The indeterminate mapping from economic principles to institutional arrangements

Here is another thought experiment. Imagine a Western economist was invited to Beijing in 1978 in order to advise the Chinese leadership on a reform strategy. What would she recommend and why?

The economist would recognize that reform must start in the rural areas since the vast majority of the poor live there.

An immediate recommendation would be the liberalization of agricultural markets and the abolition of the state order system under which peasants had to make obligatory deliveries of crops at low, state-controlled prices. But since price liberalization alone would be inadequate to generate the appropriate supplyTable 4

The logic of the Washington Consensus and a Chinese Counterfactual

| Problem | Solution |

| Low agricultural productivity ---------- | —→ Price liberalization |

| Production incentives | —→ Land privatization |

| Loss of fiscal revenues | —→ Tax reform |

| Urban wages ----- | —→ Corporatization |

| Monopoly | —→ Trade liberalization |

| Enterprise restructuring | —→ Financial sector reform |

| Unemployment ----- | —→ Social safety nets |

| ... and so on |

incentives under a system of communal land ownership, the economist would also recommend the privatization of land. Next, the economist would have to turn her attention to the broader implications of price liberalization in agriculture.

Without access to cheap grains, the state would be left without a source of implicit tax revenue, so tax reform must be on the agenda as well. And in view of the rise of food prices, there must be a way to respond to urban workers’ demand for higher wages. State enterprises in urban areas must be corporatized, so that their managers are in a position to adjust their wages and prices appropriately.But now there are other problems that need attention. In an essentially closed and non-competitive economy, price-setting autonomy for the state behemoths entails the exercise of monopoly power. So the economist would likely recommend trade liberalization in order to “import” price discipline from abroad. Openness to trade in turn calls for other complementary reforms. There must be financial sector reform so that financial intermediaries are able to assist domestic enterprises in the inevitable adjustments that are called forth. And of course there must be social safety nets in place so that those workers who are temporarily displaced have some income support during the transition.

The story can be embellished by adding other required reforms, but the message ought to be clear. By the time the Western economist is done, the reform agenda she has formulated looks very similar to the Washington Consensus (see Table 4). The economist’s reasoning is utterly plausible, which underscores the point that the Washington Consensus is far from silly: it is the result of systematic thinking about the multiple, often complementary reforms needed to establish property rights, put market incentives to work, and maintain macroeconomic stability. But while this particular reform program represents a logically consistent way achieving these end goals, it is not the only one that has the potential of doing so. In fact, in view of the administrative and political constraints that such an ambitious agenda is likely to encounter, it is not implausible that there would be better ways of getting there.

How can we be sure of this? We know this because China took a very different approach to reform - one that was experimental in nature and relied on a series of institutional innovations that departed significantly from Western norms. What is important to realize about these innovations is that in the end they delivered - for a period of a couple of decades at least - the very same goals that the Western economist would have been hoping for: market-oriented incentives, property rights, macroeconomic stability. But they did so in a peculiar fashion that, given the Chinese historical and political context, had numerous advantages.

For example, the Chinese authorities liberalized agriculture only at the margin while keeping the plan system intact. Farmers were allowed to sell surplus crops freely at a market-determined price only after they had fulfilled their obligations to the state under the state order system. As Lau, Qian and Roland (2000) explain, this was an ingenious system that generated efficiency without creating any losers. In particular, it was a shortcut that neatly solved a conundrum inherent in wholesale liberalization: how to provide microeconomic incentives to producers while insulating the central government from the fiscal consequences of liberalization. As long as state quotas were set below the fully liberalized market outcome (so that transactions were conducted at market prices at the margin) and were not ratcheted up (so that producers did not have to worry about the quotas creeping up as a result of marketed surplus), China’s dual-track reform in effect achieved full allocative efficiency. But it entailed a different infra-marginal distribution - one that preserved the income streams of initial claimants. The dual track approach was eventually employed in other areas as well, such as industrial goods (e.g. coal and steel) and labor markets (employment contracts). Lau, Qian and Roland (2000) argue that the system was critical to achieve political support for the reform process, maintain its momentum, and minimize adverse social implications.

Another important illustration comes from the area of property rights. Rather than privatize land and industrial assets, the Chinese government implemented novel institutional arrangements such as the Household Responsibility System (under which land was “assigned” to individual households according to their size) and Township and Village Enterprises (TVEs). The TVEs were the growth engine of China until the mid- 1990s [Qian (2003)], with their share in industrial value added rising to more than 50 percent by the early 1990s [Lin, Cai andLi (1996, p. 180)], so they deserve special comment. Formal ownership rights in TVEs were vested not in private hands or in the central government, but in local communities (townships or villages). Local governments were keen to ensure the prosperity of these enterprises as their equity stake generated revenues directly for them. Qian (2003) argues that in the environment characteristic of China, property rights were effectively more secure under direct local government ownership than they would have been under a private property-rights legal regime. The efficiency loss incurred due to the absence of private control rights was probably outweighed by the implicit security guaranteed by local government control. It is difficult to explain otherwise the remarkable boom in investment and entrepreneurship generated by such enterprises.

Qian (2003) discusses other examples of “transitional institutions” China employed to fuel economic growth - fiscal contracts between central and local governments, anonymous banking - and one may expand his list by including arrangements such as Special Economic Zones. The main points to take from this experience are the following. First, China relied on highly unusual, non-standard institutions. Second, these unorthodox institutions worked precisely because they produced orthodox results, namely market-oriented incentives, property rights, macroeconomic stability, and so on. Third, it is hard to argue, in view of China’s stupendous growth, that a more standard, “best-practice” set of institutional arrangements would have necessarily done better.

The Chinese experience helps lay out the issues clearly because its institutional innovations and growth performance are both so stark. But China’s experience with non-standard growth policies is hardly unusual; in fact it is more the rule than the exception. The (other) East Asian anomalies noted previously (Table 3) can be viewed as part of the same pattern: non-standard practices in the service of sound economic principles. I summarize a few non-Chinese illustrations in Table 5.

Consider for example the case of financial controls. I noted earlier that few of the successful East Asian countries undertook much financial liberalization early on in their development process. Interest rates remained controlled below market-clearing levels and competitive entry (by domestic or foreign financial intermediaries) was typically blocked. It is easy to construct arguments as to why this was beneficial from an economic standpoint. Table 5 summarizes the story laid out by Hellmann, Murdock and Stiglitz (1997), who coin the term “financial restraint” for the Asian model. Where asymmetric information prevails and the level of savings is sub-optimal, Hellman et al. argue that creating a moderate amount of rents for incumbent banks can generate useful incentives. These rents induce banks to do a better job of monitoring their borrowers (since there is more at stake) and to expand effort to mobilize deposits (since there are rents to be earned on them). The quality and level of financial intermediation can both be higher than under financial liberalization. These beneficial effects are more likely to materialize when the pre-existing institutional landscape has certain properties - for example when the state is not “captured” by private interests and the external capital account is restricted (see last two columns of Table 5). When these preconditions are in place, the economic logic behind financial restraint is compelling.

The second illustration in Table 5 comes from South Korea’s and Taiwan’s experiences with industrial policy.

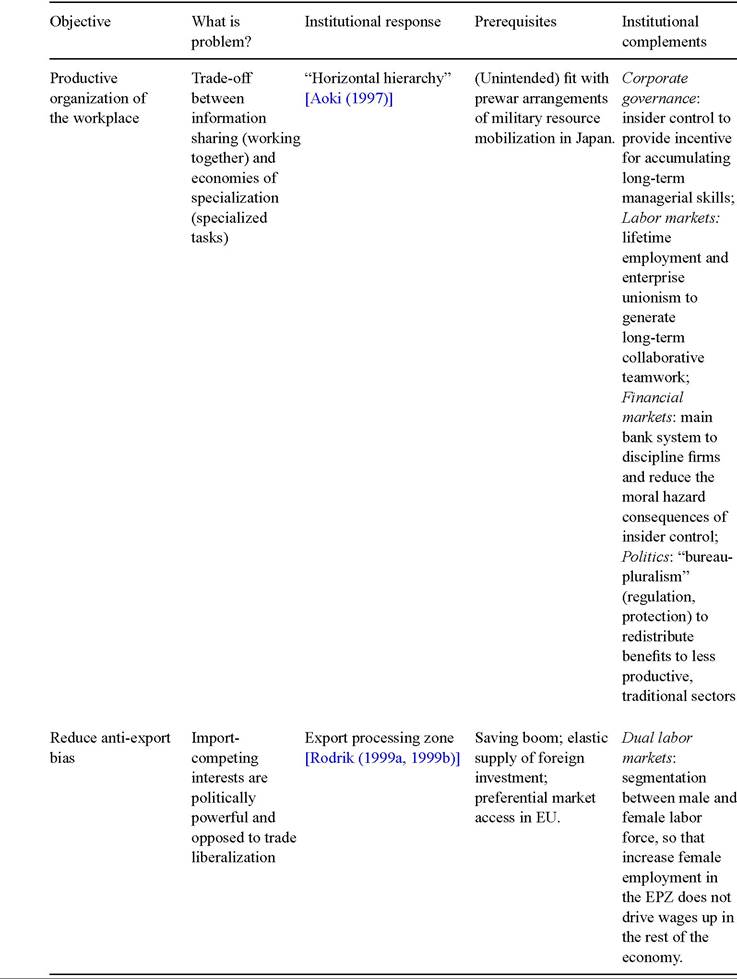

The governments in these countries rejected the standard advice that they take an arm’s length approach to their enterprises and actively sought to coordinate private investments in targeted sectors. Once again, it is easy to come up with economic models that provide justification for this approach. InRodrik (1995), I argued that the joint presence of scale economies and inter-industry linkages can depress the private return to investment in non-traditional activities below the social return. Industrial policy can be viewed as a “coordination device” to stimulate socially profitable investments. In particular, the socialization of investment risk through implicit bailout guarantees may be economically beneficial despite the obvious moral hazard risk it poses. However, once again, there are certain prerequisites and institutional complements that have to be in place for this approach to make sense (see Table 5).The third illustration in Table 5 refers to Japan and concerns the internal organization of the workplace, drawing on Aoki’s (1997) work. Aoki describes the peculiar institutional foundations of Japan’s postwar success as having evolved from a set of

Table 5

How to understand/rationalize institutional anomalies: four illustrations

Table 5 (Continued)

arrangements originally designed for wartime mobilization and centralized control of resources. He presents Japan’s team-centered approach to work organization and its redistribution of economic resources from advanced to backward sectors - arrangements that he terms “horizontal hierarchy” and “bureau-pluralism”, respectively - as solutions to particular informational and distributive dilemmas the Japanese economy faced in the aftermath of World War II. Unlike the previous authors, however, he views this fit between institutions and economic challenges as having been unintended and serendipitous.

Lest the reader think this is solely an East Asian phenomenon, an interesting example of institutional innovation comes from Mauritius [Rodrik (1999a)]. Mauritius owes a large part of its success to the creation in 1970 of an export-processing zone (EPZ), which enabled an export boom in garments to European markets. Yet, instead of liberalizing its trade regime across the board, Mauritius combined this EPZ with a domestic sector that was highly protected until the mid-1980s, a legacy of the policies of import-substituting industrialization (ISI) followed during the 1960s. The industrialist class that had been created with these policies was naturally opposed to the opening up of the trade regime. The EPZ scheme provided a neat way around this difficulty [Wellisz and Saw (1993)]. The creation of the EPZ generated new profit opportunities, without taking protection away from the import-substituting groups. The segmentation of labor markets was particularly crucial in this regard, as it prevented the expansion of the EPZ (which employed mainly female labor) from driving wages up in the rest of the economy, and thereby disadvantaging import-substituting industries. New profit opportunities were created at the margin, while leaving old opportunities undisturbed. At a conceptual level, the story here is essentially very similar to the two-track reforms in China described earlier. To produce the results it did, however, the EPZ also needed a source of investible funds, export-oriented expertise, and market access abroad, which were in turn provided by a terms-of-trade boom, entrepreneurs from Hong Kong, and preferential market access in Europe, respectively [Rodrik (1999a); Subramanian and Roy (2003)].

In reviewing cases such as these, there is always the danger of reading too much into them after the fact. In particular, we need to avoid several fallacies. First, we cannot simply assume that institutions take the form that they do because of the functions that they perform (the functionalist fallacy). Aoki’s account of Japan is a particularly useful reminder that a good fit between form and function might be the unintended consequence of historical forces. Second, it is not correct to ascribe the positive outcomes in the cases just reviewed only to their anomalies (the ex-post rationalization fallacy). Many accounts of East Asian success emphasize the standard elements - fiscal conservatism, investment in human resources, and export orientation [see for example World Bank (1993)]. As I will discuss below, East Asian institutional anomalies have often produced perverse results when employed in other settings. And it is surely not the case that all anomalies are economically functional.

The main point I take from these illustrations is robust to these fallacies, and has to do with the “plasticity” of the institutional structure that neoclassical economics is capable of supporting. All of the above institutional anomalies are compatible with, and can be understood in terms of, neoclassical economic reasoning (“good economics”). Neoclassical economic analysis does not determine the form that institutional arrangements should or do take. What China’s case and other examples discussed above demonstrate is that the higher-order principles of sound economic management do not map into unique institutional arrangements.

In fact, principles such as appropriate incentives, property rights, sound money, and fiscal solvency all come institution-free. We need to operationalize them through a set of policy actions. The experiences above show us that there may be multiple ways of packing these principles into institutional arrangements. Different packages have different costs and benefits depending on prevailing political constraints, levels of administrative competence, and market failures. The pre-existing institutional landscape will typically offer both constraints and opportunities, requiring creative shortcuts or bold experiments. From this perspective, the “art” of reform consists of selecting appropriately from a potentially infinite menu of institutional designs.

A direct corollary of this line of argument is that there is only a weak correspondence between the higher-order principles of neoclassical economics and the specific policy recommendations in the standard list (as enumerated in Table 2). To see this, consider for example one of the least contentious recommendations in the list, having to do with trade liberalization. Can the statement “trade liberalization is good for economic performance” be derived from first principles of neoclassical economics? Yes, but only if a number of side conditions are met:

• The liberalization must be complete or else the reduction in import restrictions must take into account the potentially quite complicated structure of substitutability and complementarity across restricted commodities.[568]

• There must be no microeconomic market imperfections other than the trade restrictions in question, or if there are some, the second-best interactions that are entailed must not be adverse.[569]

• The home economy must be “small” in world markets, or else the liberalization must not put the economy on the wrong side of the “optimum tariff”.[570]

• The economy must be in reasonably full employment, or if not, the monetary and fiscal authorities must have effective tools of demand management at their disposal.

• The income redistributive effects of the liberalization should not be judged undesirable by society at large, or if they are, there must be compensatory tax-transfer schemes with low enough excess burden.[571]

• There must be no adverse effects on the fiscal balance, or if there are, there must be alternative and expedient ways of making up for the lost fiscal revenues.

• The liberalization must be politically sustainable and hence credible so that economic agents do not fear or anticipate a reversal.[572]

All these theoretical complications could be sidestepped if there were convincing evidence that in practice trade liberalization systematically produces improved economic performance. But even for this relatively uncontroversial policy, it has proved difficult to generate unambiguous evidence [see Rodriguez and Rodrik (2001), Vamvakidis (2002), and Yanikkaya (2003)].[573]

The point is that even the simplest of policy recommendations - “liberalize foreign trade” - is contingent on a large number of judgment calls about the economic and political context in which it is to be implemented.[574] Suchjudgment calls are often made implicitly. Rendering them explicit has a double advantage: it warns us about the potential minefields that await the standard recommendations, and it stimulates creative thinking on alternatives (as in China) that can sidestep those minefields. By contrast, when the policy recommendation is made unconditionally, as in the Washington Consensus, the gamble is that the policy’s prerequisites will coincide with our actual draw from a potentially large universe of possible states of the world.

I summarize this discussion with the help of Tables 6, 7, and 8 dealing with microeconomic policy, macroeconomic policy, and social policy, respectively. Each table contains three columns. The first column displays the ultimate goal that is targeted by the policies and institutional arrangements in the three domains. Hence microeconomic policies aim to achieve static and dynamic efficiency in the allocation of resources. Macroeconomic policies aim for macroeconomic and financial stability. Social policies target poverty reduction and social protection.

The next column displays some of the key higher-order principles that economic analysis brings to the table. Allocative efficiency requires property rights, the rule of

Table 6

Sound economics and institutional counterparts: microeconomics

| Objective | Universal principles | Plausible diversity in institutional arrangements |

| Productive efficiency | Property rights: Ensure potential and | What type of property rights? Private, |

| (static and dynamic) | current investors can retain the returns | public, cooperative? |

| to their investments. | What type of legal regime? Common | |

| Incentives: Align producer incentives | law? Civil law? Adopt or innovate? | |

| with social costs and benefits. | What is the right balance between | |

| Rule of law: Provide a transparent, | decentralized market competition and | |

| stable and predictable set of rules. | public intervention? | |

| Which types of financial institutions/corporate governance are most appropriate for mobilizing domestic savings? | ||

| Is there a public role to stimulate technology absorption and generation (e.g. IPR “protection”)? | ||

| Table 7 | ||

| Sound economics and institutional counterparts: macroeconomics | ||

| Objective | Universal principles | Plausible diversity in institutional arrangements |

| Macroeconomic and | Sound money: Do not generate liquidity | How independent should the central bank |

| financial stability | beyond the increase in nominal money | be? |

| demand at reasonable inflation. | What is the appropriate exchange-rate | |

| Fiscal sustainability: Ensure public debt | regime (dollarization, currency board, | |

| remains “reasonable” and stable in | adjustable peg, controlled float, pure | |

| relation to national aggregates. | float)? | |

| Prudential regulation: Prevent financial | Should fiscal policy be rule-bound, and if | |

| system from taking excessive risk. | so what are the appropriate rules? | |

| Size of the public economy. | ||

| What is the appropriate regulatory apparatus for the financial system? | ||

| What is the appropriate regulatory treatment of capital account transactions? | ||

Table 8

Sound economics and institutional counterparts: social policy

| Objective | Universal principles | Plausible diversity in institutional arrangements |

| Distributive justice and | Targeting: Redistributive programs | How progressive should the tax system |

| poverty alleviation | should be targeted as closely as possible | be? |

| to the intended beneficiaries. | Should pension systems be public or | |

| Incentive compatibility: Redistributive programs should minimize incentive | private? | |

| distortions. | What are the appropriate points of intervention: Educational system? Access to health? Access to credit? Labor markets? Tax system? | |

| What is the role of “social funds”? | ||

| Redistribution of endowments (land reform, endowments-at-birth)? | ||

| Organization of labor markets: decentralized or institutionalized? | ||

| Modes of service delivery: NGOs, participatory arrangements, etc. |

law, and appropriate incentives. Macroeconomic and financial stability requires sound money, fiscal solvency, and prudential regulation. Social inclusion requires incentive compatibility and appropriate targeting. These are the “universal principles” of sound economic management. They are universal in the sense that it is hard to see what any country would gain by systematically defying them. Countries that have adhered to these principles - no matter how unorthodox their manner of doing so may have been - have done well while countries that have flouted them have typically done poorly.

From the standpoint of policy makers, the trouble is that these universal principles are not operational as stated. In effect, the answers to the real questions that preoccupy policy makers - how far should I go in opening up my economy to foreign competition, should I free up interest rates, should I rely on payroll taxes or the VAT, and the others listed in the third column of each table - cannot be directly deduced from these principles. This opens up space for a multiplicity of institutional arrangements that are compatible with the universal, higher-order principles.

These tables clarify why the standard recommendations (Table 2) correlate poorly with economic performance around the world. The Washington Consensus, in its various forms, has tended to blur the line that separates column 2 from column 3. Policy advisors have been too quick in jumping from the higher-order principles in column 2 to taking unconditional stands on the specific operational questions posed in column 3. And as their policy advice has yielded disappointing results, they have moved on to recommendations with even greater institutional specificity (as with “second generation reforms”). As a result, sound economics has often been delivered in unsound form.

I emphasize that this argument is not one about the advantages of gradualism over shock therapy. In fact, the set of ideas I have presented are largely orthogonal to the long-standing debate between the adherents of the two camps [see for example Lipton and Sachs (1990), Aslund, Boone and Johnson (1996), Williamson and Zagha (2002)]. The strategy of gradualism presumes that policy makers have a fairly good idea of the institutional arrangements that they want to acquire ultimately, but that for political and other reasons they can proceed only step-by-step in that direction. The argument here is that there is typically a large amount of uncertainty about what those institutional arrangements are, and therefore that the process that is required is more one of “search and discovery” than one of gradualism. The two strategies may coincide when policy changes reveal information and small-scale policy reforms have a more favorable ratio of information revelation to risk of failure.[575] But it is best not to confuse the two strategies. What stands out in the real success cases, as I will further illustrate below, is not gradualism per se but an unconventional mix of standard and non-standard policies well attuned to the reality on the ground.

4.