The Contagion Process

The Mexican financial system is very well capitalized. On average, its capital ratio is of around 16%, with a minimum of 11.6% and a maximum of 424%. This explains to a great extent the lack of sensitivity to shocks because banks are able to absorb losses without risking individual solvency and avoiding triggering a contagion process.

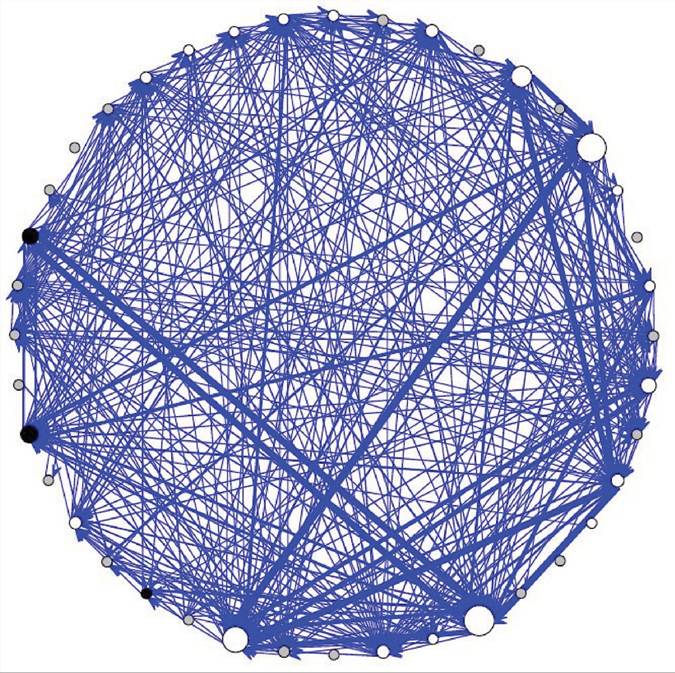

Nevertheless, when considering the “tail” scenarios a very interesting case of study arose. After a very severe shock in the stock market index, and foreign and domestic interest rates the regulatory capital of three banks went below the minimum requirement15. These banks were small banks in the system; in Figure 14, we observe such troubled banks in black, the exposed banks to them in white, and the banks with no exposures to such banks in gray. The composition of its portfolio made them practically immune to credit effects, so this was purely a market risk effect. If this were an idiosyncratic failing process, it was likely that this failure would have gone unnoticed.

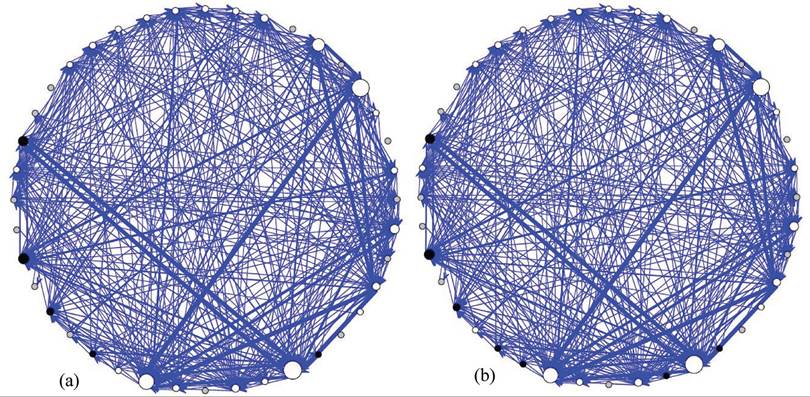

The interesting part occurred through the contagion phase: the magnitude of the shock led to failure to three banks, but several of the remaining banks were weakened by it, to the extent that the failure of these banks to honor its interbank obligations caused the failure of a medium sized bank and some small banks. This in turn led to the failure of a set of small and medium banks

Figure 14. Interbank exposures network on June 30 2011 after an initial shock

Figure 15. The interbank exposures network on June 30 2011: (a) Intermediate state of the interbank exposures network on 30 June 2011; (b) Final state of the interbank exposures network on 30 June 2011

(Figure 15a). At the end, seven banks would have failed, including a medium size bank (Figure 15b).

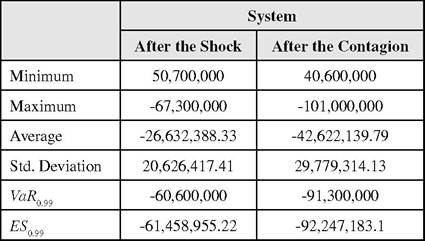

The exercise with the most severe scenarios provided qualitatively similar outcomes (though are not reported here). The difference with the above reported scenario is that in some occasions the initial shock caused the failure of less banks, causing the failure of some more banks in successive rounds. This case is one of the worst within the 5,000 stress scenarios. Table 1 summarizes the stress scenarios with some descriptive statistics.

Table 1. Statistical measures for the distribution of losses of the system

5.