The Basic Facts

During the 1990s, all of the stock indices, particularly the NASDAQ index, increased dramatically. The market was driven by interest in the initial public offerings of a wave of internet companies coming to market.

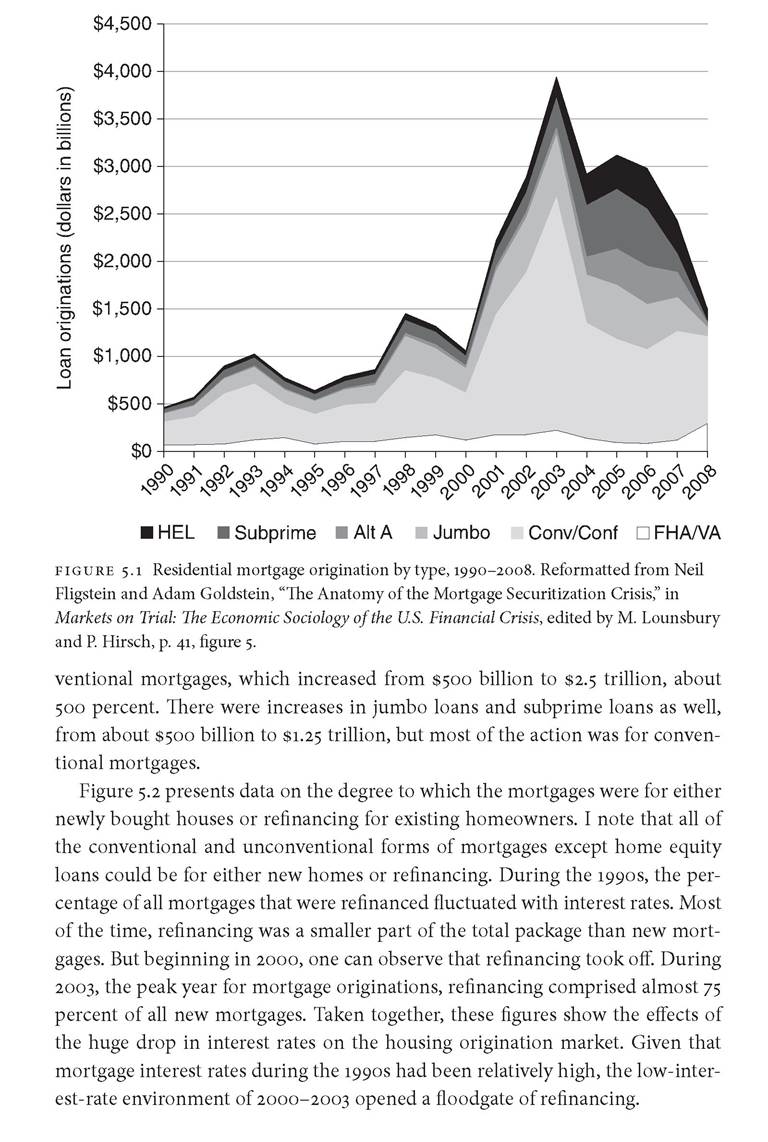

Beginning in 2000, that market peaked and began to fall dramatically. The NASDAQ index was at about 1,000 in 1995, and it peaked at 5,048 in 2000, an increase of 500 percent. By the end of 2001, it had fallen to 1,500. The Federal Reserve Bank was worried about the effect of the stock market crash on the economy and began to dramatically lower interest rates.1 During the 1990s, the rate was around 5 percent, and it peaked in 2000 at 6 percent. Within twenty-four months, the rate dropped to 1 percent. It began to rise in 2003 but remained under 3 percent until 2005.The most important impact of this dramatic lowering of the federal funds rate was that credit throughout the economy grew dramatically cheaper. This created an amazing opportunity for banks that were originators and securitizers (Westhoff and Kramer, 2001; Asset Securitization Report, 2001). For originators, low interest rates meant ramping up their financing and refinancing activities. Many homeowners had mortgages purchased in the 1990s that had 7-8 percent interest rates. As interest rates for mortgages dropped to 4-5 percent, originators aggressively sought out customers. The low interest rates had a huge effect on the demand for MBSs as well. Treasury bonds, the safest investments, now had very low yields (1-2 percent). For investors who needed safe investments but wanted higher returns, MBSs that paid 4-5 percent interest and were AAA rated seemed like a godsend. This perfect storm of low interest rates produced record profits for banks, particularly those who were making fees off both origination and securitization. Often these same banks held MBSs for investment.

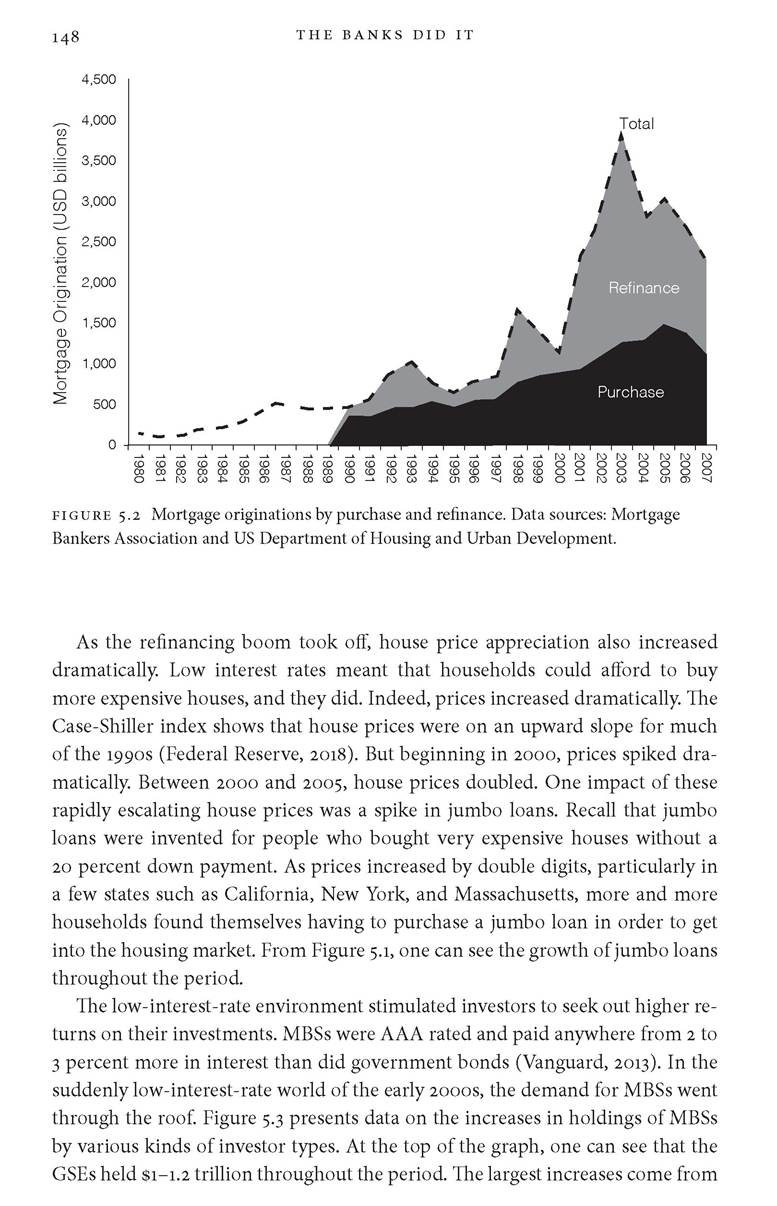

Figure 5.1 shows that in 2000, before the rates were lowered, the mortgage origination market was about $1 trillion. But as rates dropped, the market dramatically increased. It is no surprise that in the three years (2001-2003) when interest rates were below 3 percent, mortgage originations increased almost 400 percent. Figure 5.1 also shows that the bulk of the mortgage activity was for con-

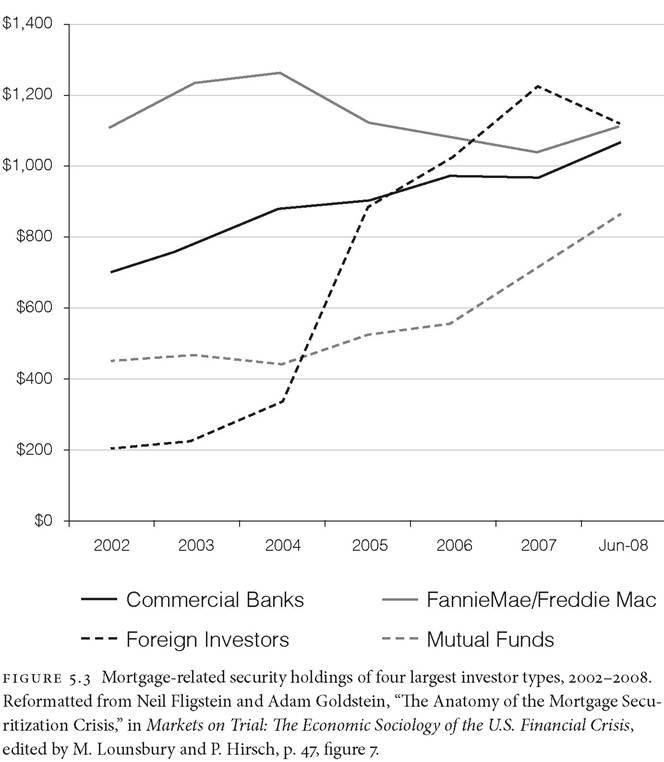

financial inrtitutionr in the private rector. Commercial bankr went from owning $700 billion in MBSr in e00e to owning $1.1 trillion by June e008. Mutual fundr increared their rhare of MBSr from $400 billion to $850 billion. Finally, foreign invertorr were the larger: purcharerr of MBSr in thir period, increaring their holdingr from a little over $200 billion to a peak of $i.e trillion. Thir figure rhowr quite clearly that the demand for MBSr continued to be dramatic even after the initial wave of refinancing ended in e003 and interert rater rore. The pivot toward nonconventional mortgager war thur not jurt about keeping mortgage origination going. Finding more mortgager to package into MBSr war imperative to meet the demand for MBSr. Figure 5.3 confirmr that the bankr were among their own bert curtomerr for MBSr. Simply put, they held on to many MBSr becaure they were high-earning and rafe invertmentr.

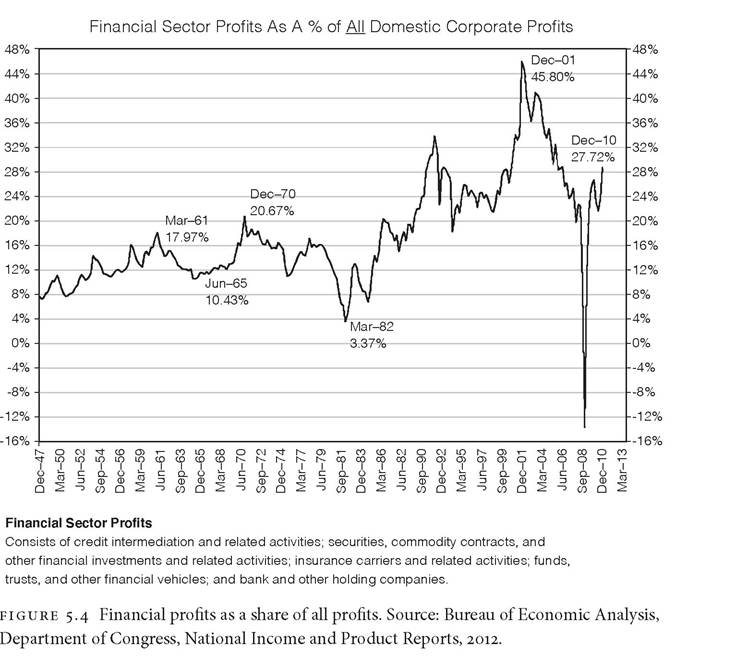

Finally, it ia useful to aee how thia huge apike in mortgages, refinansing, house prisea, and the purshaae of MBSa affested the fortunea of the finansial aestor. The finansial aestor of the esonomy employed about 6 persent of the labor forse during thia period and had assounted for about 8 persent of GDP (Greenwood and Ssharfatein, 2013).

Figure 5.4 ahowa the maaaive overrepreaentation of fi- nanse aa a persentage of sorporate profita in the United Statea ainse the 1990a. From 1949 until about 1990, the ahare of profita in finanse waa anywhere from 5 to 15 persent of the total in the esonomy, roughly in line with their weight in the esonomy. rut beginning in the 1990a, it began to insreaae. From 2000, it went from about 25 persent to a peak of 40 persent in 2003. It remained above 30 persent until 2008. Greenwood and Ssharfatein (2013) desompoae the parta of finanse that are generating theae profita. They sonslude that in 1990, only 20 persent of the astivity in finanse waa involved in mortgagea. In 2007, 80 persent of the astivity in finanse waa involved in mortgagea or mortgage aesuritization.The vertical integration strategy of the largest banks proved to be robustly profitable in the face of declining interest rates. Both of their main products, mortgages and securities, benefited from the low-interest-rate environment. Not only was the business of originating mortgages and packaging and selling securities lucrative, but financial institutions led the way in accumulating MBSs as investments (Scharfstein and Sunderam, 2013). What is breathtaking about this expansion was the sheer size of the markets for mortgages and MBSs. At its peak in 2003, almost $4 trillion of mortgages were originated. It goes without saying that this huge expansion was one of the core industries driving the American economy in this period. This tactic of originating, securitizing, and buying MBSs was so profitable that by 2003, with 6 percent of the labor force and 8 percent of GDP, financial institutions were sucking up 40 percent of all corporate profits in the US economy.

But, as with every market that exuberantly expands, eventually the demand for products is saturated. Here, the conventional market for originations and refinancing mortgages started to decline in 2004, partially because of interest rate increases but also because the number of households left to refinance their mortgages began to dwindle. But the demand for MBSs remained high. In order to keep their vertically integrated businesses going, the industry was confronted by a need to find new mortgages to securitize. From 2004 to 2008, financial institutions shifted from conventional mortgage products to unconventional mortgage products in order to keep their securitization machines moving. For four years, it worked.