Systemic Fraud in the Mortgage Securitization Industry

One way to see how this played out among the largest banks is to consider the settlements that the banks made with the government over mortgage fraud, predatory lending, and securities fraud.

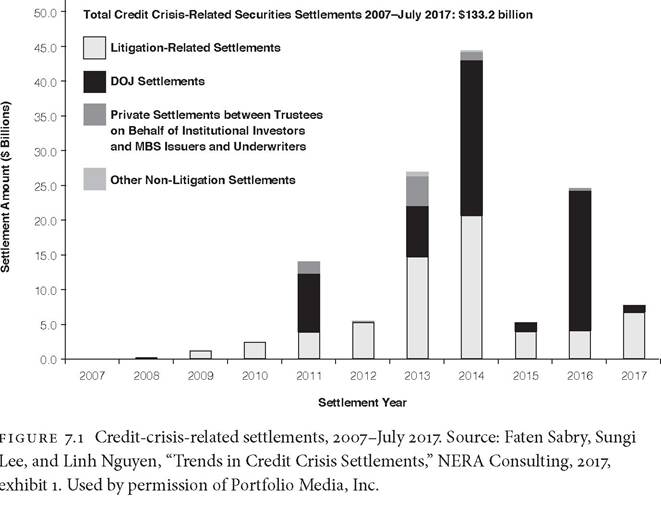

Figure 7.1 shows that between 2007 and 2017, $133.2 billion was paid out by banks in settlements for mortgage and securities fraud. These settlements peaked in 2014 when almost $45 billion were paid out to the government and various groups of private investors. Fifty-five percent of all settlements went to the federal government, while 26 percent went to class action suits, 7 percent to insurance companies who were being paid for securities fraud, and 12 percent to other litigants (Sabry et al., 2017). Fligstein and Roehr- kasse (2016) show that vertically integrated banks were the most likely to have settled predatory lending and securities fraud cases. They show that thirty-two of the sixty largest banks in the conventional and nonconventional mortgage origination and securitization businesses settled some kind of lawsuit for mortgage or securities fraud. All nine firms involved in investment banking and nine of the eleven largest commercial banks settled such lawsuits. Banks involved inCredit Crisis-Related Settlement Amounts by Year: 2007-July 2017

both origination and securitization were more likely to settle lawsuits than banks who were participants in only one or the other.

The cases of Bear Stearns and WaMu illustrate how the pressure to continue originating mortgages after 2003 in order to be able to create MBSs and CDOs worked. Both firms went aggressively into the nonconventional mortgage market and in particular dramatically increased their origination of option ARMs and subprime mortgages. The pressure to continue originating mortgages in order to have them as inputs into securities never decreased, even as the number of potential customers for new mortgages began to decline.

In fact, as the supply of mortgages started to shrink, instead of pulling back from the market, both of these vertically integrated banks doubled down and chased after more and more customers who they knew had impaired credit and not enough income to support their mortgages. To keep their securitization machines running, they helped many of these customers commit mortgage fraud, and they engaged in predatory lending by offering terms that were too good to be true to other mortgagors. Both of these actions were to provide them with nonconventional mortgages that were more lucrative to turn into securities because they were able to generate higher fees and greater returns on MBSs and CDOs. Using these loans that they knew were likely to fail to make securities meant that they were committing securities fraud as well.They sold those mortgage securities as AAA rated and held many of them on their own accounts. They borrowed money to originate and securitize mortgages. They also borrowed money in the ABCP and repo markets in order to support their own purchases of those securities. In the end, many people, particularly those who committed fraud or were the victims of predatory lending, were foreclosed on at a historically high rate. That put more pressure on other homeowners who saw the value of their homes decline and caused the housing market to crash. It also meant that many securities that were built on these mortgages, particularly those built in 2006-2007, were susceptible to default.

My analysis shows that the nature of the whole system was in fact at fault. The demand for MBSs and CDOs pushed banks to take on riskier and riskier mortgages. Their activities kept house prices rising for a while as they focused their attention on zip codes where there had already been a high level of house price appreciation. But eventually, to keep going, they had to cut corners and engage in mortgage fraud and predatory lending. The banks that were the most susceptible to these pressures were those who were involved in both origination and securitization.

The massive fraud committed from 2004 to 2007 was driven by the need of banks to keep originating mortgages in order to meet the demand for securities based on those mortgages. As the supply of mortgages dried up, banks had to work harder and harder to find mortgages to keep their securitization machines going. This meant that they normalized mortgage and securities fraud as a necessity to keep the party going. In the end, the securities based on those mortgages began to fail. When they did, banks had to quickly pay back funds borrowed in the ABCP market. They quickly went from illiquid to insolvent.The narrative that no one was punished for their role in creating the crisis is only half true. Banks did pay huge fines for their illegal activities. But those activities were not the main thing driving the banks over the cliff. Their reliance on procuring mortgages to create securities meant that as the conventional and then the nonconventional mortgage markets dried up, vertically integrated banks became desperate to keep their securitization machines going to keep their high profits intact. They realized the only way this could work was to cut corners by engaging in mortgage fraud and predatory lending. This worked for a short time, but eventually many of those bad mortgages faced foreclosure because the people who bought them simply could not afford the payments.

What the American public did not realize is that just because all of this ended badly, it did not have to be because someone committed a crime. The crimes of mortgage fraud, predatory lending, and securities fraud were oddly the collateral damage at the end of the whole mortgage cycle centered on the vertical integration of the banks and their focus on securitization. The market for MBSs and CDOs was kept going by the mortgages that were obtained fraudulently. But the bad end is inevitably what happens in capitalism when all of the easy profits get made and the market is saturated. It pushed banks to do whatever they could to keep their vertically integrated structures going. Without regulators watching to ensure that firms don't cross the line from aggressive to illegal, things tend to end badly. But of course, such regulators would have had to understand what was going on. I finally turn to how the regulators missed this whole thing.

More on the topic Systemic Fraud in the Mortgage Securitization Industry:

- Fligstein Neil. The Banks Did It: An Anatomy of the Financial Crisis. Harvard University Press,2021. — 334 p., 2021

- Settlements

- References