The Demand for MBSs and ABS-CDOs

The evidence I have presented shows that from 2003 to 2007, the largest financial institutions dramatically increased their participation in the origination and securitization of nonconventional mortgages, and most financial institutions were also large-scale investors in the securities they produced.

The evidence also shows that the largest of these institutions that were not integrated into the nonconventional origination market by 2003 did so by 2007. There are two remaining pieces of the puzzle. First, I want to return to the question of the role of the demand for MBSs and CDOs in this process. Second, I want to consider how investors were funding these purchases by borrowing money from the asset-backed commercial paper (ABCP) market.I have presented some statements from the business press and executives at some of the financial institutions that it was the high level of demand for MBSs and CDOs that caused them to double down to find new mortgages even as the supply of mortgages was drying up after 2004. The large expansion of the mortgage market from 2000 to 2003 created the opportunity for investors to buy low- risk, relatively high-reward financial products based on conventional American mortgages. As I have shown, many of them were the same financial institutions who were originating and securitizing mortgages. The demand for these investments continued to rise from 2003 to 2008, as evidenced in Figure 5.3.

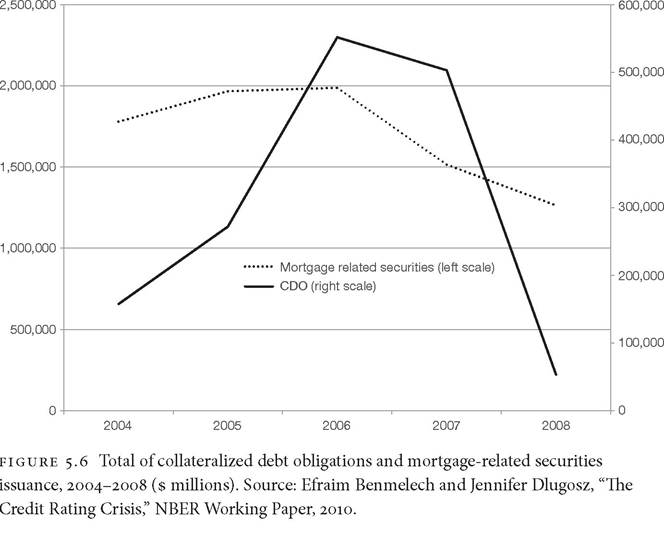

Most observers of the crisis accurately document the role of nonconventional mortgages, MBSs based on those mortgages, and the rapid expansion of ABS- CDOs, CDO-CDOs, and CDO-cubed as being responsible for most of the losses that banks suffered in the financial crisis. What has been missing in many of the accounts of the crisis is why the market moved so swiftly to nonconventional originations and MBSs based on them from 2004 to 2006 and then expanded even more rapidly into ABS-CDOs beginning in 2006-2007 (Jarrow, 2011; MacKenzie, 2011; Mian and Sufi, 2015). ABS-CDOs are securities that include

of ABS-CDOs changed, and mortgage-based products came to predominate.

The largest parts of these ABS-CDOs were made up of home equity loans, with smaller parts consisting of residential and commercial MBS tranches and other CDO tranches. Taken together, this evidence shows that the market for securities based on real estate products remained big throughout 2001-2008. As mortgages became harder to find, banks found themselves packaging whatever assets they could in order to satisfy the demand for these securities.This evidence on the continued demand for highly rated, relatively high-yield securities shows why banks were so anxious to be vertically integrated if they were not already. Simply put, they needed to secure as many mortgages as they could in order to keep their securities businesses going. This pushed them to buy originators even as the overall market for origination was slowing down. The demand for securities based on mortgages was, in the end, what kept pushing banks to originate mortgages to customers with worse and worse credit. Even as defaults and foreclosures increased in 2006 and 2007, banks worked hard to get mortgages. When that faltered, they replaced nonconventional mortgages in their securities issues with anything else they had to keep their securitization machines going. The demand was so high that hard-to-sell, lower-rated tranches of MBSs could be packaged into CDOs profitably.