THE TWILIGHT OF POOLING-OF-INTERESTS ACCOUNTING

Political contributions may or may not have been what induced leaders of both major parties to become energetic lobbyists on pooling-of-interests accounting.

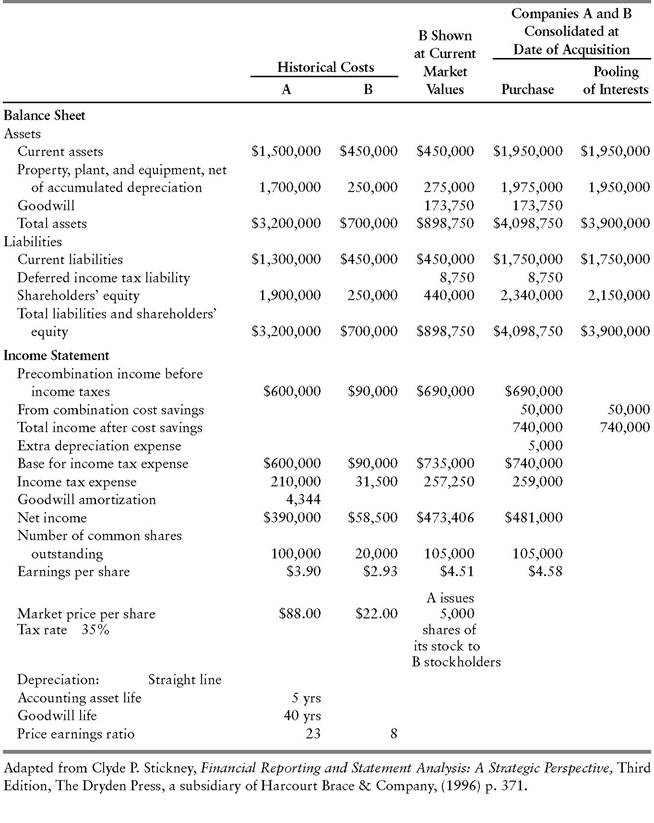

Unquestionably, however, the seemingly esoteric issue attracted attention in high places. Exhibit 10.1 helps to explain why, by detailing the alternative accounting treatments for Company A’s acquisition of Company B.Under purchase accounting, the combined companies’ balance sheet includes the acquiring company’s assets at book value (historical cost less accumulated depreciation) plus the acquired company’s assets at fair market value. In Company B’s case, fair market value exceeds book value by $198,750, representing the difference between the price paid by Company A (5,000 shares @ $88 per share = $440,000) and Company B’s shareholders’ equity ($250,000), plus $8,750 (35% of $25,000) of deferred income tax liability. Of the $198,750, the auditors allocate $25,000 to ordinary depreciable (tangible) assets, which rise from $250,000 to $275,000. The remainder, $173,750, becomes an intangible asset called goodwill, which must be amortized over a period no longer than 40 years.

In this example, we assume that the combined companies amortize the newly created goodwill over the maximum allowable period, resulting in an annual expense of $4,344. Amortization of goodwill entails no cash outlay. Neither does it generate cash through tax savings, because it is not a taxdeductible expense. The amortization does reduce reported income, however, along with the $5,000 annual depreciation (over five years) of the $25,000 write-up of Company B’s tangible assets. All told, the combined companies’ initial-post-merger-year pretax income of $740,000 ($600,000 from Company A + $90,000 from Company B + $50,000 of efficiencies gained through combining operations) is reduced by $5,000 (pretax) of new depreciation and $4,344 (after tax) of goodwill amortization.

Under pooling-of-interests accounting, by contrast, the combined balance sheet includes the assets of both Company A and Company B at book value.

There is no excess over Company B’s book value to allocate to tangible assets or goodwill, so no new depreciation or amortization arises. Taxes alone reduce the combined companies’ pretax income of $740,000. Net income, at $481,000, exceeds the $473,406 figure reported under the purchase method.From a cash flow standpoint, investors are actually better off under the purchase method, in this example. Assuming that changes in working capital accounts will be identical under the two scenarios we shall use net income + depreciation + amortization as a proxy for cash flow. (Depreciation of net property, plant, and equipment is calculated at 20% per annum.)

EXHIBIT 10.1 Alternative Accounting Treatments for Company A’s Acquisition of Company B

Under purchase accounting, the total comes to $473,406 + lang=EN-US>$390,000 + $5,000 + $4,344 = $872,750. Cash generated under pooling of interests, on the other hand, totals just $481,000 + $390,000 = $871,000. The difference represents the tax savings on the extra depreciation expense under the purchase method: $5,000 × 35% = $1,750.

Before FASB abolished pooling of interests in 2001, companies typically structured mergers and acquisitions to qualify for pooling-of-interests treatment, even though the cash flow impact of using the purchase method was either favorable or neutral. (The latter would be the case if none of the excess of purchase price over shareholders’ equity were allocated to tangible assets). Conceivably, managers believed that they could achieve the highest share price for stockholders by maximizing net income and, as indicated in Exhibit 10.1, earnings per share. Alternatively, they may have been trying to maximize their own performance bonuses, which at least in years past, tended to be tied to reported earnings, rather than performance of the company’s stock.

The potential for abuse of pooling-of-interests accounting had been apparent for many years by the time Senator Lieberman and other politicians urged FASB to slow down its supposedly hasty effort to abolish the practice. In the layperson’s mind, the pooling-of-interests method was reserved for transactions that represented a merger of equals.

In practice, big fish routinely swallowed small fish in acquisitions that qualified as poolings under APB Accounting Opinion No. 16, “Business Combinations” (1970). As discussed later in this chapter, certain acquisitions made by Navigant Consulting qualified for pooling-of-interests accounting while also being small enough, relative to Navigant, to be deemed immaterial for financial reporting purposes.On January 24, 2001, the protracted wrangling ended in a compromise. The Financial Accounting Standards Board officially marked the pooling method for extinction. As a quid pro quo, FASB eliminated the requirement to amortize the goodwill created in mergers consummated after June 30, 2001. Neither did companies have to continue amortizing existing goodwill in fiscal years beginning after December 15, 2001.

Gone was the mandatory annual reduction of earnings, which had been the issuers’ primary objection to the purchase method all along. Cisco Systems controller Dennis Powell, for example, found the resolution highly satisfactory. “Clearly,” commented Powell, “the FASB listened and responded to extensive comments from the public and the financial community to make the purchase method of accounting more effective and realistic.” 4

To be sure, the new rules required companies to test annually for possible impairment of the goodwill on their books. Any loss of value would have to be recognized through a partial or complete write-down. Inevitably, however, there would be a sizable judgmental component to the determination that impairment had occurred.

Remarkably, Wall Street securities analysts recommended certain stocks that they contended would benefit from FASB’s decision. Reported earnings, the analysts noted, would rise as a consequence of the elimination of goodwill amortization. This argument made no sense, given that the change in financial reporting practice could not improve the companies’ economic profits one iota.

The analysts nevertheless insisted that the stocks would rise, asserting that investors were too unsophisticated to understand that goodwill was a noncash expense.One member of the analysts’ own ranks, Morgan Stanley managing director Trevor J. Harris, conspicuously rejected the notion that the change in financial reporting practices would vault shares higher. “It makes no economic sense,” said Harris, who doubled as a professor of accounting at Columbia Business School. “There should be no long-term price effect.”5

Pepperdine University Professor of Accounting Michael Davis added that there were approximately 10 academic studies of the issue, covering periods from the 1960s to the 1990s. The studies consistently found that the higher reported earnings generated by pooling did not cause the stocks of the acquiring companies to outperform the stocks of companies employing the purchase method.6 This empirical evidence did not necessarily guide the practices of analysts, however. Assistant Professor of Accounting Patrick E. Hopkins of the Kelley School of Business at Indiana University conducted an experiment in which he showed three versions of a company’s financial statements to 113 analysts employed by money management organizations. The statements differed only in that one version used pooling-of-interests accounting for mergers, whereas the other two did not. Based only on the cosmetic difference in accounting treatment, the analysts awarded higher valuations to the company’s stock when pooling was not used.7