CREDIT EXPOSURE SYSTEMIC RISK

Interlinkages and interdependencies of credit exposures can cause systemic risk. This can arise when a credit event of a single exposure or cluster1 of exposures, causes cascading credit events that ripple through other exposures.

Credit events are the default or downgrading of the underlying counterparties linked to the credit exposure. These are the obligor of the exposure and may also be the guarantor or protection seller covering part of the exposures via counterparty credit enhancements, as we explained in Chapter 10.As we will discuss in Chapter 12 about the principles of the treasury model, banking institutions are acting as investors via their lending activities. Moreover, as we explained in Chapter 7 they are also obligors because they are borrowing capital via, for instance, interbanking and retail markets. Finally, banks can take on a third role: they may also act as guarantors and protections sellers, for example, by offering derivative products.

Exposures may default or not, but change their value due to the obligor's credit distress,

i. e., downgrading. In both cases, the defaulted or downgraded exposures may affect the value and counterparties of the credit enhancements that they are also attached to. In addition, both investors and obligors attached to these exposures suffer a sequence of losses. Finally, they may affect other exposures sharing the same counterparties or by using the defaulted or downgraded exposures as credit enhancements. The following two sections describe the main chain reactions after default and downgrading credit events.

11.1.1 Chain reactions after default credit event

A default credit event of the obligor's credit exposure may trigger the following sequence of defaults, downgrading and losses to other exposures and counterparties as is explained in more details in the following paragraphs.

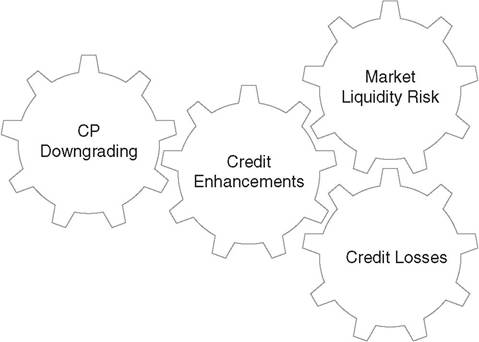

1. The credit enhancements have to be exercised; thus, considering that there is no specific wrong way risk:2

a. The asset based credit enhancements will be most likely under liquidation, at short term, covering the credit losses. Indeed, a liquidation of high volume of assets, e.g., stocks or bonds, especially under stress market conditions will influence negatively their market value. In other words, market liquidity risk may be the result, which will increase the actual net exposure and credit losses.

When those types of assets are also used as collaterals to other exposures it will directly affect their exposure at default.

Moreover, under stress market conditions, the loss of the assets' market value may influence the credit status of the underlying counterparties that they belong to. This may result in further systemic counterparty risk as the influenced counterparty will affect all other exposures that it is linked to.

b. In the counterparty-based credit enhancements, the guarantor or protection seller will be asked to cover the credit losses. These losses may impact any other exposures that the guarantor or protection seller may be linked to. In other words, they may negatively influence their credit rating which can result in higher risk and expected credit losses.

Overall, as illustrated in Figure 11.1, the systemic elements of credit enhancements are the counterparties, market liquidity and credit losses.

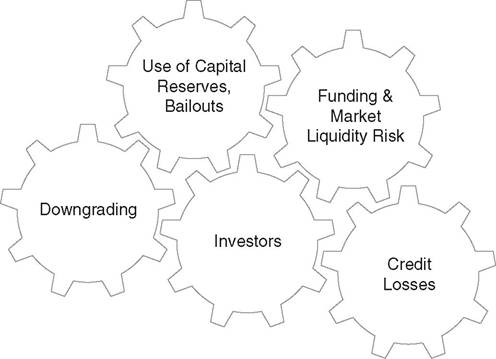

2. In the event of credit default, the investors (e.g., lenders) will have a credit loss equal to the loss given default as explained in Chapter 9. However, where the recovery is negligible or is not expected within a short term, the credit loss is equal to the net exposure, i.e., EAD defined in Chapter 9. Moreover, the defaulted exposure will result in funding liquidity risk, discussed in Chapter 12, due to the cancelation of the contractual expected cash flows.

Banks are not only acting as investors but also as obligors to other exposures. Thus, the losses in value and liquidity of the defaulted contract that they are exposed to, may influence their capability to fulfil their future obligations, i.e., against the outstanding loans and/or derivative contracts that they are committed to.

In such cases, banks have to use their own capital buffers3 liquidating their own assets, which may affect their market value. Where such a buffer is not sufficient, the bank may default or get downgraded, which impacts systemically all of its outstanding exposures and credit enhancements which they are linked to. Such distress will also influence the continuity of the future

FIGURE 11.1 Credit enhancements are linked counterparties, market liquidity and credit losses

business and relative credit exposures. Most possibly however, financial institutions are getting bailouts, for avoiding default but not downgrading events, which turns to systemic risk and loss distribution within the markets,4 i.e., exposing markets to the defaulted credit portfolios.

Figure 11.2 illustrates the systemic elements referring to investors.

3. The obligors (e.g., the borrower) of the defaulted exposure will increase the probability to default and thus the credit spreads of the other exposures that they are linked to. As a result, the value of these exposures will be reduced. Moreover, both changes in default probability and value of the exposure will further increase the expected credit loss.

FIGURE 11.2 Systemic elements referring to investors

4. The defaulted exposures, such as bonds, may have been used as collaterals to other exposures. Thus, there will be direct impact on the linked net exposures, increasing their expected credit losses for the investor(s).

11.1.2 Chain reactions after credit downgrading

In the event of credit downgrading the probability for default and the corresponding credit spread of the credit exposure increases, whereas the actual value of the exposure is reduced. Thus, a chain of events may happen in the following ways:

1. Where such exposure, e.g., governmental or corporate bond, is used as asset-based credit enhancements the loss of value will directly impact the linked net exposures.

2. The expected credit losses, for the investors (e.g., lenders) of these downgraded exposures will be increased and therefore there is a need for more capital adequacy/buffer that may be used against these losses; this may introduce the employment of limits in further exposures and business development.

In addition, if the investors are also obligors, such credit distress will possibly increase the default probability causing possible further impact to all credit exposures that are linked to.

3. The increase in default probabilities and spreads implies that the obligor is downgraded. Thus all other exposures linked to such an obligor will increase the probability of default, credit spreads and expected credit losses, and reduce the market value of these exposures.

4. Any counterparty based credit enhancements (e.g., credit derivatives) will be exercised against value change of the exposure due to the rise of credit spread (downgrading event). Thus, the protection sellers, who may also be playing the role of obligor, may go through financial distress.

The analysis of systemic risk, based on credit events, may be a complex exercise, as it involves most financial analysis elements, as illustrated in Figure 11.3. However, it is very important for managing efficiently the credit exposures and ensuring robustness of the entire financial system against financial risks.

11.2