2000-2014: ERA OF PARTICIPATION AND MULTIMEDIA (WEB 2.0)

By 2002 the World Association of Newspapers had recognized that ‘the Internet is proving to be neither the threat nor the opportunity that we all once expected’ (WAN- IFRA, 2002).

The bursting of the dot-com bubble in 2000 removed any hope of recovering investments in online businesses via IPOs or spinoffs. As Internet sites became more sophisticated, publishers realized that print content could not simply be transferred online. It needed to be presented differently and the content itself needed to be adapted for online consumption styles - more depth was often required, and immediacy was critical. The realization also dawned that digital editions needed primacy over print ones. Newsrooms were not simply going to need a stronger digital component, but ultimately would have to become digital news operations with a print component. Breaking news needed to appear online first.And just as content did not transfer happily online, neither did their traditional advertising pricing models. In print newspapers, the amount of space for advertising is limited. This scarcity increases its economic value and price. In the digital world the amount of advertising space is nearly unlimited and supply outstrips demand. As a result, online advertising prices are lower than in print and falling constantly - ‘print dollars have been replaced by digital dimes’, as the adage goes.

So although the volume of online advertising increased during this period, and indeed grew faster than all other forms of advertising, overall revenue levels remained low. Moreover, not only were prices lower online, but there were more competitors. Even by 2014, print media still account for about two-thirds of all advertising expenditures worldwide.3 Despite the migration of classified advertising to the Internet - and an overall decline in advertising expenditures - print newspapers are still producing profits.

One of the most disruptive elements of the Internet has been the way it has enabled the unbundling of the various component parts of traditional newspapers. Search engines and aggregators allow Internet users to find a range of articles on any subject without having to visit publishers’ online sites. A large percentage of classified advertising has moved online. And contextual search advertising has reduced the appeal of publishers’ display markets.

Even so, publishers were reluctant to switch to digital-only distribution, even though this would allow news to be produced and distributed far more cheaply - three-quarters of their costs derive from printing, distribution, property and facilities management (Picard and Brody, 1997). This dilemma has led an increasing number of publishers to look again at pay models. Strategies vary, according to local market conditions, the size and role of the news provider, and the competing services. A more subtle factor affecting the strategy is the fundamental trade-off publishers must make between maximizing the income paid by subscribers versus maximizing the greater advertising revenue that will result from a larger number of unique visitors: generally the higher the subscription fee, the lower the overall visitor number and by extension the lower the advertising revenue.

Publishers must also make a basic choice between a pay-per-use or subscription-based models. Pay-per-use provides access to a single article or a single issue, or one-day access to all content. Payment can be by currency transfers, credit cards, or e-money held in an account with the media company. These systems involve high numbers of micropayments and carry high transaction costs for managing transactions, accounting and auditing, and conveying payments. To be viable they must be highly efficient and used by a large number of people. News providers are starting to establish joint systems, as with the Project Piano payment system that provides paid access to parts of publishers’ sites in Slovakia, Slovenia and Poland, or the industry-wide user management and payment system introduced in 2013 by 11 Belgian newspapers.

Subscription models allow access over a fixed period of time (say one, three or 12 months). Some provide access to all content, and some to basic content with additional charges for premium content. Payments for subscriptions can typically be made both online and offline.

All these models involve a ‘paywall’ that prevents users from accessing the content without payment. Paywall strategies differ. They can be ‘hard’ and block access to all or most content without payment, or ‘soft’ or ‘metered’, where there is limited free access, after which users must pay. The Financial Times, for example, instituted such a model in 2007 when it set up a system allowing users to view five articles per month for free, required registration to obtain 6-30 free articles per month, and required users to pay for a subscription after viewing more than 30 articles. The New York Times also introduced a metered model in 2011 and has a complex range of payment options including print + digital access, all digital access from any device, or access restricted to various combinations of computers, smartphones and tablets.

Another option pursued by some websites is the ‘freemium’ approach in which some basic content is free (usually breaking news, blogs and some other current content) but payment is required to access more in-depth or premium content. A further revenue source for newspapers and news magazine is charging for app-based delivery of news to tablets and smartphones, while online content consumed on a computer remains free. Newspapers are typically sold by subscription or short-term trial subscriptions, but many weekly news magazines, such as the Canadian news and public affairs magazine Macleans, offer single-issue app-based purchases as well as subscriptions.

By 2013, payment for digital content and online advertising was providing 15-25 percent of the total income for many large news providers, but the progress has been modest.4 In order to make online news provision viable they, along with smaller news organizations and many digital-only start-ups, are exploring a ‘long tail’ of new revenue sources.

These include e-commerce, the digital agency concept (where they act as online marketers and provide training and consulting), ‘people media’ (public events such as conferences and festivals), training courses, and grants and subsidies.Broadcasters’ news portals or sites became more sophisticated, complex and interactive during the second web era. There was increased use of user-generated still picture and video content, blogs, personalization features, and RSS feeds,5 and social media such as Facebook, YouTube and Twitter were added to their existing services.

In addition, the distribution of broadcast programming over broadband networks became standard, via streaming, on-demand services or via smartphone and tablet apps. This rapidly became an accepted dimension of television distribution and consumption, but unlike the stand-alone news websites that were a new activity for broadcasters, the online (re)distribution of news broadcasts involved minimal changes to the content. Rather, it was a new means of distributing traditional types of content, including news content.

Second- and third-screen consumption also became standard during this period. Here, audiences can be consuming broadcast news on one screen, looking at an Internet site in parallel on another, and using social media to communicate about that content on a third. In this context social media are functioning as a means of promoting content, drawing audiences back to the broadcast content, and increasing audience engagement.

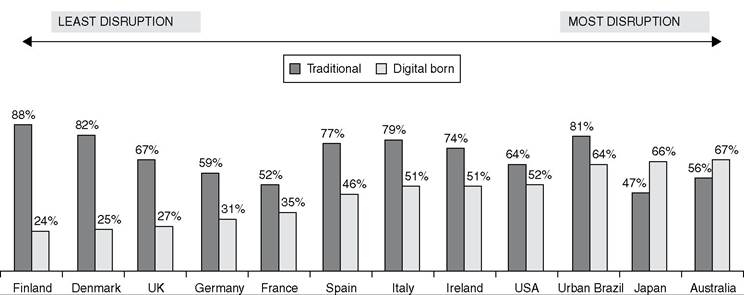

During the second Internet era, the greatest disruption for legacy news providers came from new Internet-based news organizations (the pure plays) and aggregators. They were successful in attracting significant audiences (although this differs around the world, as shown in Figure 21.1), and created new market demand by engaging new audiences. They also contributed to the commoditization of breaking news, a key element of newspapers’ product packages.

The arrival of powerful self-publishing software led to the phenomenon known as the ‘blogosphere’, and a dimension of this comprised blogs dealing with news and politics. The concepts of the blog, the Web 2.0 movement, and social media were all driven in part by the idea that every citizen can create news, and brought a new wave of disruption to the field.

Blogs written by individuals widened the range of news perspectives available but had limited appeal to advertisers. It has been estimated that 60 percent of bloggers do so for fun, that only 18 percent aim to make a full- or part-time living from it, and that the average earnings for bloggers who run ads is around $5000 per year with the top 10 percent

Source: Reuters Institute (2015).

Figure 21.1 Strength of traditional news brands by country

of bloggers earning an average of $19 000.6 The rise of social media sites like Twitter and Facebook has further undermined the prospects of blogging, and many ‘A-list’ bloggers have quit, cut down their commitments, or returned to mainstream media.

Cheap blogging technology has, however, proved to be the inspiration for a small number of successful new online news businesses. Entrepreneur Nick Denton established Gawker Media in 2002 in New York City, which after a troubled start emerged with eight blogs focusing on specific content niches (e.g., Gizmodo, which deals with technology). These new players did not have the financial cushion of still-profitable (just) print businesses to subsidize growth until they had revenue streams in place. Those that have succeeded combined low-cost models with previously unserved niche audiences (the so-called boutique aggregators), or are able to access large audiences with an innovative news offer. Two such examples are Mashable and TNZ. Mashable.com, which was founded in 2005 by 19-year-old Pete Cashmore in his bedroom in Scotland, developed into a social media and technology blog that was at one stage valued at $200 million.

TNZ is a celebrity news website founded in 2005 as a collaboration between AOL and a division of Warner Bros, that is focused on breaking celebrity stories such as the death of Michael Jackson.Crowdsourced journalism has been another important aspect of this second phase. The Korean website OhMyNews.com, launched in 2002, attracted international attention as the first news site in the world to be written by its (paid) contributors. It had a major impact on the South Korean media scene by opening up a new type of news stories, but struggled with the costs of managing and editing the contributions. Its international version closed in 2010 and today relies on some big advertisers and public appeals for cash for its domestic edition.

Another significant new content player was Wikipedia, founded in 2001, a free encyclopedia written almost entirely by volunteers. The basic idea is that collaborators initiate entries on subjects they find interesting, and other collaborators add to these entries - in the process cleaning up errors or misleading elements. While it is still primarily a reference work, Wikipedia has somewhat surprisingly also developed into important reference point for information about news.

During this second Internet era some new players have matured into significant and powerful forces in the news establishment. The Huffington Post, a US website, content aggregator and blog founded by Arianna Huffington in 2005, has become the most heavily trafficked political news site in the United States. It aggregates content from various news sources, including blogs, has its own columnists, and has won a Pulitzer Prize. Bought by AOL for $315 million in 2011, it has since developed into more of a general news site, hired more journalists, and has branched out into video. It now has editions in Canada, France, the UK, Italy, Spain and Germany.

A further wave of change in online news followed the launch of social media sites like Facebook (2004) and Twitter (2006). These networks do not create content themselves, but act as fora where links to both user-generated content and professional journalism can be quickly and efficiently shared. In this sense they have become an important source of news as well as a powerful new distribution mechanism, helping drive traffic to traditional news sites. By 2012 it was estimated that one in five people (20 percent) in the UK find news stories each week via news streams on social networks and social news aggregators (Reuters Institute, 2012).

From a business perspective, however, social networks have made it even harder for news sites to make money, by providing extra competition for the limited amount of online advertising expenditure. And like Google, they bring additional disruption because they have created new types of advertising by drawing on the extremely rich data they have collected from, and about, their users. Online news players, particularly legacy players, do not have access to comparable aggregated data, potentially further undermining their competitive position in the delicate advertising ecosystem.

Smartphones, tablets and other mobile media devices are also disrupting online news provision. Many news providers have created apps for mobile devices that function as ‘destination news brands’ that can be accessed directly from the home screen. Although it is early days, it appears that strong news brands tend to do better in a mobile environment than on a PC where the browser acts as the gateway to the Internet and where portals and ISPs have traditionally acted as homepages for large numbers of users.7

New mobile gateways are also emerging for online news. Apple’s Newsstand is an app that simulates a real newsstand with virtual shelves offering digital versions of newspapers and magazines. Amazon’s version is a folder that allows access to publications users have subscribed to. But while apps represent a welcome new income source, publishers are unhappy about the terms offered by Apple, Google, and Amazon. In 2011 the Financial Times removed its iPad and iPhone apps from Apple’s App Store after losing a battle to keep the consumer data generated through purchase process, and because it was unhappy with Apple’s policy of taking a 30 percent share of revenues.

This second online era is marked by the appearance of start-up news and information providers using emerging software and applications, and by increased use of visual and audiovisual content. It also produced significant changes in publishers’ views of how news should be provided online, growing understanding of differences among digital platforms, and a search for new revenue models. Online news provision became more competitive because of the significant inroads made by broadcast news organizations and new ‘born digital’ news providers.

21.4