A BRIEF HISTORY AND OVERVIEW OF THE ONLINE ADVERTISING SECTOR

20.2.1 Key Technological and Institutional Developments

ARPANET and NSFNet, the government-funded predecessors to today’s Internet, had acceptable use policies that banned their use for advertising.

Nevertheless, what may have been the first use of the Internet for advertising occurred in 1978 when American West Coast ARPANET users received emailed ads for personal computers (Seabrook, 2008).426

Display advertising began in the 1980s when the subscription-based online service provider, Prodigy, which was jointly owned by IBM and Sears, displayed banner-like ads for Sears. The date for the first clickable online ad is a matter of dispute. Tim O’Reilly, the founder of Global Network Navigator (GNN), claimed that the first clickable ad appeared on his website in 1993 (Bourn, 2013), but Kaye and Medoff (2001) date the first clickable ad to 1994 when Hotwire sold its first banner advertisement. By today’s standards, when the average click-through rate is reported to be about 0.1 percent (Interactive Advertising Bureau, 2012), these early clickable ads were very effective. According to Morrissey (2013), AT&T’s first clickable ad had a 44 percent click-through rate.

As is detailed by Hal Varian in Chapter 18 in this volume, search advertising services tried out a variety of mechanisms for ordering search results before Google’s introduction of the page ranking mechanism for ordering organic listings established a standard that, while it has evolved, still rules today. The first search advertising auction was created by GoTo.com in 1998, which changed its name to Overture in 2001 and was acquired by Yahoo! in 2003. Google launched its AdWords' search advertising program in 2000. In 2002, Google introduced the generalized second-price (GSP) auction, which, with modifications, is the pricing mechanism used for most search ad sales today.

Display ads and the ways they are sold have also changed considerably as the online ad industry has grown and evolved. The massive online data storage and computational capabilities that made possible the profusion of interactive Web 2.0 services since 2000 have also been employed to create the targeting capabilities that are now routinely used to match an advertiser’s online ads to Internet users with web-generated profiles that mark them as more likely to be receptive to the advertiser’s messages. While untargeted display ads have not disappeared, targeted ads have accounted for much of the growth of this segment.

In the 1990s, almost all display advertising inventory was sold through salespeople, but by the end of the 2008-09 recession real-time bidding for audiences defined by preset descriptive parameters had emerged as an important alternative for selling and buying online inventory. The use of pre-set parameters made it possible to computerize and automate the purchase process so that ads targeted to users that matched the specified parameters could be loaded automatically when users matching those parameters loaded websites to which an advertiser had purchased access. The process by which such ads are purchased is known as pre-set bidding and is commonly managed by ad networks, which are described below. Automation of the process has also made it possible to bid on ads in real time, with the option to purchase remaining inventory available up to the time an ad is placed before a user with the requested pre-set parameters (Reynolds, 2011).

20.2.2 Growth and Proliferation of Online Advertising Services

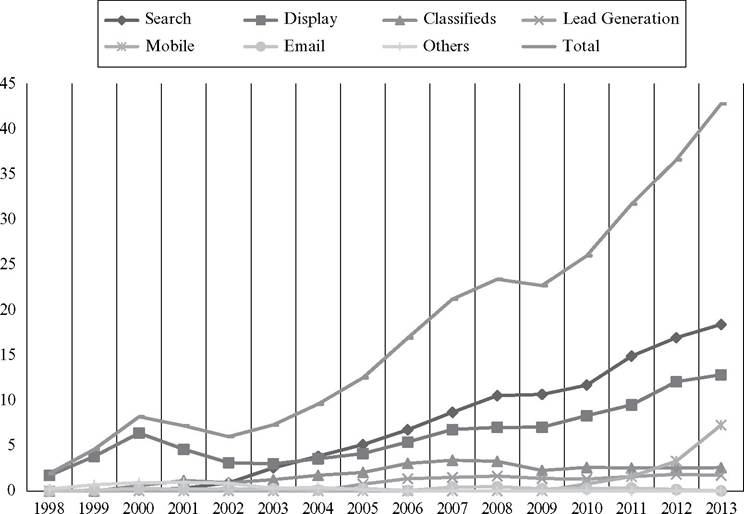

According to the Interactive Advertising Bureau (IAB) (2007), total online advertising was a fairly modest $55 million in 1995, the first year the Internet was commercialized. While in percentage terms, growth in its early years was quite rapid, through the 1990s this was accounted for largely by growth in display ads, which in 2000 accounted for over three-quarters of online ad sales of $8.2 billion.

This was also the first year that search advertising shows up (at $0.1 billion) in IAB’s time series. By 2004 the search share of total online ad sales had passed that of display. In 2013, search accountedTable 20.1 USA online advertising spending by formats in 2013 ($ billions)

| Ad Format:3 | Search | Display | Classifieds | Lead Generation | Mobile | Total | |

| 18.4 | 12.8 | 2.6 | 1.8 | 7.1 | bgcolor=white>NA42.8 |

Note: Four of the format labels for this table are self-explanatory, but two are not. Lead generation refers to the use of any of several online vehicles, including email, display ads and online forums, to place before consumers news of product deals they can learn more about by contacting a vendor directly using an identifier provided. The vendor then compensates the lead generator when contacted by ‘leads’ that provide the corresponding identifier. Email ads are messages customized for delivery through mobile devices, such as smartphones, feature phones and tablets. Mobile ads can include static or rich media display ads, text messages, search ads and audio or video ads in mobile apps.

Source: Interactive Advertising Bureau (2013).

Sources: Interactive Advertising Bureau (1999-2014).

Figure 20.1 US online advertising spending by formats, 1998-2013 ($ billions) for $18.4 billion, 43 percent of all online ad sales, which is about double the share for display. Other categories of online advertising have emerged since 1999 to account for noticeable, though much smaller shares of online ad sales, with mobile ads the most recent category to emerge. The IAB's 2013 revenue totals for the six major categories of online advertising are presented in Table 20.1.

Figure 20.1 shows the levels and trends for the six major categories plus the minor categories that are combined under ‘others’ from 1998 on.1 Table 20.1 and Figure 20.1 both illustrate the diversity of services that contribute to the online advertising total, and even these figures mask diversity within the six categories, such as the distinction between the targeted ads and run-of-site ads that contribute to the display total. Run-of-site advertisements are displayed to anyone who visits a webpage where they are placed. Advertisers who want to reach broader audiences, such as those selling fast-moving consumer goods (FMCG), often choose this type of advertisement. A targeted ad appears only in front of visitors identified as matching the profiles of individuals deemed most likely to respond to the ad’s appeal.20.2.3 Supporting Services

Advertising in online media is supported by a large collection of intermediaries, facilitators and suppliers of various complementary services that collectively, and sometimes individually, are substantial businesses in their own right. While some have close counterparts in offline advertising, many do not. Major categories of support services for the online advertising industry include advertising networks, advertising exchanges, demandside platforms (DSPs), search management platforms (SMPs), audience measurement services, and advertising agencies.

The fact that the Internet audience is dispersed across millions of webpages and services (such as RSS [really simple syndication] feeds and email advertising services) makes it highly desirable, if not necessary, to aggregate audiences across multiple outlets to achieve meaningful scale. Advertising networks perform this aggregation service in exchange for a portion of the fees advertisers pay for placements with online publishers and other online services that affiliate with them. They also provide the targeting services, described in more detail below, that allow an advertiser to place its ads before specified subsets of the web users accessing a network’s affiliates who, by various metrics, are judged to be particularly attractive recipients of the advertiser’s message.

In some cases fees paid by advertisers are set by the affiliated outlets, while in other cases networks set these prices and remit a predetermined fraction of revenues generated to the participating sites and services.In the USA the market for ad networking services is highly fragmented and has no clearly dominant providers. For example, for June 2012 comScore listed the Google Ad Network as the largest in the USA with nearly 206 million unique visitors while crediting Undertone, the twentieth ranked network, with close to 124 million unique visitors, approximately 60 percent of Google’s total (comScore Media Metrix, 2012).

Not all online advertising inventory is sold through networks. Some web services sell some or all of their ad inventory directly and some is sold through advertising exchanges, which, like ad networks, help reduce the transaction costs associated with connecting online inventory suppliers to buyers of ad availabilities. Exchanges are totally automated with prices set through online auctions. Exchanges also help advertisers evaluate suppliers of online inventory by providing data on the audiences they attract.

Demand-side platforms (DSPs) help advertisers and agencies perform many of the tasks associated with managing the display component of an online advertising campaign. Search management platforms (SMPs) provide analogous services for the search components of such ad campaigns. Services include budget allocation and management and development and implementation of bidding strategies.

Audience measurement services play the same roles for online advertising that they have played for offline media for many decades, providing third-party estimates of the sizes and characteristics of the audiences attracted by media vehicles. Unlike offline media, where one or occasionally a couple of audience measurement services typically dominate the supply of audience measurements for a given medium,2 currently measurement of Internet audiences is a more competitive affair.

comScore, which is indigenous to the Internet, and Nielsen, the primary supplier of television audience measurements in the USA, are the largest players, but face competition from ad networks and DSPs and from some publishers, like Google, Facebook and Yahoo!, all of whom provide information on their audiences that includes much more than mere counts.Whether in the long run online advertising markets will also settle on a very small number of audience measurement services whose measures are accepted universally by both publishers and advertisers remains to be seen. Auditing print circulation is a time- and people-intensive operation and the small but supposedly statistically representative panels of television viewers and radio listeners that have traditionally been the foundation for measuring television and radio audiences are also expensive to administer. Economies of scale and near homogeneous services may have dictated monopoly or duopoly structures for the markets for these services. On the other hand, the basic count data used to estimate the sizes of Internet audiences is both comprehensive and relatively easy and inexpensive to produce and the costs of the analytics services offered by ad networks and exchanges has yet to produce significant concentration in the provision of these services.

20.3