the behaviour of other banks, possibly yielding interesting aggregate outcomes.

Secondly, besides testing different levels of initial liquidity values in the OL framework, a decision rule for the opening liquidity could be modeled; as recognised by the authors, interesting input could be provided by introducing a learning process so that at the beginning of each simulation the external liquidity level is determined relying on the daily experience of the previous days.

For example, the decision could be function not only of the expected liquidity at the end of the day, namely balances Bt plus expected incoming payments ∣e excluding the outgoing payments Ot but also of the delay costs of the previous day dt1 and the opportunity costs of having posted collateral at the Central Bank c: Recursively d and ct1 will embed the experience gained from the beginning of the simulation to the day t-1. Since the incoming payments will be the result of other participants ’ behaviour, this extension of the model would produce an environment in which the synergic interactions of individual strategies might be fully appraised.However, this kind of modeling would still imply a one-day horizon, so that each new day is an independent experiment in which the agent can profit from the experience gained in the previous games but which isn’t affected from the result of the previous day’s behaviour. A third kind of extension of the Markose et al. model could be therefore, the introduction of a multi-period framework, namely the possibility to follow the interaction of the agents for several days. This could allow to determine a repeated game in which the players base their daily operating rule on the equilibrium outcome of the previous day. For example, the account balance of liquidity available at the beginning of each day could be made equal to the previous end-of-day balance: the new experiment will inherit not only the experience gained from the previous days but also their effects.

In addition, the Arciero et al. model needs to be extended in several directions, in order to represent a more realistic framework11.

First of all, this model should be “credit based” which is the standard for RTGS systems. Moreover, it should allow for a higher number of agents to interact, as if it happens in the payment systems of developed countries. With a more realistic number of agents, for example calibrated on real Payment Systems data, the default of one of them might be differently absorbed by the other market participants than in the previous stylised version and the system might be able to reach a new equilibrium without the need of a lender of last resort.

Secondly, the model should allow simulating the payment system over a longer period of days. When dealing with a multiple daytime horizon, it must be taken into account that over the so called maintenance period banks have to fulfill a Minimum Reserve Requirement (MRR). Central Banks require namely that market participants possess on the own account a certain amount of money at the end of the days of that period. According to the monetary policy implementation framework, banks can be required to hold minimum reserves on a daily basis or on average: in the last case, they are allowed to mobilise funds according to their needs and convenience, as long as they compensate by maintaining enough excess reserves on their account at the end of the subsequent days. In a multi period model, the decision to raise or lend funds in the money market will therefore not only be triggered by the bank expectations on its liquidity, but also by the fact that each bank has to be compliant with the MRR.

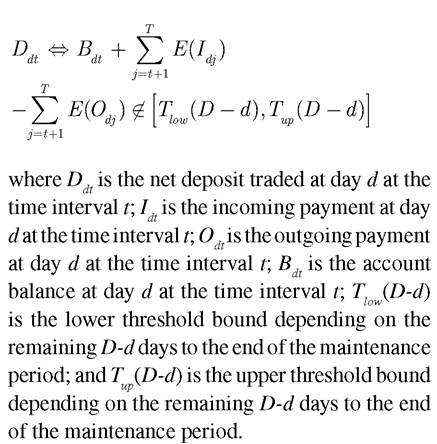

To this aim, a possible option, empirically founded (Cassola, 2008) is to imagine that end- of-day reserves have to fall within thresholds that allow him to be compliant with the MRR at the end of the period along a linear fulfillment path. These thresholds can be modeled as function of both the number of days to the end of the maintenance period, since it can be expected that banks will be more focused on the requirement’s fulfillment the more the end of the maintenance period approaches, and the previous days’ end- of-day balance pattern.

Formula 1: Condition at which a net deposit is traded

We can hypothetically split the maintenance period into two parts: a first one during which we can assume that banks do not care much about the MRR and a second one when the market participants have to explicitly target a desired level of end-of day balance that allows them to be compliant.

During this second subperiod the more the end of the maintenance period approaches the more banks can tolerate smaller and smaller deviations from their own target level;

Third, the possibility to recur to the money market in case of lack or excess of funds has to be more extensively developed. The marginal role that has been attributed to the market in the first version of the model, to which banks turn only after having exhausted their collateral endowment to be pledged at the Central Bank, seems to be limiting. First, it does not consider banks’ opportunity costs linked to the fact that these securities are not invested. Furthermore, it may be speculated that in a world where all agents believe that the Central Bank has injected all the liquidity needed by the system to clear and where the money market efficiently redistributes the liquidity across agents, the priority attributed from banks to liquidity sources is inverted: they first rely on the money market and only residually on Central Banks’ facilities (see Figure 2).

Fourth, a simple money market microstructure needs to be introduced. The counterparty search process used in the old version of the model that sequentially evaluates the liquidity position of randomly selected banks and that rejects the proposal after a limited number of failures, could determine a suboptimal liquidity distribution mechanism. In fact, a proposal may be rejected also in the presence of one or more banks that would be interested in such a proposal, because the two willing have not been matched by the random selection mechanism. Money market transactions should be therefore concluded on an electronic trading platform12, on which all trading proposals are contemporaneously exposed. A realistic

Figure 2. Interest rate dynamics for a quantity based price rule (Arciero et al., 2010)

matching mechanism should be based not only on the quantity but also on the interest rate, otherwise the simulated interest rate time series will follow a random walk, being driven by innovations in payment arrivals, which are stochastic in nature, while the actual interest rate series are usually stationary (see Arciero, et al., 2010).

In this way, on the one hand, the matching likelihood decreases, since the success of the search depends on the joint probability of matching the quantity and the rate; on the other hand, the contemporaneous presence on the screen of all the liquidity imbalances in the system, facilitates the matching of opposite needs by reducing the searching costs and allows competition between banks with the same need (lack or excess of liquidity).

The agents’ proposals exposed on the money market cannot be left unchanged since the end of the operational day: more realistically, the banks check periodically whether their proposals need to be revised in terms of quantity and/or of rate. On the one hand, an unexpected incoming payment or the need to delay an outgoing payment might induce them to vary the asked or offered quantity. On the other hand, the flow of time makes the liquidity need more compelling as the risk of not reaching the targeted end-of- day balance increases: the bank will revise the proposed rate, making it more convenient for a potential counterparty and thereby increasing the probability of matching.

As a consequence the interest rate will fluctuate around the policy rate according to the temporary imbalance in the aggregate liquidity need of the system13. Depending on such fluctuations, banks could decide to post additional proposals on the market even if their expected end-of-day balance is close enough to the target value that allows the MRR compliance. In this case, the access to the money market is justified by convenience reasons: positive spreads on the key policy rate will stimulate lenders to look for potential profits; negative ones will induce borrowers to anticipate higher reserve levels to reduce future borrowing costs. The deviations from the policy rate are in this way neutralised, thus granting a mean reverting process for the interest rate.

The money market could be furthermore enriched with credit risk issues: a bank specific random spread could be applied on the rate of each proposal to borrow money, which would reflect different levels of individual creditworthiness. The model could be also expanded to include exchanges, which last longer than overnight, providing in this way a money market interest rate yield curve.

Finally, the central bank as monetary policy authority could be introduced: as a consequence the fixing of the interest rate policy level and the execution of monetary policy operations should be modeled. Interest rate expectations and market risk premia should affect the banks’ behavioural rules. The model could be hypothetically expanded to embrace at the limit the whole economy. However, a delicate equilibrium line has to be set down after which any benefit deriving from an increase in realism is outweighted by the disadvantages of enhancing the complexity of the model.

5.

More on the topic AGENT BASED MODELING IN MARKETS AND PAYMENT SYSTEMS: WHICH WAY FORWARD?:

- Challenges for Scaling Agent-Based Modeling

- Replicating Agent Training

- HYPERTHERMIA

- Modeling Dispersal Processes

- Contributions

- DYSPHAGIA

- Ethambutol

- Local Markets

- Recording Electrodes

- Appendices