The Model

Regarding the method of analysis, in order to avoid the disadvantages presented by the models of Linear Regression and Discriminant Analysis -identified by Mures et al (2005)-, we apply the Binary Logistic Regression as a technique to propose a model whose response or dependent variable is a dummy variable with a value of zero (0) when the customer leaves the bank and operations in favour of another institution, and one (1), when otherwise the customer is loyal to his financial institution.

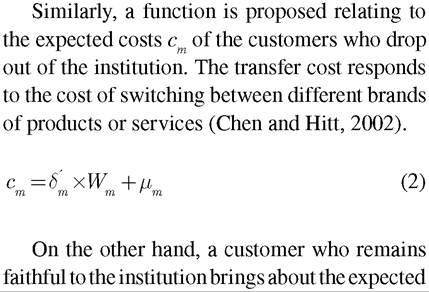

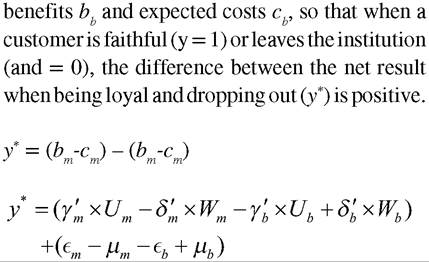

The statistical model comes from the structural random-utility model proposed by Green (1993), in which the unobserved vector (1 x N) of expected profit b for bank customers who leave is a linear function of an unobserved vector (k x 1) of coefficients ym a noticed matrix (k x N) of independent or explanatory variables Um and unobserved vector (1 x N) that collects the random disruption ş.

m

Table 4. Explanatory variables

| Variable | Concept |

| ZONE | Geographic location fo the agency or branch. Dummy variable: (0) Central Area; and (1) Outskirts. |

| PROD_NUM | Number of products that the customer has contracted with the financial institution. |

| PROF_RAT | Customer profitability ratio with the financial institution (gross income/financial products). |

| RAT_LIQUID | Customer cash ratio with the financial institution (loans/total assets). |

| PROD_CLASS | Customer classification based on their connection with products in the financial institution. Dummy variable: (0) Customer with low connection; and (1) Customer with high connection. |

| VOL_CLASS | Customer ranking based on volume of business with the bank. Dummy variable: (0) Customer with low turnover; and (1) Customer with high turnover. |

| RENT_CLASS | Customer listing based on the degree of profitability that contributes to financial institution. Dummy variable: (0) Customer that provides low profitability; and (1) Client that provides high return. |

| PAYROLL | Establish payroll direct deposit in the financial institution. Dummy variable: (0) No; and (1) Yes. |

| PENSION | Hiring a pension plan with the financial institution. Dummy variable: (0) No; and (1) Yes. |

continued on following page

Table 4. Continued

| Variable | Concept |

| DEB_CARD | Customer has contracted debit card. Dummy variable: (0) No; and (1) Yes. |

| CRED_CARD | Customer has contracted credit card. Dummy variable: (0) No; and (1) Yes. |

| DEBCARD_NUM | Number of debit cards that the client has with the financial institution during the period that he has remained a customer of the institution. |

| AGE | Age of customer at the time of evaluation. |

| GENDER | Gender of the borrower. Dummy variable: (0) Male; and (1) Female |

| MOBILE | Use of the mobile phone in banking transactions. Dummy variable :(0) No; and (1) Yes. |

| The customer has an email account. Dummy variable: (0) No; and (1) Yes. | |

| SELF-EMPLOYED | The client is independent worker. Dummy variable: (0) No; and (1) Yes. |

| YEAS AS A CLIENT | Time of the borrower as a customer of the entity. |

| E-BANK_NUM | Number of e-banking transactions of the customer. |

| E-BANK_AMOUNT | Average amount of the customer in e-banking transactions. |

| CLARITY | Level of openness of the financial institution with the customer. Categorical variable: (1) Very Dissatisfied; (2) Somewhat Dissatisfied; (3) Neutral; (4) Somewhat Satisfied; and (5) Very Satisfied. |

| AGILITY | Level of agility in the financial institution operations. Categorical variable: (1) Poor; (2) Fair; (3) Good; (4) Very Good; and (5) Excellent. |

| CONFIDENCE | Level of customer confidence in the financial institution. Categorical variable: (1) Dissatisfied; (2) Somewhat Dissatisfied; (3) Somewhat Satisfied; (4) Satisfied; and (5) Very Satisfied. |

| SECURITY | Security level that the client has when performing e-banking operations. Categorical variable: (1) Poor; (2) Fair; (3) Good; (4) Very Good; and (5) Excellent. |

| CUSTOMER SERVICE | Level of customer satisfaction regarding the customer service department. Categorical variable: (1) Strongly Disagree; (2) Disagree; (3) Neutral; (4) Agree; and (5) Strongly Agree. |

| SATISFACTION | Overall level of satisfaction that he financial institution provides. Categorical variable: (1) Very Dissatisfied; (2) Somewhat Dissatisfied; (3) Neutral; (4) Somewhat Satisfied; and (5) Very Satisfied. |

y* = β'?X + ş > 0

(3)

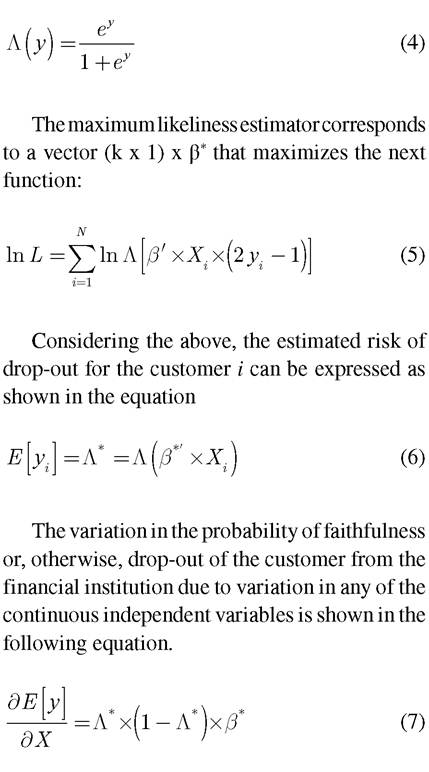

Building a logistic regression model assumes that ş takes a logistic distribution, so the cumulative distribution function can be reflected as shown in the equation.

Logistic regression supports the use of categorical variables by using dummy variables. In these cases, the variation in the estimated probability of dropping out because of a variation in a dummy variable is similar to the one calculated by means of the expression (7) (Menard, 2009).

Among the parametric techniques, the choice of Binary Logistic Regression as statistical technique is due to the large utility in the following topics gathered in the works of Eisenbeis (1981) and Lawrence and Arshadi (1995):

• Logistic regression is not as strict as linear regression regarding the performance of the strict hypothesis of linearity, normality, homoscedasticity and independence.

• The statistical properties are more suitable than the linear models, where at times inefficient estimators are obtained.

• It recognizes the categorical variables with greater flexibility than the linear models.

• It makes it possible to estimate the probability of drop-out or desertion from a financial institution, according to the values of the independent variables.

• The model determines the influence of each independent variable on the dependent variable (loyalty and abandonment) depending on the OR (Odds Ratio or advantage). This is defined as exp (β), where exp is the base of natural logarithms (a constant whose value is 2.718) and β is value of the regression parameter of the independent variable in the model. Thus, exp (β) represents the value of the odds when the explanatory variable takes the value 0; in other words, success is much more likely than failure when the explanatory variable is 0.