The Role of the Asset-Backed Commercial Paper Market in Funding Mortgages

Many observers agree that the proximate causes of the financial crisis were the inability of banks to pay back their loans from the ABCP market and the “repo” market (Gorton, 2010; Brunnermeier, 2009; Covitz et al., 2013).

Historically, the main purpose of these markets was for banks and other firms to be able to borrow on assets for very short periods, usually from one day to one year. Banks are constantly borrowing and lending into these markets, and the same bank may actually be doing both, as one part of the bank has money to lend for a very short term and another a need for funds. Firms use these markets to borrow against accounts receivables for short-term cash and often to meet payrolls while waiting for payment for goods and services. In the case of mortgage securitization, these markets had been used since the 1980s to borrow money to purchase mortgages and pay it back when the securities that were being made from the mortgages were sold.But over time, banks came to use these short-term loans not to just to hold mortgages until their eventual sale as securities but as a source of capital to buy those securities on their own accounts. It was this business practice that put banks most at risk. By borrowing money short term to hold securities that had long maturities, banks were taking the risk that they could keep rolling over those loans or, if a problem arose, that they could not sell those securities. The meltdown in finance began in earnest when Lehman Brothers collapsed in September 2008. This collapse was caused by their inability to pay back loans to creditors in several of these markets (Swedberg, 2010). The unexpected effect of the Lehman Brothers collapse was to cause the lenders in these markets to suddenly worry about all of the loans they had made to banks holding MBSs and CDOs. This effect cascaded and became a panic that eventually brought down many of the largest banks (Covitz et al., 2013).

It is useful to describe the two most important of these markets, the repo market and the ABCP market.In the business model of the repo market, one party sells an asset (usually fixed-income securities such as Treasury bonds but also corporate bonds, MBSs, and CDOs) to another party at one price at the start of the transaction and commits to repurchase the assets from the second party at a different price at a future date (Adrian et al., 2011). If the seller defaults during the life of the repo, the buyer as the new owner can sell the asset to a third party to offset their loss. The asset therefore acts as collateral and mitigates the credit risk that the buyer has on the seller. Although assets are sold outright at the start of a repo, the commitment of the seller to buy back the assets in the future means that the buyer has only temporary use of those assets, while the seller has only temporary use of the cash proceeds of the sale. Thus, although repo is structured legally as a sale and repurchase of securities (hence the term repo), it is more like a collateralized loan or secured deposit for a loan.

The ABCP market is more complex, both in the way that assets are packaged into legal vehicles called special investment vehicles (SIVs) and in the roles of banks and other financial institutions in packaging, selling, and servicing such vehicles. The SIV is a kind of special-purpose vehicle used in the ABCP market. ABCP is typically a short-term instrument that matures between 1 and 270 days (with an average of 30 days) from issuance and is issued through the use of a legal entity called a SIV. The purpose of these vehicles is to purchase and hold financial assets from a variety of asset sellers. The purchase of the assets in the vehicle is made possible by selling asset-backed commercial paper to outside investors. The assets act as collateral for the loan. The assets, as is the case with mortgages, may also have cash flows attached to them, which accrue to the purchaser of the bonds.

The financial assets that serve as collateral for ABCP can be a mix of many different assets, mostly asset-backed securities (which could include car loans, student loans, or credit card debt), residential mortgages, commercial loans, and CDOs. Most of the assets are AAA rated, and the mixtures are jointly judged to have a low risk of bankruptcy by a rating agency. These high ratings are justified because the different assets in the SIV are diversified, and thus the risk that any one asset class will default is theoretically uncorrelated to others failing, making such packages attractive investments. Many large institutions heavily invested in these assets because they represented a very attractive investment opportunity. They benefited from high ratings from agencies and gave institutions the ability to invest cash assets safely for short periods.

As mentioned above, historically, banks used the ABCP market to help fund their purchase of mortgages that would then be made into securities. By creating a SIV, a bank could borrow money short term and then repay it when the mortgage-based securities were sold. This form of organization allowed banks to take the purchase of the mortgages off their books by creating walled-off investments (Gorton and Souleles, 2005). Thus, they did not count against the amount of capital banks had to hold. This meant that banks could borrow more to buy more mortgages and produce more securities without fear of running into limits on their ability to borrow. This made the ABCP market ideal for banks who wanted to be aggressive in taking on debt in order to take advantage of a large and expanding market for mortgages and securities based on mortgages. It also made it cheap to fund mortgage securitization.

Over time, banks began to create SIVs to obtain funds for longer-term investments, mostly made up of MBSs and CDOs. They would use the MBSs and CDOs they bought and create investment vehicles that still had the advantage of being off books.

SIVs set up by some commercial banks came to finance their longer-term, higher-yield investing through sales of ABCP. This had been very profitable when ABCP was considered safe, as ABCP buyers accepted a low interest rate. For example, one might borrow for a year in the ABCP market for 2 percent and earn 5 percent return on the MBSs and CDOs during that period. At the end of the year, one would seek to roll over the loan for another year or find a different funder.This worked only if buyers in the ABCP market continued to see the MBSs and CDOs in the SIVs as safe investments. As mortgagors began to default in 2006 and house foreclosures began to increase, the value of the MBSs and CDOs in the SIVs came into question. Moreover, since many of the SIVs contained a wide variety of assets, the buyers of assets did not really know what was in the package they were buying. Eventually, this made participants in this market become unwilling to purchase ABCP. This caused trouble for financial institutions that had relied on sales of ABCP to obtain funds for use in longer-term investments. When Lehman collapsed in September 2008, this created a panic in the

ABCP market (Covitz et al., 2013). At this point, no one knew what asset prices should be, and investors were less willing to buy or roll over ABCP. As these doubts spread, a financial panic ensued.

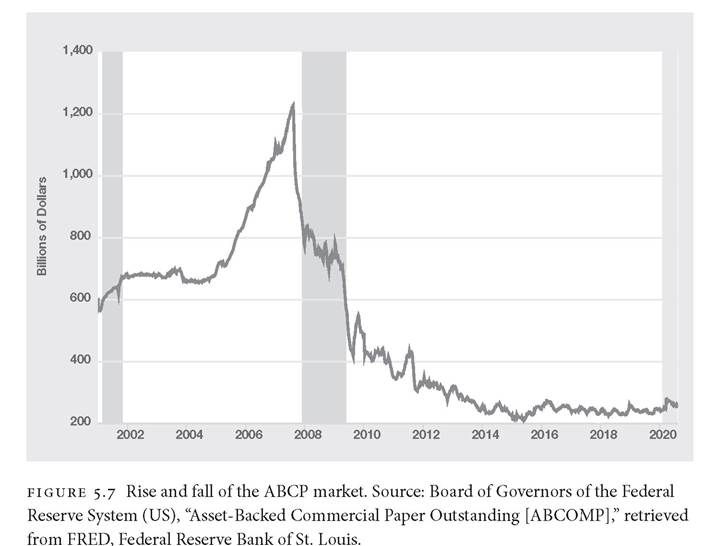

It is useful to present some data on the size of these markets and the identities of the market participants. Figure 5.7 presents data on the size of the ABCP market. Before 2004, the ABCP market was relatively stable at about $600-700 billion in transactions per year. But in the next three years, it increased to over $1.2 trillion. Almost all of this was used to fund the purchase of MBSs and CDOs. One can observe that beginning in late 2006, the ABCP market began to shrink dramatically. By the end of 2008, it returned to around $700 billion.

Essentially, all of the MBSs and CDOs that were being funded by ABCP were no longer being funded short term.We now know that this lack of funding meant that banks that held large amounts of ABCP were going to find themselves in a serious liquidity crisis, and for most, this turned into insolvency. This single figure dramatically shows why the financial crisis happened so swiftly and with such devastating consequences. Banks who were funding their MBS and CDO activities by borrowing in the ABCP market had no more than a year to figure out how to sell those assets, because continuing to borrow to hold them had become impossible. This cre-

ated a perfect storm. Since many of the MBSs and CDOs had nonconventional mortgages in them and these mortgages were starting to fail, no one knew how to value the underlying assets. As banks tried to sell these assets, they ended up quickly having to take such large losses that they went from being illiquid to being insolvent.

Acharya et al. (2013) explore the identities of firms that were involved as conduits in the ABCP market over this period.3 They show that the largest US banks who were participants included Citigroup, Bank of America, Morgan Stanley, Bear Stearns, GMAC, State Street Corporation, Lehman Brothers, and Countrywide Financial. I note that six of these eight financial entities (Citibank, Bank of America, Morgan Stanley, Bear Stearns, Lehman Brothers, and Countrywide Financial) appear in the top ten of conventional and nonconventional mortgage originators and issuers of conventional and nonconventional MBSs in Table 5.1. Not only were the largest vertically integrated originators and issuers of mortgage products large and integrated, but they inordinately relied on the ABCP market for their funding.

This last finding should not be a surprise. If a bank was going to be vertically integrated, they were going to need capital to purchase mortgages, make securities, and borrow to hold those securities on their own accounts. When Lehman Brothers collapsed, it makes sense that those banks who were deepest into the vertical integration strategy were the ones who had borrowed the most money to fund their efforts and found themselves at greatest risk. While the vertical integration strategy worked dramatically to produce record profits from 2001 to 2006, it left the banks most deeply involved with large amount of debt that was effectively hidden off books in SIVs funded by the ABCP market. This borrowing short to go long worked spectacularly well while it worked, but once the confidence in the banks that employed it most successfully was in question the bottom fell out quickly (Swedberg, 2010).