Systemic Relevance of Financial Institutions

At the core of macro-prudential regulation is the determination of the participation of an institution in the systemic risk. There are many recent proposals, which vary widely on their underlying models.

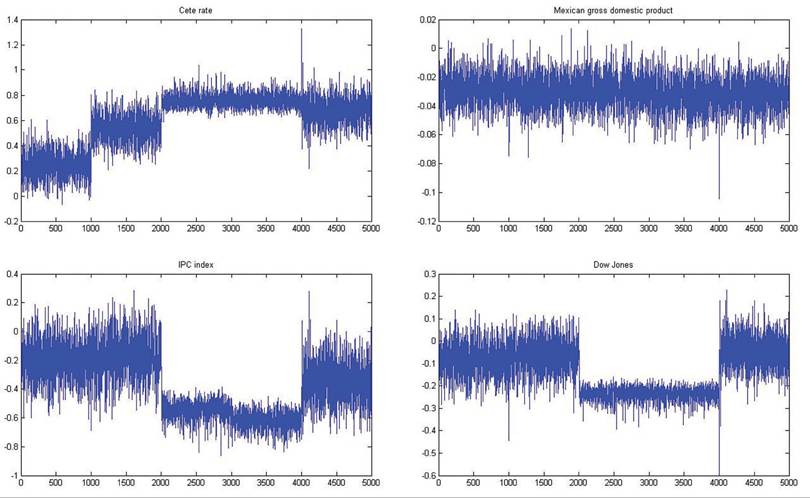

In Tarashev et al. (2009), the authors borrow the Shapley value concept from game theory, although it is not clear if such concept can be directly used in the context of systemic risk. A different stream of work is the one followed by the Financial Stability Board (FSB) in which it is proposed that the condition of systemic relevance of a financial institution is associated with size, lack of substitutability and interconnectedness (See FSB, 2009). Following a totally differentFigure 8. Realizations of some risk factors under the “tail scenarios”

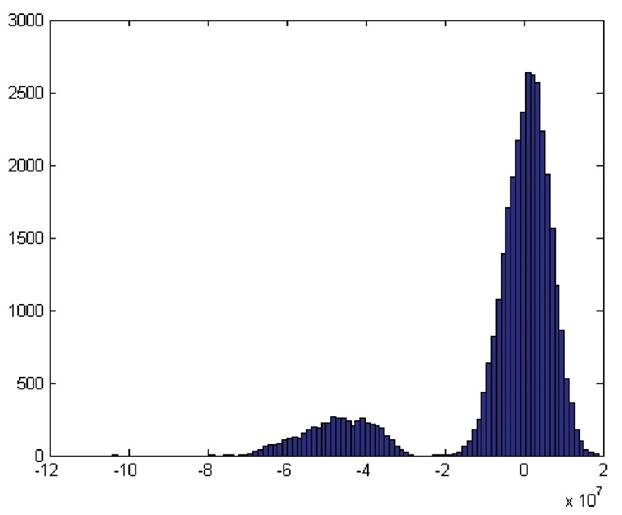

Figure 9. The distribution of losses for the Mexican banking system 35,000 scenarios including 5,000 biased scenarios

approach Adrian and Brunnermeier (2008) define a risk measure which they call the CoVaR13. Such value can be defined as the Value at Risk (VaR) of financial institutions conditional on other institutions being in distress. In this work, we are interested on the VaR of the banking system conditional on particular banks being in distress.

We find that the CoVaR is probably the best from the above-mentioned measures as it can be easily derived once the SDL has been obtained14. Moreover, such distribution and measure encompasses the elements proposed in FSB (2009) as in our proposal the interconnectedness element is implicit in the estimation of the contagion process.

The precise definition of CoVaR can be revised in Adrian and Brunnermeier (2008) but in order to illustrate in a graphical way how such measure works we will show some interesting graphical representations.

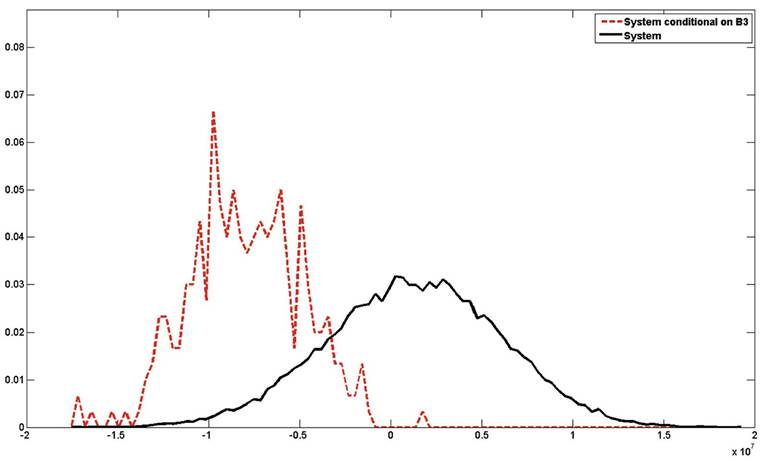

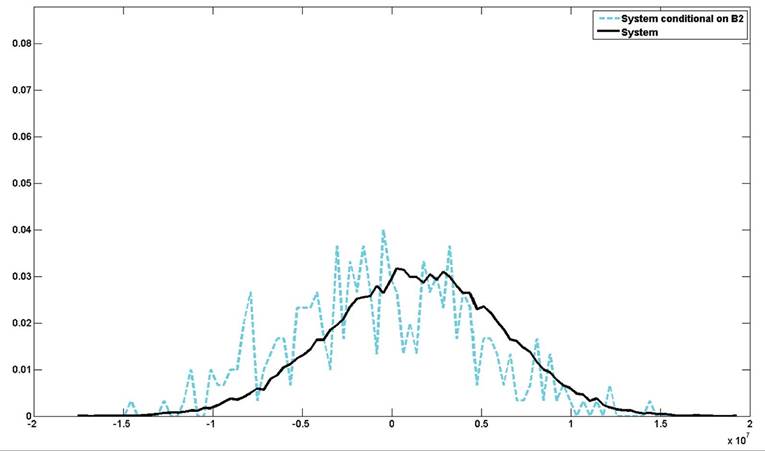

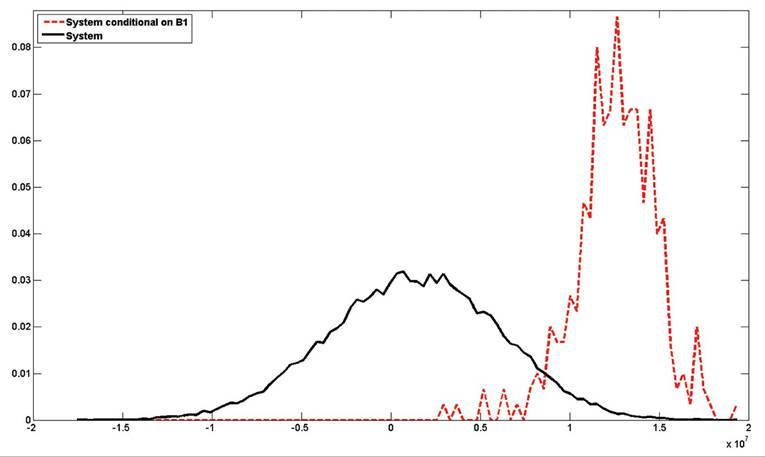

Figure 11 illustrates the distribution of losses for the system and the distribution of the system given that bank B3 is in distress. Figure 12 shows the same distribution of losses for the system and the distribution of losses of the system given that bank B2 is in distress. Finally, Figure 13 shows the same case but using bank B1 to condition the distribution of losses for the system.From the previous figures, we can see that the contribution to the risk of the system is different for each bank. For example, bank B3 is the one from these three banks, which contributes more to the systemic risk while bank B1 is the one, which in fact has a negative correlation with the system in terms of losses when one is located at the tail of the distribution. If we compute, as it is proposed in Adrian and Brunnermeier (2008), the difference between the CoVaR and the unconditional financial system VaR, ΔCoVaR, such measure captures the marginal contribution of a particular institution to the overall systemic risk. Although, ΔCoVaR, does not measures the contribution of an institution to the overall risk, it is important from the systemic risk perspective and contribution as it captures the expected participation of institutions

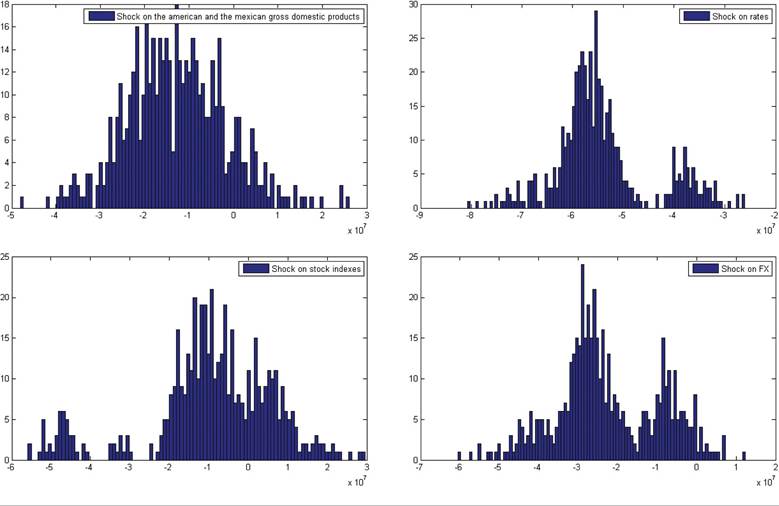

Figure 10. Losses under stress scenarios

Figure 11. The distribution of losses for the system and the distribution of the system given that bank B3 is in distress

Figure 12. The distribution of losses for the system and the distribution of the system given that bank B2 is in distress

Figure 13. The distribution of losses for the system and the distribution of the system given that bank B1 is in distress

in systemic events, which are the relevant events in the study of systemic risk.

Finally, from our experience and given that there is not a proper counterfactual available to compute other systemic risk measures; this measure could represent the best option for measuring the contribution to the systemic risk by financial institutions, computed either by estimating the SDL or by quantile regression. This measure, ΔCoVaR, is a tractable alternative to focusing on several different measures, which can be difficult to combine.

3.3.

More on the topic Systemic Relevance of Financial Institutions:

- References

- COUNTERPARTY SYSTEMIC RISK

- References

- THE THEORY AND PRACTICE OF EMPIRE-BUILDING

- CONCLUSION

- DIRECT INTERVENTIONS IN MODERN TIMES

- The indeterminate mapping from economic principles to institutional arrangements

- INTRODUCTION

- The Implementation of the 1993 Constitution

- Implementation