A two-pronged growth strategy

As the evidence discussed above reveals, growth accelerations are feasible with minimal institutional change. The deeper and more extensive institutional reforms needed for long-term convergence take time to implement and mature.

And they may not be the most effective way to raise growth at the outset because they do not directly target the most immediate constraints and opportunities facing an economy. At the same time, such institutional reforms can be much easier to undertake in an environment of growth rather than stagnation. These considerations suggest that successful growth strategies are based on a two-pronged effort: a short-run strategy aimed at stimulating growth, and a medium- to long-run strategy aimed at sustaining growth.[583] The rest of this section takes these up in turn.5.1. An investment strategy to kick-start growth

From the standpoint of economic growth, the most important question in the short run for an economy stuck in a low-activity equilibrium is: how do you get entrepreneurs excited about investing in the home economy? “Invest” here has to be interpreted broadly, as referring to all the activities that entrepreneurs undertake, such as expanding capacity, employing new technology, producing new products, searching for new markets, and so on. As entrepreneurs become energized, capital accumulation and technological change are likely to go hand in hand - too entangled with each other to separate out cleanly.

What sets this process into motion? There are two kinds of views on this in the literature. One approach emphasizes the role of government-imposed barriers to entrepreneurship. In this view, policy biases towards large and politically-connected firms, institutional failures (in the form of licensing and other regulatory barriers, inadequate property rights and contract enforcement), and high levels of policy uncertainty and risk create dualistic economic structures and repress entrepreneurship.

The removal of the most egregious forms of these impediments is then expected to unleash a flurry of new investments and entrepreneurship. According to the second view, the government has to play a more pro-active role than simply getting out of the private sector’s way: it needs to find means of crowding in investment and entrepreneurship with some positive inducements. In this view, economic growth is not the natural order of things, and establishing a fair and level playing field may not be enough to spur productive dynamism. The two views differ in the importance they attach to prevailing, irremovable market imperfections and their optimism with regard to governments’ ability to design and implement appropriate policy interventions.5.1.1. Government failures

A good example of the first view is provided by the strategy of development articulated in Stern (2001). In a deliberate evocation of Hirschman’s (1958) book, Stern outlines an approach with two pillars: building an appropriate “investment climate” and “empowering poor people”. The former is the relevant part of his approach in this context. Stern defines “investment climate” quite broadly, as “the policy, institutional, and behavioral environment, both present and expected, that influences the returns and risks associated with investment” [Stern (2001, pp. 144-145)]. At the same time, he recognizes the need for priorities and the likelihood that these priorities will be context specific. He emphasizes the favorable dynamics that are unleashed once a few, small things are done right.

In terms of actual policy content, Stern’s illustrations make clear that he views the most salient features of the investment climate to be government-imposed imperfections: macroeconomic instability and high inflation, high government wages that distort the functioning of labor markets, a large tax burden, arbitrary regulations, burdensome licensing requirements, corruption, and so on. The strategy he recommends is to use enterprise surveys and other techniques to uncover which of these problems bite the most, and then to focus reforms on the corresponding margin.

Similar perspectives can be found in Johnson, McMillan and Woodruff (2000), Friedman et al. (2000), and Aslund and Johnson (2003). Besley and Burgess (2002a) provide evidence across Indian states on the productivity depressing effects of labor market regulations. The title of Shleifer and Vishny’s (1998) book aptly summarizes the nature of the relevant constraint in this view: The Grabbing Hand: Government Pathologies and Their Cures.5.1.2. Market failures

The second approach focuses not on government-imposed constraints, but on market imperfections inherent in low-income environments that block investment and entrepreneurship in non-traditional activities. In this view, economies can get stuck in a low-level equilibrium due to the nature of technology and markets, even when government policy does not penalize entrepreneurship. There are many versions of this latter approach, and some of the main arguments are summarized in the taxonomy presented in Table 10. I distinguish here between stories that are based on learning spillovers (a non-pecuniary externality) and those that are based on market-size externalities induced by scale economies. See also the useful discussion of these issues in Ocampo (2003), which takes a more overtly structuralist perspective.

Table 10

Ataxonomy of “natural” barriers to industrialization

A. Learning externalities

1. Learning-by-doing [e.g., Matsuyama (1992)]

2. Human capital externalities [e.g., Azariadis and Drazen (1990)]

3. Learning about costs [e.g., Hausmann and Rodrik (2002)]

1. Wage premium in manufacturing [e.g., Murphy, Shleifer and Vishny (1989)]

2. Infrastructure [e.g., Murphy, Shleifer and Vishny (1989)]

3. Specialized intermediate inputs [e.g., Rodrik (1991, 1995)]

4. Spillovers associated with wealth distribution [e.g., Hoff and Stiglitz (2001)]

As Acemoglu, Aghion and Zilibotti (2002) point out, two types of learning are relevant to economic growth: (a) adaptation of existing technologies; and (b) innovation to create new technologies.

Early in the development process, the kind of learning that matters the most is of the first type. There are a number of reasons why such learning can be subject to spillovers. There may be a threshold level of human capital beyond which the private return to acquiring skills becomes strongly positive [as in Azariadis and Drazen (1990)]. There may be learning-by-doing which is either external to individual firms, or cannot be properly internalized due to imperfections in the market for credit [as in Matsuyama (1992)]. Or there may be learning about a country’s own cost structure, which spills over from the incumbents to later entrants [as in Hausmann and Rodrik (2002)]. In all these cases, the relevant learning is under-produced in a decentralized equilibrium, with the consequence that the economy fails to diversify into non-traditional, more advanced lines of activity.[584] There then exist policy interventions that can improve matters. With standard externalities, the first-best takes the form of a corrective subsidy targeted at the relevant distorted margin. In practice, revenue, administrative or informational constraints may make resort to second-best interventions inevitable.For example, Hausmann and Rodrik (2002) suggest a carrot-and-stick strategy to deal with the learning barrier to industrialization that they identify. In that model, costs of production in non-traditional activities are uncertain, and they are revealed only after an upfront investment by an incumbent. Once that initial investment is made, the cost information becomes public knowledge. Entrepreneurs engaged in the cost discovery process incur private costs, but provide social benefits that can vastly exceed their anticipated profits. The first-best policy here, which is an entry subsidy, suffers from an inextricable moral hazard problem. Subsidized entrants have little incentive to engage subsequently in costly activities to discover costs. A second-best approach takes the form of incentives contingent on good performance.

Hausmann and Rodrik (2002) evaluate East Asian and Latin American industrial policies from this perspective. They argue that East Asian policies were superior in that they effectively combined incentives with discipline. The former was provided through subsidies and protection, while the latter was provided through government monitoring and the use of export performance as a productivity yardstick. Latin American firms under import substituting industrialization (ISI) received considerable incentives, but faced very little discipline. In the 1990s, these same firms arguably faced lots of discipline (exerted through foreign competition), but little incentives. This line of argument provides one potential clue to the disappointing economic performance of Latin America in the 1990s despite a much improved “investment climate” according to the standard criteria.The second main group of stories shown in Table 10 relates to the existence of coordination failures induced by scale economies. The big-push theory of development, articulated first by Rosenstein-Rodan (1943) and formalized by Murphy, Shleifer and Vishny (1989), is based on the idea that moving out of a low-level steady state requires coordinated and simultaneous investments in a number of different areas. A general formulation of such models can be provided as follows. Let the level of profits in a given modern-sector activity depend on n, the proportion of the economy that is already engaged in modern activities: πm(n), with dπm(n)∕dn > 0. Let profits in traditional activities be denoted πt. Suppose modern activities are unprofitable for an individual entrant if no other entrepreneur already operates in the modern sector, but highly profitable if enough entrepreneurs do so: πm(0) < πt and πm(1) > πt. Then n = 0 and n = 1 are both possible equilibria, and industrialization may never take hold in an economy that starts with n = 0.

The precise mechanism that generates profit functions of this form depends on the model in question. Murphy, Shleifer and Vishny (1989) develop models in which the complementarity arises from demand spillovers across final goods produced under scale economies or from bulky infrastructure investments. Rodriguez- Clare (1996), Rodrik (1996a, 1996b), and Trindade (2003) present models in which the effect operates through vertical industry relationships and specialized intermediate inputs. Hoff and Stiglitz (2001) discuss a large class of models with coordination failure characteristics.The policy implications of such models can be quite unconventional, requiring the crowding in of private investment through subsidization, jawboning, public enterprises and the like. Despite the “big push” appellation, the requisite policies need not be wide-ranging. For example, socializing investment risk through implicit investment guarantees, a policy followed in South Korea, is welfare enhancing in Rodrik’s (1996a) framework because it induces simultaneous entry into the modern sector. It is also costless to the government, because the guarantees are never called on insofar as the resulting investment boom pays for itself. Hence, when successful, such policies will leave little trail on government finances or elsewhere.[585]

Both types of models listed in Table 10 suggest that the propagation of modern, non-traditional activities is not a natural process and that it may require positive inducements. One such inducement that has often worked in the past is a sizable and sustained depreciation of the real exchange rate. For a small open economy, the real exchange rate is defined as the relative price of tradables to non-tradables. In practice, this price ratio tends to move in tandem with the nominal exchange rate, the price of foreign currency in terms of home currency. Hence currency devaluations (supported by appropriate monetary and fiscal policies) increase the profitably of tradable activities across the board. From the current perspective, this has a number of distinct advantages. Most of the gains from diversification into non-traditional activities are likely to lie within manufactures and natural resource based products (i.e., tradables) rather than services and other nontradables. Second, the magnitude of the inducement can be quite large, since sustained real depreciations of 50 percent or more are quite common. Third, since tradable activities face external competition, the activities that are encouraged tend to be precisely the ones that face the greatest market discipline. Fourth, the manner in which currency depreciation subsidizes tradable activities is completely market-friendly, requiring no micromanagement on the part of bureaucrats. For all these reasons, a credible, sustained real exchange rate depreciation may constitute the most effective industrial policy there is.

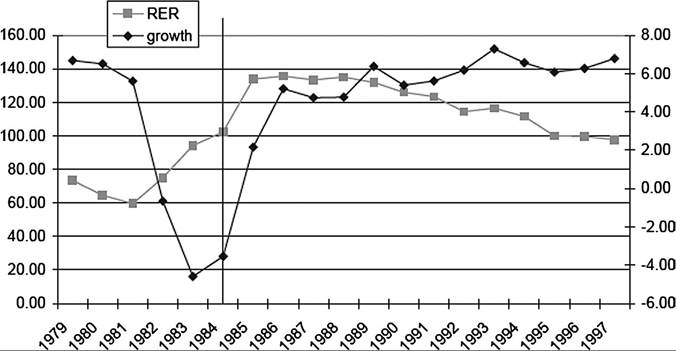

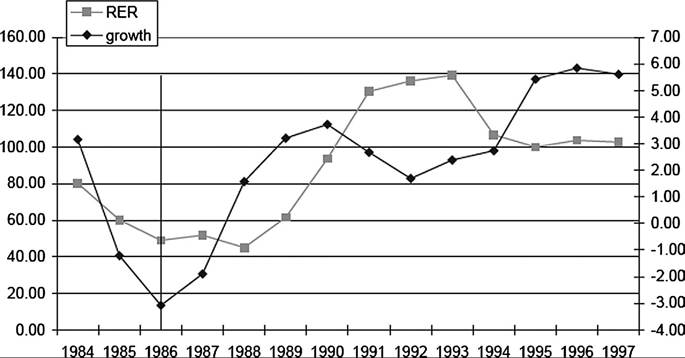

Large real exchange rate changes have played a big role in some of the more recent growth accelerations. Figure 4 shows two well-known cases: Chile and Uganda since the mid-1980s. In both cases, a substantial swing in relative prices in favor of tradables accompanied the growth take-off. In Chile, the more than doubling of the real exchange rate following the crisis of 1982-1983 (the deepest in Latin America at the time) is commonly presumed to have played an instrumental role in promoting diversification into non-traditional exports and stimulating economic growth. It is worth noting that import tariffs were raised significantly as well (during 1982-1985), giving importsubstituting activities an additional boost. As the bottom panel of Figure 3 shows, the depreciation in Uganda was even larger. These depreciations are unlikely to have been the result of growth, since growth typically generates an appreciation of the real exchange rate through the Balassa-Samuelson effect. By contrast, large real depreciations did not play a major role in early growth accelerations in East Asia during the 1960s [Rodrik (1997)].[586]

5.1.3. Where to start?

The two sets of views outlined above - the government failure and market failure approaches - can help frame policy discussions and identify important ways of thinking about policy priorities in the short run. The most effective point of leverage for stimulating growth obviously depends on local circumstances. It is tempting to think that the right first step is to remove government-imposed obstacles to entrepreneurial activity before worrying about “crowding in” investments through positive inducements. But this may not always be a better strategy. Certainly when inflation is in triple digits or the regulatory framework is so cumbersome that it stifles any private initiative, removing these distortions will be the most sensible initial step. But beyond that, it is difficult to say in general where the most effective margin for change lies. Asking businessmen their views on the priorities can be helpful, but not decisive. When learning spillovers and coordination failures block economic take-off, enterprise surveys are unlikely to be revealing unless the questions are very carefully crafted to elicit relevant responses.

(a)

(b)

Figure 4. Real exchange rate and per-capita GDP growth shown as 3-year moving average in (a) Chile and (b) Uganda.

Hausmann, Rodrik and Velasco (2004) outline a framework for undertaking “growth diagnostics”, i.e., targeting reforms on the most binding constraints on economic growth.

One of the lessons of recent economic history is that creative interventions can be remarkably effective even when the “investment climate”, judged by standard criteria, is pretty lousy. South Korea’s early reforms took place against the background of a political leadership that was initially quite hostile to the entrepreneurial class.[587] China’s TVEs have been stunningly successful despite the absence of private property rights and an effective judiciary. Conversely, the Latin American experience of the 1990s indicates that the standard criteria do not guarantee an appropriate investment climate. Governments can certainly deter entrepreneurship when they try to do too much; but they can also deter entrepreneurship when they do too little.

It is sometimes argued that heterodoxy requires greater institutional strength and therefore lies out of reach of most developing countries. But the evidence does not provide much support for this view. It is true that the selective interventions I have discussed in the case of South Korea and Taiwan were successful in part due to unusual and favorable circumstances. But elsewhere, heterodoxy served to make virtue out of institutional weakness. This is the case with China’s TVEs, Mauritius’ export processing zone, and India’s gradualism. In these countries, it was precisely institutional weakness that rendered the standard remedies impractical. It is in part because the standard reform agenda is institutionally so highly demanding - a fact now recognized through the addition of so-called “second generation reforms” - that successful growth strategies are so often based on unconventional elements (in their early stages at least).

It is nonetheless true that the implementation of the market failure approach requires a reasonably competent and non-corrupt government. For every South Korea, there are many Zaires where policy activism is an excuse for politicians to steal and plunder. Finely-tuned policy interventions can hardly be expected to produce desirable outcomes in setting such as the latter. And to the extent that Washington Consensus policies are more conducive to honest behavior on the part of politicians, they may well be preferable on this account. However, the evidence is ambiguous on this. Most policies, including those of the Washington Consensus type, are corruptible if the underlying political economy permits or encourages it. Consider for example Russia’s experiment with mass privatization. It is widely accepted that this process was distorted and delegitimized by asset grabs on the part of politically well-connected insiders. Washington Consensus policies themselves cannot legislate powerful rent-seekers out of existence. Rank ordering different policy regimes requires a more fully specified model of political economy than the reduced-form view that automatically associates governmental restraint with less rent-seeking.[588]

I close this section with the usual refrain: the range of strategies that have worked in the past is quite diverse. Traditional import-substituting industrialization (ISI) model was quite effective in stimulating growth in a large number of developing countries (e.g., Brazil, Mexico, Turkey). So was East Asian style outward orientation, which combined heavy-handed interventionism at home with single-minded focus on exports (South Korea, Taiwan). Chile’s post-1983 strategy was based on quite a different style of outward orientation, relying on large real depreciation, absence of explicit industrial policies (but quite a bit of support for non-traditional exports in agro-industry), saving mobilization through pension privatization, and discouragement of short-term capital inflows. The experience of countries such as China and Mauritius is best described as two-track reform. India comes as close to genuine gradualism as one can imagine. Hong Kong represents probably the only case where growth has taken place without an active policy of crowding in private investment and entrepreneurship, but here too special and favorable preconditions (mentioned earlier) limit its relevance to other settings. In view of this diversity, any statement on what ignites growth has to be cast at a sufficiently high level of generality.

5.2. An institution building strategy to sustain growth

In the long run, the main thing that ensures convergence with the living standards of advanced countries is the acquisition of high-quality institutions. The growth-spurring strategies described above have to be complemented over time with a cumulative process of institution building to ensure that growth does not run out of steam and that the economy remains resilient to shocks. This point has now been amply demonstrated both by historical accounts [North and Thomas (1973), Engerman and Sokoloff (1994)] and by econometric studies [Hall and Jones (1999), Acemoglu, Johnson and Robinson (2001), Rodrik, Subramanianand Trebbi (2002), Easterly and Levine (2002)]. However, these studies tend to remain at a very aggregate level of generality and do not provide much policy guidance [a point that is also made in Besley and Burgess (2002b)].

The empirical research on national institutions has generally focused on the protection of property rights and the rule of law. But one should think of institutions along a much wider spectrum. In its broadest definition, institutions are the prevailing rules of the game in society [North (1990)]. High quality institutions are those that induce socially desirable behavior on the part of economic agents. Such institutions can be both informal (e.g., moral codes, self-enforcing agreements) and formal (legal rules enforced through third parties). It is widely recognized that the relative importance of formal institutions increases as the scope of market exchange broadens and deepens. One reason is that setting up formal institutions requires high fixed costs but low marginal costs, whereas informal institutions have high marginal costs [Li (1999); Dixit (2004, Chapter 3)]. I will focus here on formal institutions.

What kind of institutions matter and why? Table 11 provides a taxonomy of marketsustaining institutions, associating each type of institutions with a particular need. The starting point is the recognition that markets need not be self-creating, self-regulating, self-stabilizing, and self-legitimizing. Hence, the very existence of market exchange presupposes property rights and some form of contract enforcement. This is the as-

Table 11

A taxonomy of market-sustaining institutions

| Market-creating institutions | Market-regulating institutions | Market-stabilizing institutions | Market-legitimizing institutions |

| Property rights | Regulatory bodies | Monetary and fiscal institutions | Democracy |

| Contract enforcement | Other mechanisms for correcting market failures | Institutions of prudential regulation and supervision | Social protection and social insurance |

pect of institutions that has received the most scrutiny in empirical work. The central dilemma here is that a political entity that is strong enough to establish property rights and enforce contracts is also strong enough, by definition, to violate these same rules for its own purpose [Djankov et al. (2003)]. The relevant institutions must strike the right balance between disorder and dictatorship.

As Table 11 makes clear, there are other needs as well. Every advanced economy has discovered that markets require extensive regulation to minimize abuse of market power, internalize externalities, deal with information asymmetries, establish product and safety standards, and so on. They also need monetary, fiscal, and other arrangements to deal with the business cycle and the problems of unemployment/inflation that are at the center of macroeconomists’ analyzes since Keynes. Finally, market outcomes need to be legitimized through social protection, social insurance, and democratic governance most broadly [Rodrik (2000)].

Institutional choices made in dealing with these challenges often have to strike a balance between competing objectives. The regulatory regime governing the employment relationship must trade off the gains from “flexibility” against the benefits of stability and predictability. The corporate governance regime must delineate the interests and prerogatives of shareholders and stakeholders. The financial system must be free to take risks, but not so much so that it becomes an implicit public liability. There must be enough competition to ensure static allocative efficiency, but also adequate prospect of rents to spur innovation.

The last two centuries of economic history in today’s rich countries can be interpreted as an ongoing process of learning how render capitalism more productive by supplying the institutional ingredients of a self-sustaining market economy: meritocratic public bureaucracies, independent judiciaries, central banking, stabilizing fiscal policy, antitrust and regulation, financial supervision, social insurance, political democracy. Just as it is silly to think of these as the prerequisites of economic growth in poor countries, it is equally silly not to recognize that such institutions eventually become necessary to achieve full economic convergence. In this connection, one may want to place special emphasis on democratic institutions and civil liberties, not only because they are important in and of themselves, but also because they can be viewed as metainstitutions that help society make appropriate selections from the available menu of economic institutions.

However, the earlier warning not to confuse institutional function and institutional form becomes once again relevant here. Appropriate regulation, social insurance, macroeconomic stability and the like can be provided through diverse institutional arrangements. While one can be sure that some types of arrangements are far worse than others, it is also the case that many well-performing arrangements are functional equivalents. Function does not map uniquely into form. It would be hard to explain otherwise how social systems that are so different in their institutional details as those of the United States, Japan, and Europe have managed to generate roughly similar levels of wealth for their citizens. All these societies protect property rights, regulate product, labor, and financial markets, have sound money, and provide for social insurance. But the rules of the game that prevail in the American style of capitalism are very different from those in the Japanese style of capitalism. Both differ from the European style. And even within Europe, there are large differences between the institutional arrangements in, say, Sweden and Germany. There has been only modest convergence among these arrangements in recent years, with the greatest amount of convergence taking place probably in financial market practices and the least in labor market institutions [Freeman (2000)].

There are a number of reasons for institutional non-convergence. First, differences in social preferences, say over the trade-off between equity and opportunity, may result in different institutional choices. If Europeans have a much greater preference for stability and equity than Americans, their labor market and welfare-state arrangements will reflect that preference. Second, complementarities among different parts of the institutional landscape can generate hysteresis and path dependence. An example of this would be the complementarity between corporate governance and financial market practices of the Japanese “model”, as discussed previously. Third, the institutional arrangements that are required to promote economic development can differ significantly, both between rich and poor countries and among poor countries. This too has been discussed previously.

There is increasing recognition in the economics literature that high-quality institutions can take a multitude of forms and that economic convergence need not necessarily entail convergence in institutional forms [North (1994), Freeman (2000), Pistor (2000), Mukand and Rodrik (2005), Berkowitz, Pistor and Richard (2003), Djankov et al. (2003), Dixit (2004)].[589] North (1994, p. 8) writes: “Economies that adopt the formal rules of another economy will have very different performance characteristics than the first economy because of different informal norms and enforcement [with the implication that] transferring the formal political and economic rules of successful Western economies to third-world and Eastern European economies is not a sufficient condition for good economic performance.” Freeman (2000) discusses the variety of labor market institutions that prevail among the advanced countries and argues that differences in these practices have first-order distributional effects, but only second-order efficiency effects. Pistor (2000) provides a general treatment of the issue of legal transplantation, and shows how importation of laws can backfire. In related work, Berkowitz, Pistor and Richard (2003) find that countries that developed their formal legal orders internally, adapted imported codes to local conditions, or had familiarity with foreign codes ended up with much better legal institutions than those that simply transplanted formal legal orders from abroad. Djankov et al. (2003) base their discussion on an “institutional possibility frontier” that describes the trade-off between private disorder and dictatorship, and argue that different circumstances may call for different choices along this frontier. And [Dixit (2004, p. 4)] summarizes the lessons for developing countries thus: “it is not always necessary to create replicas of western style state legal institutions from scratch; it may be possible to work with such alternative institutions as are available, and build on them.”

Mukand and Rodrik (2005) develop a formal model to examine the costs and benefits of institutional “experimentation” versus “copycatting” when formulas that have proved successful elsewhere may be unsuitable at home. A key idea is that institutional arrangements that prove successful in one country create both positive and negative spillovers for other countries. On the positive side, countries whose underlying conditions are sufficiently similar to those of the successful “leaders” can imitate the arrangements prevailing there and forego the costs of experimentation. This is one interpretation of the relative success that transition economies in the immediate vicinity of the European Union have experienced. Countries such as Poland, the Czech Republic or the Baltic republics share a similar historical trajectory with the rest of Europe, have previous experience with capitalist market institutions, and envisaged full EU membership within a reasonable period [De Menil (2003)]. The wholesale adoption of EU’s acquis communautaire may have been the appropriate institution-building strategy for these countries. On the other hand, countries may be tempted or forced to imitate institutional arrangements for political or other reasons, even when their underlying conditions are too dissimilar for the strategy to make sense.[590] Institutional copycatting may have been useful for Poland, but it is much less clear that it was relevant or practical for Ukraine or Kyrgyzstan. The negative gradient in the economic performance of transition economies as one moves away from Western Europe provides some support for this idea [see Mukand and Rodrik (2005)].

Even though it is recent, this literature opens up a new and exciting way of looking at institutional reform. In particular, it promises an approach that is less focused on so-called best practices or the superiority of any particular model of capitalism, and more cognizant of the context-specificity of desirable institutional arrangements. Dixit’s (2004) monograph outlines a range of theoretical models that help structure our thinking along these lines.

6.