Back to the real world

Previously we had asked our Martian to interpret economic performance in the real world from the lens of the standard reform agenda. Suppose we now remove the constraint and ask him to summarize the stylized facts as he sees them.

Here is a list of four stylized facts that he may come up with.4.1. In practice, growth spurts are associated with a narrow range of policy reforms

One of the most encouraging aspects of the comparative evidence on economic growth is that it often takes very little to get growth started. To appreciate the point, it is enough to turn to Table 9, which lists 83 cases of growth accelerations. The table shows all cases of significant growth accelerations since the mid-1950s that can be identified statistically. The definition of a growth acceleration is the following: an increase in an economy’s per-capita GDP growth of 2 percentage points or more (relative to the previous 5 years) that is sustained over at least 8 years. The timing of the growth acceleration is determined by fitting a spline centered on the candidate break years, and selecting the break that maximizes the fit of the equation [see Hausmann, Pritchett and Rodrik (2004) for details on the procedure].[576]

Mostof the usual suspects are included in the table: for example Taiwan 1961, Korea 1962, Indonesia 1967, Brazil 1967, Mauritius 1971, China 1978, Chile 1986, Uganda 1989, Argentina 1990, and so on. But the exercise also yields a large number of much less well-known cases, such as Egypt 1976 or Pakistan 1979. In fact, the large number of countries that have managed to engineer at least one instance of transition to high growth may appear as surprising. As I will discuss later, most of these growth spurts have eventually collapsed. Nonetheless, an increase in growth of 2 percent (and typically more) over the better part of a decade is nothing to sneer at, and it is worth asking what produces it.

In the vast majority of the cases listed in Table 9, the “shocks” (policy or otherwise) that produced the growth spurts were apparently quite mild. Asking most development economists about the policy reforms of Pakistan in 1979 or Syria in 1969 would draw a blank stare. This reflects the fact that not much reform was actually taking pace in these cases. Relatively small changes in the background environment can yield significant increase in economic activity.

Even in the well-known cases, policy changes at the outset have been typically modest. The gradual, experimental steps towards liberalization that China undertook in the late 1970s were discussed above. South Korea’s experience in the early 1960s was similar. The military government led by Park Chung Hee that took power in 1961 did not have strong views on economic reform, except that it regarded economic development as its key priority. It moved in a trial-and-error fashion, experimenting at first with various public investment projects. The hallmark reforms associated with the Korean miracle, the devaluation of the currency and the rise in interest rates, came in 1964 and fell far short of full liberalization of currency and financial markets. As these instances illustrate, an attitudinal change on the part of the top political leadership towards a more market-oriented, private-sector-friendly policy framework often plays as large a role as the scope of policy reform itself (if not larger). Perhaps the most important example of this can be found in India: such an attitudinal change appears to have had a particularly important effect in the Indian take-off of the early 1980s, which took place a full decade before the liberalization of 1991 [DeLong (2003); Rodrik and Subramanian (2004)].

This is good news because it suggests countries do not need an extensive set of institutional reforms in order to start growing. Instigating growth is a lot easier in practice than the standard recipe, with its long list of action items, would lead us to believe.

This should not be surprising from a growth theory standpoint. When a country is so far below its potential steady-state level of income, even moderate movements in the right direction can produce a big growth payoff. Nothing could be more encouraging to policy makers, who are often overwhelmed and paralyzed by the apparent need to undertake policy reforms on a wide and ever-expanding front.Table 9

Episodes of rapid growth by region, decade and magnitude of acceleration

| Region | Decade | Country | Year | Growth before | Growth after | Difference in growth |

| Sub- | 1950s and | NGA | 1967 | -1.7 | 7.3 | 9.0 |

| Saharan | 1960s | BWA | 1969 | 2.9 | 11.7 | 8.8 |

| Africa | GHA | 1965 | -0.1 | 8.3 | 8.4 | |

| GNB | 1969 | -0.3 | 8.1 | 8.4 | ||

| ZWE | 1964 | 0.6 | 7.2 | 6.5 | ||

| COG | 1969 | bgcolor=white>0.95.4 | 4.5 | |||

| NGA | 1957 | 1.2 | 4.3 | 3.0 | ||

| 1970s | MUS | 1971 | -1.8 | 6.7 | 8.5 | |

| TCD | 1973 | -0.7 | 7.3 | 8.0 | ||

| CMR | 1972 | -0.6 | 5.3 | 5.9 | ||

| COG | 1978 | 3.1 | 8.2 | 5.1 | ||

| UGA | 1977 | -0.6 | 4.0 | 4.6 | ||

| LSO | 1971 | 0.7 | 5.3 | 4.6 | ||

| RWA | 1975 | 0.7 | 4.0 | 3.3 | ||

| MLI | 1972 | 0.8 | 3.8 | 3.0 | ||

| MWI | 1970 | 1.5 | 3.9 | 2.5 | ||

| 1980s and | GNB | 1988 | -0.7 | 5.2 | 5.9 | |

| 1990s | MUS | 1983 | 1.0 | 5.5 | 4.4 | |

| UGA | 1989 | -0.8 | 3.6 | 4.4 | ||

| MWI | 1992 | -0.8 | 4.8 | 5.6 | ||

| South Asia | 1950s/1960s | PAK | 1962 | -2.4 | 4.8 | 7.1 |

| 1970s | PAK | 1979 | 1.4 | 4.6 | 3.2 | |

| LKA | 1979 | 1.9 | 4.1 | 2.2 | ||

| 1980s | IND | 1982 | 1.5 | 3.9 | 2.4 | |

| East Asia | 1950s and | THA | 1957 | -2.5 | 5.3 | 7.8 |

| 1960s | KOR | 1962 | 0.6 | 6.9 | 6.3 | |

| IDN | 1967 | -0.8 | 5.5 | 6.2 | ||

| SGP | 1969 | 4.2 | 8.2 | 4.0 | ||

| TWN | 1961 | 3.3 | 7.1 | 3.8 | ||

| 1970s | CHN | 1978 | 1.7 | 6.7 | 5.1 | |

| MYS | 1970 | 3.0 | 5.1 | 2.1 | ||

| 1980s and | MYS | 1988 | 1.1 | 5.7 | 4.6 | |

| 1990s | THA | 1986 | 3.5 | 8.1 | 4.6 | |

| PNG | 1987 | 0.3 | 4.0 | 3.7 | ||

| KOR | 1984 | 4.4 | 8.0 | 3.7 | ||

| IDN | 1987 | 3.4 | 5.5 | 2.1 | ||

| CHN | 1990 | 4.2 | 8.0 | 3.8 |

Table 9

(Continued)

| Region | Decade | Country | Year | Growth before | Growth after | Difference in growth |

| Latin | 1950s and | DOM | 1969 | -1.1 | 5.5 | 6.6 |

| America | 1960s | BRA | 1967 | 2.7 | 7.8 | 5.1 |

| and | PER | 1959 | 0.8 | 5.2 | 4.4 | |

| Caribbean | PAN | 1959 | 1.5 | 5.4 | 3.9 | |

| NIC | 1960 | 0.9 | 4.8 | 3.8 | ||

| ARG | 1963 | 0.9 | 3.6 | 2.7 | ||

| COL | 1967 | 1.6 | 4.0 | 2.4 | ||

| 1970s | ECU | 1970 | 1.5 | 8.4 | 6.8 | |

| PRY | 1974 | 2.6 | 6.2 | 3.7 | ||

| TTO | 1975 | 1.9 | 5.4 | 3.5 | ||

| PAN | 1975 | 2.6 | 5.3 | 2.7 | ||

| URY | 1974 | 1.5 | 4.0 | 2.6 | ||

| 1980s and | CHL | 1986 | -1.2 | 5.5 | 6.7 | |

| 1990s | URY | 1989 | 1.6 | 3.8 | 2.1 | |

| HTI | 1990 | -2.3 | 12.7 | 15.0 | ||

| ARG | 1990 | -3.1 | 6.1 | 9.2 | ||

| DOM | 1992 | 0.4 | 6.3 | 5.8 | ||

| Middle | 1950s and | MAR | 1958 | -1.1 | 7.7 | 8.8 |

| East and | 1960s | SYR | 1969 | 0.3 | 5.8 | 5.5 |

| North | TUN | 1968 | 2.1 | 6.6 | 4.5 | |

| Africa | ISR | 1967 | 2.8 | 7.2 | 4.4 | |

| ISR | 1957 | 2.2 | 5.3 | 3.1 | ||

| 1970s | JOR | 1973 | -3.6 | 9.1 | 12.7 | |

| EGY | 1976 | -1.6 | 4.7 | 6.3 | ||

| SYR | 1974 | 2.6 | 4.8 | 2.2 | ||

| DZA | 1975 | 2.1 | 4.2 | 2.1 | ||

| 1980s and 1990s | SYR | 1989 | -2.9 | 4.4 | 7.3 | |

| OECD | 1950s and | ESP | 1959 | 4.4 | 8.0 | 3.5 |

| 1960s | DNK | 1957 | 1.8 | 5.3 | 3.5 | |

| JPN | 1958 | 5.8 | 9.0 | 3.2 | ||

| USA | 1961 | 0.9 | 3.9 | 3.0 | ||

| CAN | 1962 | 0.6 | 3.6 | 2.9 | ||

| IRL | 1958 | 1.0 | 3.7 | 2.7 | ||

| BEL | 1959 | 2.1 | 4.5 | 2.4 | ||

| NZL | 1957 | 1.5 | 3.8 | 2.4 | ||

| AUS | 1961 | 1.5 | 3.8 | 2.3 | ||

| FIN | 1958 | 2.7 | 5.0 | 2.2 | ||

| FIN | 1967 | 3.4 | 5.6 | 2.2 | ||

| 1980s and | PRT | 1985 | 1.1 | 5.4 | 4.3 | |

| 1990s | ESP | 1984 | 0.1 | 3.8 | 3.7 | |

| IRL | 1985 | 1.6 | 5.0 | 3.4 | ||

| GBR | 1982 | 1.1 | 3.5 | 2.5 | ||

| FIN | 1992 | 1.0 | 3.7 | 2.8 | ||

| NOR | 1991 | 1.4 | 3.7 | 2.2 |

Source: Hausmann, Pritchett and Rodrik (2004).

4.2.

The policy reforms that are associated with these growth transitions typically combine elements of orthodoxy with unorthodox institutional practicesNo country has experienced rapid growth without minimal adherence to what I have termed higher-order principles of sound economic governance - property rights, market-oriented incentives, sound money, fiscal solvency. But as I have already argued, these principles were often implemented via policy arrangements that are quite unconventional. I illustrated this using examples such as China’s two-track reform strategy, Mauritius’ export processing zone, and South Korea’s system of “financial restraint”.

It is easy to multiply the examples. When Taiwan and South Korea decided to reform their trade regimes to reduce anti-export bias, they did this not via import liberalization (which would have been a Western economist’s advice) but through selective subsidization of exports. When Singapore decided to make itself more attractive to foreign investment, it did this not by reducing state intervention but by greatly expanding public investment in the economy and through generous tax incentives [Young (1992)]. Botswana, which has an admirable record with respect to macroeconomic stability and the management of its diamond wealth, also has one of the largest levels of government spending (in relation to GDP) in the world. Chile, a country that is often cited as a paragon of virtue by the standard check list, has also departed from it in some important ways: it has kept its largest export industry (copper) under state ownership; it has maintained capital controls on financial inflows through the 1990s; and it has provided significant technological, organizational, and marketing assistance to its fledgling agro-industries.

In all these instances, standard desiderata such as market liberalization and outward orientation were combined with public intervention and selectivity of some sort. The former element in the mix ensures that any economist so inclined can walk away from the success cases with a renewed sense that the standard policy recommendations really “work”.

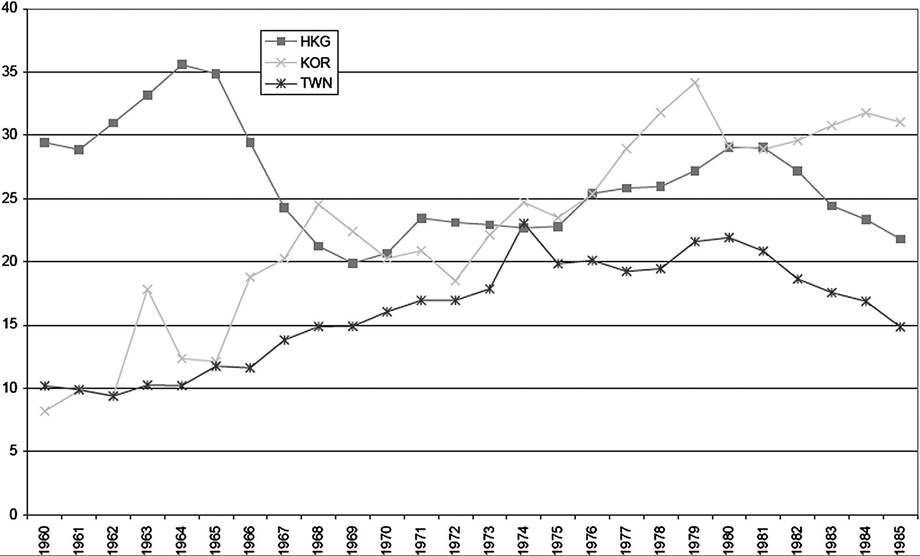

Most egregiously, China’s success is often attributed to its turn towards market - which is largely correct - and then with an unjustified leap of logic is taken as a vindication of the standard recipe - which is largely incorrect. It is not clear how helpful such evaluations are when so much of what these countries did is unconventional and fits poorly with the standard agenda.[577]It is difficult to identify cases of high growth where unorthodox elements have not played a role. Hong Kong is probably the only clear-cut case. Hong Kong’s government has had a hands-off attitude towards the economy in almost all areas, the housing market being a major exception. Unlike Singapore, which followed a free trade policy but otherwise undertook extensive industrial policies, Hong Kong’s policies have been as close to laissez-faire as we have ever observed. However, there were important prerequisites to Hong Kong’s success, which illuminate once again the context-specificity of growth strategies. Most important, Hong Kong’s important entrepot role in trade, the strong institutions imparted by the British, and the capital flight from communist China had already transformed the city-state into a high investment, high entrepreneurship economy by the late 1950s. As Figure 3 shows, during the early 1960s Hong Kong’s investment rate was more than three times higher than that in South Korea or Taiwan. The latter two economies would not reach Hong Kong’s 1960 per-capita GDP until the early 1970s.[578] Hence Hong Kong did not face the same challenge that Taiwan, South Korea, and Singapore did to crowd in private investment and stimulate entrepreneurship.

It goes without saying that not all unorthodox remedies work. And those that work sometimes do so only for a short while. Consider for example Argentina’s experiment in the 1990s with a currency board. Most economists would consider a currency board regime as too risky for an economy of Argentina’s size insofar as it prevents expenditure switching via the exchange rate.

(Hong Kong has long operated a successful marketing board.) However, as the Argentinean economy began to grow rapidly in the first half of the 1990s, many analysts altered their views. Had the Asian crisis of 1997-1998 and the Brazilian devaluation of 1999 not forced Argentina off its currency board, it would have been easy to construct a story ex post about the virtues of the currency board as a growth strategy. The currency board sought to counteract the effects of more than a century of financial mismanagement through monetary discipline. It was a shortcut aimed at convincing foreign and domestic investors that the rules of the game had changed irrevocably. Under better external circumstances, the credibility gained might have more than offset the disadvantages. The problem in this case was the unwillingness to pull back from the experiment even when it became clear that the regime had left the Argentine economy with a hopelessly uncompetitive real exchange rate. The lesson is that institutional innovation requires a pragmatic approach which avoids ideological lock-in.4.3. Institutional innovations do not travel well

The more discouraging aspect of the stylized facts is that the policy packages associated with growth accelerations - and particularly the elements therein that are non-standard - tend to vary considerably from country to country. China’s two-track strategy of reform differs significantly from India’s gradualism. South Korea’s and Taiwan’s more protectionist trade strategy differs markedly from the open trade policies of Singapore (and Hong Kong). Even within strategies that look superficially similar, closer look reveals large variation. Taiwan and South Korea both subsidized non-traditional industrial activities, but the former did it largely through tax incentives and the latter largely through directed credit.[579]

Figure 3. Investment as a share of GDP in East Asia.

Ch. 14: GrowthStrategies 995

Attempts to emulate successful policies elsewhere often fail. When Gorbachev tried to institute a system similar to China’s Household Responsibility System and two-track pricing in the Soviet Union during the mid- to late-1980s, it produced few of the beneficial results that China had obtained.[580] Most developing countries have export processing zones of one kind or another, but few have been as successful as the one in Mauritius. Import-substituting industrialization (ISI) worked in Brazil, but not in Argentina.[581]

In light of the arguments made earlier, this experience should not be altogether surprising. Successful reforms are those that package sound economic principles around local capabilities, constraints and opportunities. Since these local circumstances vary, so do the reforms that work. An immediate implication is that growth strategies require considerable local knowledge. It does not take a whole lot of reform to stimulate economic growth - that is the good news. The bad news is that it may be quite difficult to identify where the binding constraints or promising opportunities lie. A certain amount of policy experimentation may be required in order to discover what will work. China represents the apotheosis of this experimental approach to reform. But it is worth noting that many other instances of successful reform were preceded by failed experiments. In South Korea, President Park’s developmental efforts initially focused on the creation of white elephant industrial projects that ultimately went nowhere [Soon (1994, pp. 2728)]. In Chile, Pinochet’s entire first decade can be viewed as a failed experiment in “global monetarism”.

Economists can have a useful role to play in this process: they can identify the sources of inefficiency, describe the relevant trade offs, figure out general-equilibrium implications, predict behavioral responses, and so on. But they can do these well only if their analysis is adequately embedded within the prevailing institutional and political reality. The hard work needs to be done at home.

4.4. Sustaining growth is more difficult than igniting it, and requires more extensive institutional reform

The main reason that few of the growth accelerations listed in Table 9 are etched in the consciousness of development economists is that most of them did not prove durable. In fact, as discussed earlier, over the last four decades few countries except for a few East Asian ones have steadily converged to the income levels of the rich countries. The vast majority of growth spurts tend to run out of gas after a while. The experience of Latin America since the early 1980s and the even more dramatic collapse of SubSaharan Africa are emblematic of this phenomenon. In a well-known paper, Easterly et al. (1993) were the first to draw attention to a related finding, namely the variability in growth performance across time periods. The same point is made on a broader historical canvas by Goldstone (in preparation).

Hence growth in the short- to medium-term does not guarantee success in the longterm. A plausible interpretation is that the initial reforms need to be deepened over time with efforts aimed at strengthening the institutional underpinning of market economies. It would be nice if a small number of policy changes - which, as argued above, is what produces growth accelerations - could produce growth over the longer term as well, but this is obviously unrealistic. I will discuss some of the institutional prerequisites of sustained growth in greater detail later in the paper. But the key to longer-term prosperity, once growth is launched, is to develop institutions that maintain productive dynamism and generate resilience to external shocks.

For example, the growth collapses experienced by many developing countries in the period from the mid-1970s to the early 1980s seem to be related mainly to the inability to adjust to the volatility exhibited by the external environment at that time. In these countries, the effects of terms-of-trade and interest-rate shocks were magnified by weak institutions of conflict management [Rodrik (1999b)]. This, rather than the nature of microeconomic incentive regimes in place (e.g., import substituting industrialization), is what caused growth in Africa and Latin America to grind to a halt after the mid- 1970s and early 1980s (respectively). The required macroeconomic policy adjustments set off distributive struggles and proved difficult to undertake. Similarly, the weakness of Indonesia’s institutions explains why that country could not extricate itself from the 1997-1998 East Asian financial crisis [see Temple (2003)], while South Korea, for example, did a rapid turnaround. These examples are also a warning that continued growth in China cannot be taken for granted: without stronger institutions in areas ranging from financial markets to political governance, the Chinese economy may well find itself having outgrown its institutional underpinnings.[582]

5.