LOSING VALUE THE OLD-FASHIONED WAY

Goodwill write-offs by technology companies such as Uniphase make splashy headlines in the financial news, but they by no means represent the only way in which balance sheet assets suddenly and sharply decline in value.

In the “Old Economy,” where countless manufacturers earn slender margins on low-tech industrial goods, companies are vulnerable to long-run erosion in profitability. Common pitfalls include fierce price competition and a failure, because of near-term pressures to conserve cash, to invest adequately in modernization of plants and equipment. As the rate of return on their fixed assets declines, producers of basic commodities such as paper, chemicals, and steel must eventually face up to the permanent impairment of their reported asset values.In the case of a chronically low rate-of-return company, it is not feasible to predict precisely the magnitude of a future reduction in accounting values. Indeed, there is no guarantee that a company will fully come to grips with its overstated net worth, especially on the first round. To estimate the expected order of magnitude of future write-offs, however, an analyst can adjust the shareholders’ value shown on the balance sheet to the rate of return typically being earned by comparable corporations.

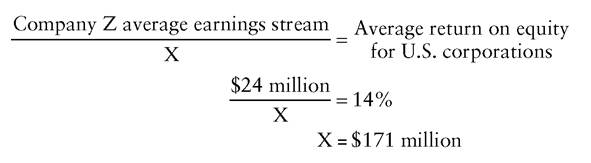

To illustrate, suppose Company Z’s average net income over the past five years has been $24 million. With most of the company’s modest earnings being paid out in dividends, shareholders’ equity has been stagnant at around $300 million. Assume further that during the same period, the average return of companies in the Standard & Poor’s 400 index of industrial corporations has been 14%.

Does the figure $300 million accurately represent Company Z’s equity value? If so, the implication is that investors are willing to own the company’s shares and accept a return of only 8% ($24 million divided by $300 million), even though a 14% return is available on other stocks. There is no obvious reason why investors would voluntarily make such a sacrifice, however.

Therefore, Company Z’s book value is almost certainly overstated.A reasonable estimate of the low-profit company’s true equity value would be the amount that produces a return on equity equivalent to the going rate:

Although useful as a general guideline, this method of adjusting the shareholders’ equity of underperforming companies neglects important subtleties. For one thing, Company Z may be considered riskier than the average company. In that case, shareholders would demand a return higher than 14% to hold its shares. Furthermore, cash flow (see Chapter 4) may be a better indicator of the company’s economic performance than net income. This would imply that the adjustment ought to be made to the ratio of cash flow to market capitalization, rather than return on equity. Furthermore, investors’ rate-of-return requirements reflect expected future earnings, rather than past results. Depending on the outlook for its business, it might be reasonable to assume that Company Z will either realize higher profits in the next five years than in the past five or see its profits plunge further. By the same token, securities analysts may expect the peer group of stocks that represent alternative investments to produce a return higher or lower than 14% in coming years. The further the analyst travels in search of true value, it seems, the murkier the notion becomes.