COUNTERPARTY SYSTEMIC RISK

Counterparty systemic risk appears where a failure of an individual or a cluster5 of counterparties impact a great majority of the other counterparties that are directly or indirectly linked.

This implication can range from the downgrade of a credit rating to a credit default event, which can result in a collapse of the entire value of credit portfolios. As we have observed, during the crisis of 2007/8, the great majority of portfolios had significant losses which were due to downgrading rather than to default events. However, what should we consider in systemic risk portfolio value and liquidity analysis and where do market counterparty and behavior characteristics play a role?In counterparty systemic risk analysis, the degree of correlations among counterparties in regards to their credit worthiness (expressed as credit ratings) should be identified. In

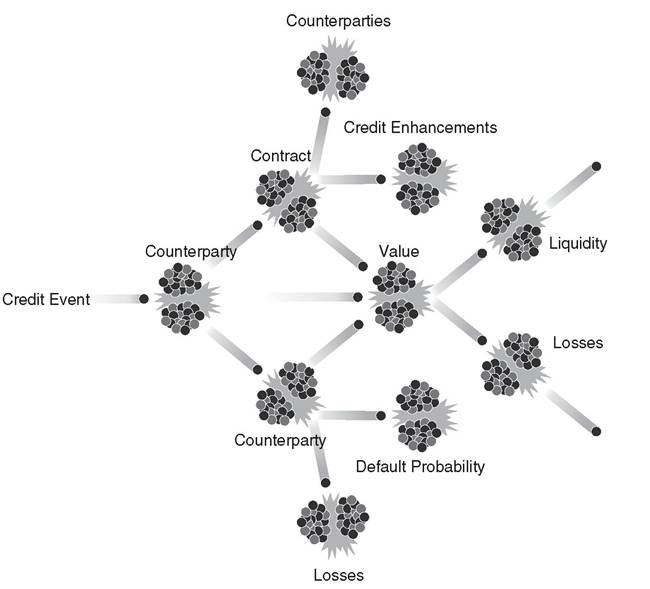

FIGURE 11.3 A credit event, e.g., default, in an exposure may cause a chain systemic risk reaction

such correlation analysis we need to identify whether and how an event of a counterparty's downgrades or defaults will influence the degree of other counterparties' credit rating. The most applicable way of performing such analysis is to consider the common and correlated market risk factors where counterparties are linked. This linkage is defined by analyzing the counterparties' sensitivities to these factors as discussed in Chapter 7. Typically, such factors are market indices, e.g., referring to the business sectors, currency, etc., to which the counterparty belongs. Thus, we should also consider the corresponding volatilities and correlations among these market risk factors. In addition, the idiosyncratic sensitivities, which indicate the level of the counterparty's strength to have the least sensitivity with the index factors, are also considered.

Sensitivity profiles are behavior driven parameters and they are defined based on statistical observations together with expertise assumptions; thus, they are subject to change in the future.Counterparties can be interlinked and interdependent of an event on a single counterparty or cluster of counterparties. This may systematically cause credit events on the other counterparties and exposures that they are linked to. As we already know in a loan contract, we typically need to consider three types of counterparties: the investor (the lender), the obligor (the borrower), and the guarantor or protection seller.

When counterparties default or downgrade, there is an expected impact on the value and size of the net exposures, the degree of expected credit losses, and the credit rating of the counterparties that are linked to it. For instance, as soon as a counterparty of a bond downgrades or defaults, the actual bond decrease in value and expected losses rise; moreover, the credit event may also impact those counterparties that are directly or indirectly linked to this bond. Let us now look at the chain reactions that may happen in the case of a default and the downgrading of counterparty credit events:

■ Contracts linked to the counterparty default event will lose value whereas the expected cash flows will be cancelled out. Any other counterparties that may be linked to these contracts (via joint accounts or acting as guarantors) will also be affected. If such contracts are used as credit enhancement, such as financial collateral, to other exposures their corresponding net value will be changed accordingly.

■ The net exposures of the financial instruments linked to the defaulted guarantor or protection seller will be increased.

■ Counterparties linked to the defaulted or downgraded counterparty may increase their default probability and the expected losses of the contracts they are linked to.

As illustrated in Figure 11.4, the two main views of systemic risk for counterparties are based on identifying the linkages in regards to credit exposures and to other counterparties.

FIGURE 11.4 A credit event, e.g., default, in an exposure may cause a chain reaction of systemic risk

The former is based on exposure analysis of counterparties whereas the latter focuses on their allocation within the markets.

We can estimate the future correlation of the counterparties and corresponding systemic risk by simulating the evolution of the performance of assets and their sensitivity profiles. In such a process, one may simulate the market evolution in the future. We can do this with what-if market scenarios or by throwing the dice for the market conditions by applying Monte Carlo stochastic processes. Then, via the market correlations and sector sensitivities, one can determine the new ratings of the counterparties. A more advanced approach can be applied if, for the future time steps, one also throws the dice or deterministically changes the future ratings of a particular counterparty or a group of counterparties. In this dynamic analysis of the systemic risks, the new (future) counterparties and market conditions (sectors and indices) can also be considered.

11.3