TRUE EQUITY IS ELUSIVE

What financial analysts are actually seeking, but are unable to find in the financial statements, is equity as economists define it. In scholarly studies, the term equity generally refers not to accounting book value, but to the present value of future cash flows accruing to the firm’s owners.

Consider a firm that is deriving huge earnings from a trademark that has no accounting value because it was developed internally rather than acquired. The present value of the profits derived from the trademark would be included in the economist’s definition of equity, but not in the accountant’s, potentially creating a gap of billions of dollars between the two.The contrast between the economist’s and the accountant’s notion of equity is dramatized by the phenomenon of negative equity. In the economist’s terms, equity of less than zero is synonymous with bankruptcy. The reasoning is that when a company’s liabilities exceed the present value of all future income, it is not rational for the owners to continue paying off the liabilities. They will stop making payments currently due to lenders and trade creditors, which will in turn prompt the holders of the liabilities to try to recover their claims by forcing the company into bankruptcy. Suppose on the other hand, that the present value of a highly successful company’s future income exceeds the value of its liabilities by a substantial margin. If the company runs into a patch of bad luck, recording net losses for several years running and writing off selected operations, the book value of its assets may fall below the value of its liabilities. In accounting terms, the result is negative shareholders’ equity. The economic value of the assets, however, may still exceed the stated value of the liabilities.

Under such circumstances, the company has no reason to consider either suspending payments to creditors or filing for bankruptcy.Negative shareholders’ equity can also arise from a leveraged recapitalization, a type of transaction that gained a considerable vogue in the 1980s. The analytical relevance of leveraged recaps does not arise solely from the insight they provide into the differences between economic and accounting-based equity. One day, they may be of more than historical interest. If stock prices ever become as depressed as they were in the early 1980s, the massive stock repurchases with borrowed funds may easily make a comeback.

A leveraged recap is ostensibly designed to remedy a corporation’s low stock market valuation. Another, unadvertised purpose may be to fend off a hostile takeover. Suppose that several large shareholders, who are sympathetic (or even identical to) the corporation’s incumbent management, retain their stock as the total number of outstanding shares declines sharply. The small group of shareholders will materially increase its proportional ownership. If all goes well, the leveraged recap will kill two birds with one stone, solidifying the insiders’ control of the company while bo osting the share price to appease shareholders who were disposed to support the hostile bid.

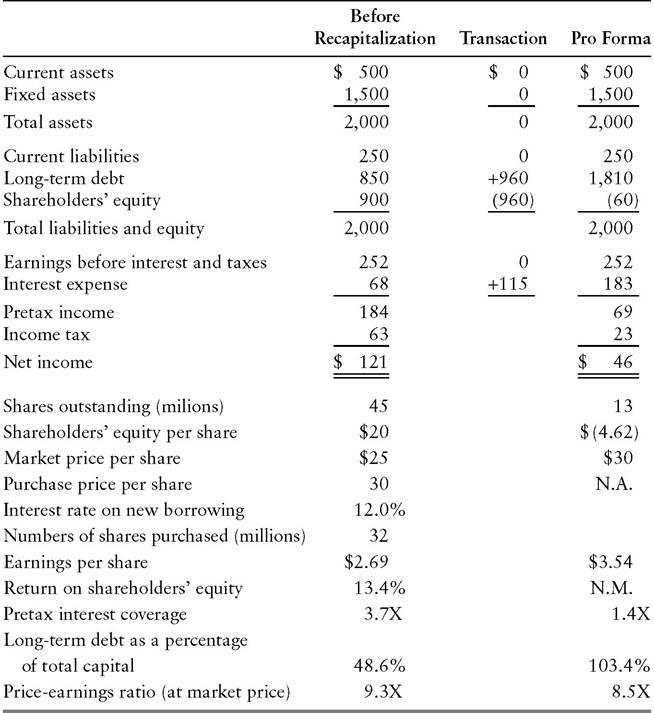

In the fictitious example shown in Exhibit 2.2, Sluggard Corporation’s stock is languishing at a modest 9.3 times earnings, or $25 a share. Restive shareholders are urging management to improve Sluggard’s operating performance, explore the possibility of selling the company at a premium to its present stock price, or step aside in favor of others who can do a better job of enhancing shareholder value. A dissident group has even nominated its own slate of directors, who are committed to divesting unprofitable operations and replacing the current chief executive officer.

Management counters by asserting that the real problem is with the stock market.

Fickle, short-term-oriented investors are not attributing appropriate value to Sluggard’s excellent long-term business prospects. Under current market conditions, says the CEO, shareholders cannot realize full value on their investment by engineering the sale of Sluggard to a bigger company.To satisfy shareholders’ legitimate desire for better stock performance, while preserving Sluggard’s ability to capitalize on its outstanding opportunities as an independent company, management and the board announce a bold financial transaction. The company will tender for 32 million of its 45 million outstanding shares at a 25% premium to the current market price, or $30 a share. To pay for the $960 million stock repurchase, Sluggard has arranged an interim credit line, which it plans to refinance through a longterm bond offering. The greatly increased debt load that will result will raise interest expense from $68 million to $183 million annually, on a pro forma basis. After-tax income will consequently drop from $121 million to $46 million. That decline will be more than offset, however, by the reduction in shares outstanding. Earnings per share, management concludes, will rise from $2.69 to $3.54.

To be sure, the market may lower Sluggard’s price-earnings ratio to reflect the increase in financial risk indicated by a sharply higher ratio of long-term debt to capital and a significantly reduced pretax interest coverage ratio (see Chapter 13). Under reasonable assumptions, however, the company’s stock should continue to trade at the tender price of $30 a share

EXHIBIT 2.2 Leveraged Recapitalization (Illustration)

Sluggard Corpooration Condensed Balance Sheet and Income Statement December 31, 20XX ($000 omitted)

after the tender offer is completed.

Accordingly, the currently disgruntled stockholders will get a chance to sell some of their shares at a big premium to the current market and also enjoy a longer-run boost to the share price. Furthermore, for the next few years, Sluggard plans to devote the cash generated from its operations to debt repayment. That should take care of the biggest concern raised by management’s plan, namely, the heightened risk of financial strain posed by sharply increased interest costs.Based on the bankruptcies of many prominent companies that underwent leveraged buyouts or leveraged recapitalizations in the 1980s, investors’ worries about Sluggard’s expanded debt load are by no means unfounded. In the period of the leveraged recaps’ greatest popularity, in fact, many veteran financial analysts perceived the leveraged recaps to be bankrupt from inception. The only instances in which they had previously observed negative shareholders’ equity, comparable to the -$60 million figure shown in Exhibit 2.2, involved moribund companies that had wiped out their retained earnings through repeated losses. Typically, those companies were approaching negative equity in the economic, as well as the accounting sense.

The leveraged recaps presented a very different case, however. Their negative shareholders’ equity figures arose from the conventions of doubleentry-bookkeeping. Unlike other kinds of asset purchases, a company’s purchase of its own stock does not simply result in one type of asset (cash) being replaced by another (such as inventory or plant and equipment) on the balance sheet. Instead, the entry that offsets the reduction in cash is a reduction in shareholders’ equity. In the illustration, Sluggard pays a premium over book value, with the consequence that a buyback of less than 100% of the shares costs more than the stated shareholders’ equity.

Despite the resulting negative shareholders’ equity that arises, Sluggard is by no means faced with an immediate prosp ect of bankruptcy. The company’s pretax earnings continue to cover expense, albeit by a slimmer margin than formerly. Moreover, Sluggard is continuing to earn a profit, which the stock market is capitalizing at $30 a share times 13 million shares, or $390 million. This is a plain demonstration that in economists’ terms, the company continues to have a substantially positive equity, whatever the financial statements show.