INEQUALITY IN INCOME

8.4.1 Measures of Inequality from the Overall Distribution

8.4.1.1 Introduction

This section focuses on measures of the overall distribution of income in high-income and some middle-income and developing countries.

In contrast with the next section, which focuses narrowly on the top of the pretax income distribution, this section considers a variety of statistics that either explicitly exclude the very top (and bottom) of the distribution or that use the full distribution but are calculated with data that are not necessarily representative of incomes at the very top. Most of this section describes trends since 1970, but some attention is also paid to data series that are available over shorter periods and to a single-year analysis of the most current available income data, which allow us to discuss a broader range of inequality metrics and a greater number of countries.Overall conclusions about the broad distribution of household income include:

* The countries with the least unequal distributions are the Nordic (Sweden, Norway, Denmark, and Finland) and “Benelux” (Belgium, Netherlands, and Luxembourg) countries as well as Austria and some eastern European nations.

* Across MICs and high-income countries there is a wide range in levels of inequality. By most measures the income distribution in the United States is among the most unequal, and when compared with the narrower set of the richest nations, the distribution in the United States is the most unequal. A number of MICs and developing nations, including Brazil, China, Turkey, and South Africa, though, have income distributions that are more unequal than in the United States.

* Taxes and transfers reduce the degree of inequality in every country, but there is dramatic variation in the extent of redistribution. The impact of taxes and transfers is very small in some highly unequal countries (Russia) and some less unequal ones (South Korea).

In some countries, taxes and transfers have a dramatic impact on the distribution of income; Finland has among the most unequal distributions of market income but one of the most equal distributions of DHI because of the extensive distribution in its welfare state. The United States combines relatively high levels of inequality in market income with very low levels of tax and transfer redistribution to achieve the highest level of DHI inequality among rich nations.* The distribution of income has become more unequal in most countries since the 1970s. The only rich country to buck the long-term trends toward greater inequality is France. Even France, though, has experienced increases in inequality since the early 2000s.

* The income distribution in a number of countries has followed a U-shaped pattern (Sweden, Finland, and Canada), falling in the 1970s or the 1980s before rising in the 1990s.

* Two of the most unequal of the rich nations—the United States and the United Kingdom—experienced large increases in inequality in the late 1970s and 1980s and modest increases in the second half of the 1990s, but in both countries the level of inequality in 2010 was not very different from levels experienced in the early 1990s.

* The distribution of market income in Germany, Italy, Japan, and some of the Nordic countries grew steadily more unequal between the mid-1980s and the mid-2000s, and the distribution of pretax/transfer income in those countries is now almost as unequal as in the United States, Israel, or the United Kingdom.

* In almost all countries the long-term trends in inequality are more pronounced among the working-age population.

8.4.1.2 Distributional Statistics

A variety of statistics have been developed for the analysis of the distribution of income. The most commonly used statistic is the Gini coefficient, but a number of other measures have been applied to a wide range of countries using data covering the most recent decades. The statistics discussed below include Lorenz curves, the Gini coefficient, Atkinson Index (ATK), percentile ratios (P90/P50 and P90/P10), quintile shares (S80/S20), and the Palma Index.

(See Allison, 1978; Atkinson, 1970; Cowell, 2000; Heshmati, 2004; among others, for overviews of the various summary statistics to describe distributional inequality.)Not a statistic perse, the Lorenz curve is a graphical representation of the cumulative distribution of income. The Lorenz curve uses ordered income data and shows the cumulative share of income held at each point in the distribution of households.

To reduce the information contained in the Lorenz curve to a single number, a variety of summary statistics have been proposed. One that has a direct link to the Lorenz curve is the Gini coefficient. The Gini coefficient can be calculated in a number of ways and visually can be represented as a ratio of the area between the Lorenz curve and the perfect equality line divided by the total area below the perfect equality line. In ordered data for household share of total income, the 45-degree line represents perfect equality; each household has the same income and each point in the distribution of total households matches the same point in the distribution of total household income (e.g., the bottom 45% of households receive 45% of total income). The Gini coefficient ranges from 0 (perfect equality) to 1 (the most extreme inequality) if all income is held by a single household.

Using unordered data, the Gini coefficient for household income can be calculated as the relative mean difference, or the average absolute difference between incomes for all pairs of households divided by twice the mean income (Allison, 1978):

where N represents the total number of households, i and j index each household in all possible pairings of household, x is household income, and x is mean income over the sample.

The Gini coefficient is one of many statistics representing the entire distribution. Other commonly used measures of inequality focus on specific points or regions of the distribution.

Below we discuss inequality measures from the most recently available data using the P90/P10 and P90/P50 interdecile ratios, which represent “high” income levels (from the 90th percentile of the distribution in this case) as some multiple of “low” income (the 10th percentile of the distribution) or “middle” income (the median). Asimilarmeasure, the S80/S20, represents a ratio of the shares of total household income received by those in the top quintile of the distribution and those in the bottom quintile. The Palma Index, popularized by Palma (2011), is a slight modification of the more common S80/S20 and divides the share of income held by the highest 10% of the distribution by the share of income received by the lowest-income 40% of the distribution.The final measure discussed in this section is the ATK.20 Similar to the Gini coefficient, the ATK summarizes the entire distribution. Unlike the Gini, though, the ATK can be decomposed to identify different groups or income sources making different contributions to inequality. The ATK differs from the previous measures by explicitly incorporating a weighting variable that can be selected to place more weight on incomes at the top or the bottom of the distribution

[1] The mean log deviation (MLD) is another statistic that uses the entire distribution but tends to produce results very similar to the Gini coefficient. MLD statistics are not included here because of limited space, but they have been calculated by the OECD in the past, including in Divided We Stand (2011). Also, the squared coefficient of variation (SCV) has been used in some analyses of income distribution, including OECD (2011), but rankings developed using this measure are very sensitive. Deding and Dall Schmidt (2002) showed that, compared to the Gini coefficient, the SCV produces substantially larger year-to-year shifts in inequality and is particularly sensitive to tax and transfer payments at the upper tail of the distribution.

For these reasons we do not include SCV measures in this review.aversion, reflect greater sensitivity to incomes at the lower end of the distribution. The ATK falls between 0 and 1, equaling 0 under perfect equality and with higher values when dispersion is greater.

8.4.1.3 Levels of Inequality in High- and Middle-Income Countries in the Late 2000s With expanded interest in the distribution of income, there are more data available from recent years to compare incomes across countries than at any point in history. This section reviews evidence from a broad array of rich countries and MICs using all of the distribution statistics described above. The following section focuses on a narrower set of countries and examines trends in the distribution of income using a more limited set of statistics. All of the analyses in these sections rely heavily on the data produced and made available by LIS, Eurostat, the OECD, and the national statistical agencies of a handful of rich countries.

8.4.1.3.1 LorenzCurves

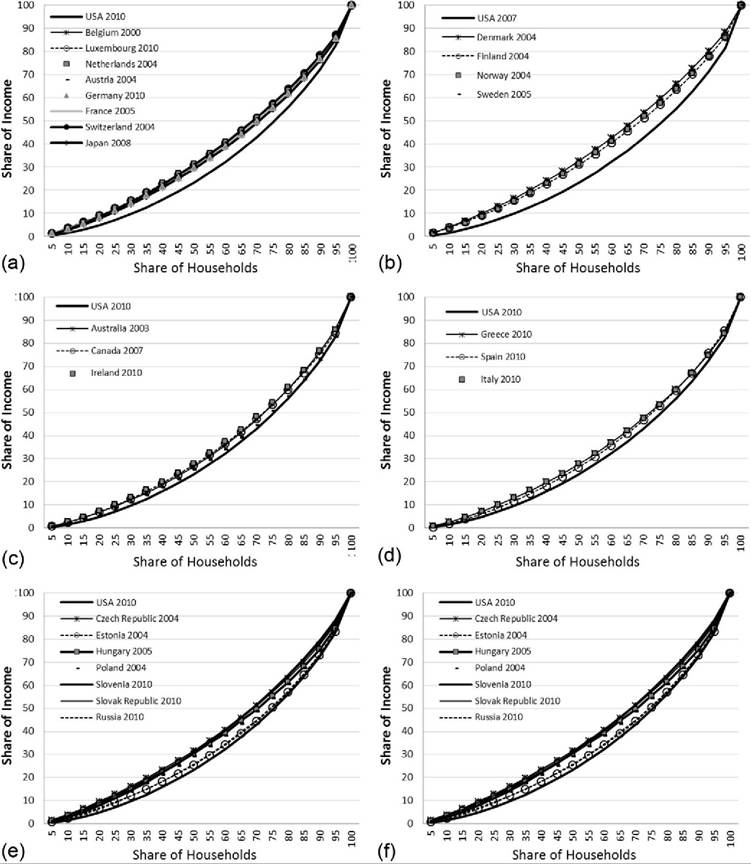

Unlike most summary statistics used in the analysis of inequality, Lorenz curves visually represent the entire distribution. Analyzing these plotted cumulative distribution functions allows us to see whether pairs of countries can be ranked by standard dominance criteria.[378] Figure 8.8 includes a series of Lorenz curves for different geographically or institutionally coherent clusters of countries. Each graph also includes the Lorenz curve for the United States to aid in comparability across the different graphs. The figure uses data from the most recent LIS wave for each country (identified in the individual graphs) and represents equivalized DHI.[379]

The distribution of income in the continental European countries (including Austria, Belgium, France, Germany, Luxembourg, and Switzerland), as well as Japan (shown in Figure 8.8a), and the Nordic countries (Denmark, Finland, Norway, and Sweden, shown in Figure 8.8b) is much less unequal than in the United States.

Because the Lorenz curves do not cross at any point, we can say that each of these countries has a “superior” Lorenz curve to the United States. Any differences between these countries—which are slightly more evident among the Nordic counties—are small compared with their differences with the United States.The U.S. distribution is more unequal than most of the rest of the European countries, but not to such a great extent. In the case of the Anglo-Saxon countries (Figure 8.8c), Australia, Canada, and Ireland have Lorenz curves that are superior to that of the United States, but the Lorenz curves for the United States and the

Figure 8.8 Lorenz curves Ofequivalized DHI (LIS) in the mid- and late 2000s: (a) continental European countries (and Japan), (b) Nordic countries, (c) Anglo-Saxon countries, (d) Southern European countries, (e) Eastern European countries, and (f) other countries. Data are based on the authors'analysis of LIS data.

United Kingdom are virtually indistinguishable, although they do not cross. The United States also has an inferior Lorenz curve relative to the countries in Southern Europe (Spain, Italy, and Greece, shown in Figure 8.8d), but the gaps are less dramatic than for the Nordic or continental European countries. None of the southern European countries has a distribution that is superior to the others, as the Lorenz curves cross at the top and the bottom of the distributions.

Even in Eastern Europe (Figure 8.8e), each country has a Lorenz curve superior to that of the United States. In the case of Estonia (2004) and the Russian Federation, the distribution is very similar, especially in the upper third, but at no point do the Lorenz curves cross. In the Slovak Republic, Slovenia, and the Czech Republic (2004) the distributions look more similar to those of continental European countries than those of their Eastern European neighbors.

Only when we expand the set of countries beyond Europe and include MICs and developing counties do we find distributions of income that are more unequal than that of the United States (“Other Countries” include South Korea, India, China, Brazil, and Israel, shown in Figure 8.8f). The most recent LIS data for Brazil, India, China, and South Africa show that the Lorenz curves for those countries are inferior to that of the United States. Among those four nations, South Africa stands out with the most unequal distribution. Israel and the United States have virtually indistinguishable Lorenz curves, both of which are inferior to the Lorenz curves for South Korea and Taiwan.

8.4.1.3.2 EU and OECD Country Summary Statistics and Rankings

In recent years the EU and the OECD have calculated timely summary distributional statistics for their member countries. These figures are based on DHI data from 2010 to 2011 for the EU and “around 2010” for the non-EU OECD countries.[380] Statistics from both entities are adjusted for household size using slightly different equivalence scales.

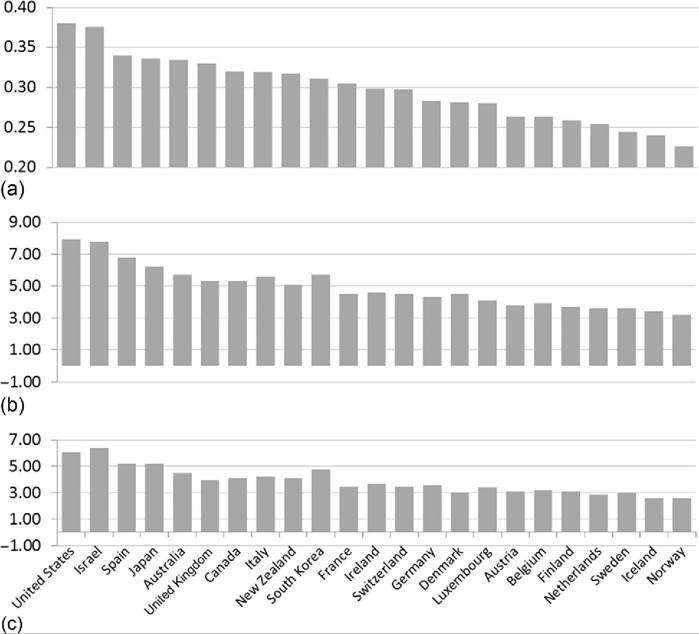

Figure 8.9 includes three different summary statistics for the 23 richest nations that are EU or OECD members and is sorted based on rankings for the Gini coefficient (shown in Figure 8.9a).[381] With a Gini coefficient of 0.38, the United States has the highest level of inequality among the rich nations. At the other extreme, with Gini coefficients between 0.23 and 0.28, the Nordic and Benelux (Belgium, Netherlands, and Luxembourg) countries and Austria had the most equal distribution of income, led by Norway. The large continental economies and the Anglo-Saxon countries fall in the middle, with Gini coefficients ranging from 0.28 and 0.31 in Germany and France, respectively, to between 0.32 and 0.33 in Australia, Canada, and the United Kingdom.

While they are based on smaller ranges of the distribution, the S80/S20 interquartile share ratio (Figure 8.9b) and the P90/P10 interdecile ratio (Figure 8.9c) each produce rankings similar to that of the Gini coefficient. In the rich nations with the highest

Figure 8.9 Summary distribution statistics for equivalized DHI for the richest EU and OECD nations for 2010-2011: (a) Gini coefficient, (b) interquartile share ratio (S80/S20), and (c) interdecile ratio (P90/P120). EU member country data are mainly from 2011 or 2010;non-EU OECD member country data are primarily from 2010. Gini coefficient, S80/S20 ratio, and P90/P10 ratio figures for EU member countries are based on Eurostat data and are mostly from 2010. A number of EU countries have data from 2011, including Denmark, Finland, France, Germany, Iceland, Luxembourg, the Netherlands, and Norway. Non-EU OECD member county figures for Gini, S80/S20, and P90/P10 are mainly from 2010, with some exceptions: South Korea, 2011; Japan, New Zealand, and Switzerland, 2009. Sources: Eurostat and OECD.

S80/S20 ratios, the United States and Israel, the average income among the highest- income fifth of households is 7.8 times the average income in the bottom fifth. In the less unequal Nordic and Benelux nations, the ratio ranged from 3.2 to 3.9. The P90/P10 ratio was 6.4 in Israel, followed closely by the United States at 6.1. Most of the ranking using the P90/P10 is similar to the S80/S20 ranking and, in turn, the Gini coefficient ranking, but the rich Asian nations stand out somewhat. In the Gini coefficient rankings, Japan and South Korea were similar to, and somewhat less unequal than,

Table 8.2 Summary distributional statistics for equivalized disposable household income—EU and OECD measures for 2010-2011 and the late 2000s

| Australia | Gini 0.334 | Interquintiie share ratio (S80/S20) 5.7 | Interdeciie ratio (P90/P10) 4.5 |

| Austria | 0.263 | 3.8 | 3.1 |

| Belgium | 0.263 | 3.9 | 3.2 |

| Bulgaria | 0.336 | 6.1 | 4.9 |

| Canada | 0.320 | 5.3 | 4.1 |

| Croatia | 0.31 | 5.4 | 4.5 |

| Cyprus | 0.31 | 4.7 | 3.7 |

| Czech Republic | 0.249 | 3.5 | 2.9 |

| Denmark | bgcolor=white>0.2814.5 | 3.0 | |

| Estonia | 0.325 | 5.4 | 4.4 |

| Finland | 0.259 | 3.7 | 3.1 |

| France | 0.305 | 4.5 | 3.5 |

| Germany | 0.283 | 4.3 | 3.6 |

| Greece | 0.343 | 6.6 | 4.9 |

| Hungary | 0.269 | 4.0 | 3.3 |

| Iceland | 0.240 | 3.4 | 2.6 |

| Ireland | 0.298 | 4.6 | 3.7 |

| Israel | 0.376 | 7.8 | 6.4 |

| Italy | 0.319 | 5.6 | 4.2 |

| Japan | 0.336 | 6.2 | 5.2 |

| Latvia | 0.359 | 6.5 | 5.1 |

| Lithuania | 0.32 | 5.3 | 4.4 |

| Luxembourg | 0.280 | 4.1 | 3.4 |

| Malta | 0.272 | 3.9 | 3.3 |

| Netherlands | 0.254 | 3.6 | 2.9 |

| New Zealand | 0.317 | 5.1 | 4.1 |

| Norway | 0.226 | 3.2 | 2.6 |

| Poland | 0.309 | 4.9 | 4.0 |

| Portugal | 0.345 | 5.8 | 4.6 |

| Romania | 0.332 | 6.2 | 5.2 |

| Russian Federation | 0.428 | 9 | 6.9 |

| Slovak Republic | 0.257 | 3.8 | 3.1 |

| Slovenia | 0.237 | 3.4 | 3.0 |

| South Korea | 0.311 | 5.7 | 4.8 |

| Spain | 0.340 | 6.8 | 5.2 |

| Sweden | 0.244 | 3.6 | 3.0 |

| Switzerland | 0.297 | 4.5 | 3.5 |

| Turkey | 0.448 | 11.3 | 8.5 |

| United Kingdom | 0.330 | 5.3 | 4.0 |

| United States | 0.380 | 7.9 | 6.1 |

Sources: Eurostat and OECD.

Note: Eurostat data are used forEU countries that are also OECD members. EU member country data mainly from 2011 or 2010; non-EU OECD member country data are primarily from 2010. Gini Coefficient, S80/S20 ratios, and P90/P10 ratio figures for EU member countries are based on Eurostat data and are mostly from 2010. A number of EU countries have data from 2011, including Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Luxembourg, the Netherlands, Norway, Poland, Portugal, and Slovenia. Non-EU OECD member country figures for Gini, S80/S20 ratios, and P90/P10 ratios are mainly for 2010, with some exceptions: South Korea figures are from 2011; Japan, New Zealand, and Switzerland are from 2009; and Russian Federation are from 2008.

SCV for all countries is from the OECD's “DividedWe Stand” and are primarily for 2008, except for Hungary and Turkey (2007) and Japan (2006). These statistics are no longer collected by the OECD.

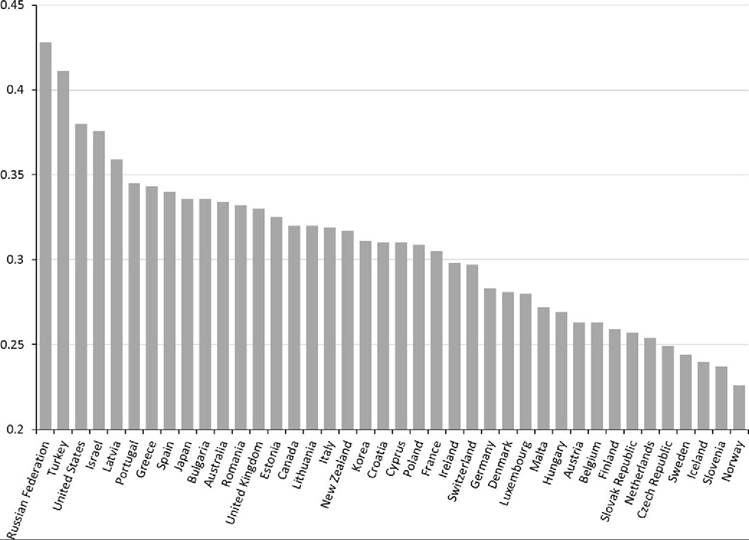

Figure 8.10 Gini coefficients for equivalized DHI for 2010-2011, including middle-income and developing EU and OECD nations. Source: EU-SILC, Eurostat data (figures for 2010/2011 for EU member countries). OECD data are mainly from 2010; exceptions include South Korea (2011) and New Zealand and Turkey (2009).

many of the Anglo-Saxon and southern European nations. Using the P90/P10, Japan and Korea appear more unequal and rank third and sixth, at 5.2 and 4.8, respectively. Among the less unequal Nordic and Benelux countries, the P90/P10 lies between 2.6 and 3.2.

The list of countries regarded as the “most unequal” or “least unequal” is, of course, somewhat dependent on the set of countries included. Figure 8.10 represents the ordered Gini coefficients for a set of countries that includes the 23 rich nations already shown in Figure 8.9 with 17 additional high-income countries, with gross domestic product per capita above $12,500 (International Monetary Fund (IMF), 2013), that are also part of EU or the OECD. In Figure 8.10, the United States is supplanted by the Russian Federation and Turkey as having the most unequal distributions using the Gini coefficient. The list of countries with less unequal distributions is similarly bolstered as the Nordic and Benelux countries are joined by several central European nations, including Slovenia and the Czech Republic. All of the summary statistics from Figures 8.9 and 8.10 are in included in Table 8.2.

8.4.1.3.3 LIS Country Summary Statistics and Rankings

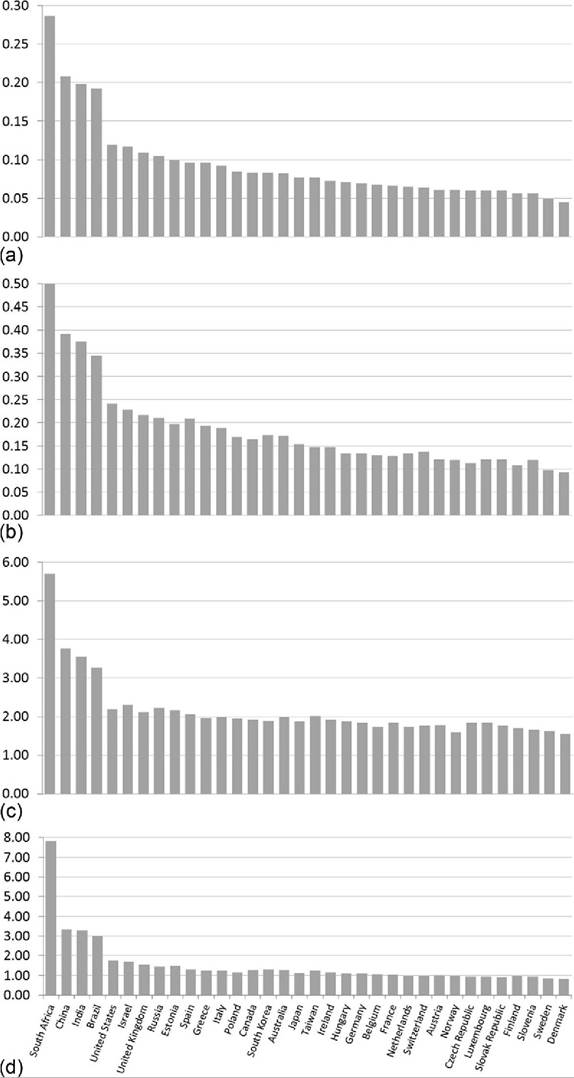

As seen in the Lorenz curves above, the LIS project includes data from a number of countries that are not part of the EU or the OECD. LIS also regularly calculates several distribution statistics not typically reported by the OECD or the EU. Figure 8.11 includes two different ATK measures (ε = 0.5, 1), the P90/P50 interdecile ratio and the Palma Index (Figure 8.11d), for 34 countries with values reported in any of the three most recent LIS waves (covering the decade of the 2000s). The data used in these figures also are included in Table 8.3.

The alternative summary statistics in Figure 8.11 maintain the same basic rank ordering among the rich countries shown in Figure 8.9, with the least unequal distributions found in the Benelux and Nordic countries and the most unequal found in the United States, Israel, and the United Kingdom. Including the MICs and developing countries that are part of the LIS project, though, alters the ranking considerably. South Africa stands out as the most unequal country by far among the 34, with an ATK of 0.29, 38% higher than second-ranked China. Using a somewhat larger inequality aversion parameter (ε = 1) results in higher measured ATK numbers but by and large preserves the rank ordering across nations (Figure 8.11a). With greater sensitivity to incomes at the bottom of the distribution, the Czech Republic’s rank (from most unequal to least unequal) falls three spots, and Switzerland’s rises five spots, but overall our understanding of which countries have more- or less-equal distributions of income is essentially unchanged by modest changes in the inequality aversion parameter.

Analysis of the P90/P50 interdecile ratio (Figure 8.11c) demonstrates the dramatic differences in the distributions of the rich EU and OECD countries from those of the MICs and developing countries in the LIS project. Israel is the rich nation with the highest P90/P50, with an equivalized DHI at the 90th percentile 2.3 times that at the median. Four LIS lower-income countries (Brazil, China, India, and South Africa) have P90/P50 ratios at least 40% higher than Israel.

Proponents of adopting the Palma Index have argued that it isolates the portions of the income distribution that are most volatile over time and across countries (Cobham and Sumner, 2013). Compared to the Gini Index (and the ATK) the Palma Index is also transparent as to which portions of the distribution are determining the measure of inequality. This feature is shared by the P90/P10, P90/P50, and S80/S20 measures. Country rankings based on the Palma Index, calculated using LIS data, are very similar to those obtained using more common measures. The Nordic countries have the least unequal distributions, with values ranging from 0.98 (Norway) to 0.82 (Denmark), whereas South Africa has the most unequal, with a Palma Index of 7.8. The United States has the highest Palma Index (1.75) among rich nations.

Figure 8.11 indicates that the country rankings are similar across all four inequality measures. South Africa is the most unequal among the 34 nations in the LIS data using all of the measures, whereas Denmark is the least unequal. The United States ranks fifth most unequal using three of the measures and seventh most unequal using the other (P90/P50).

Figure 8.11 Distributional summary statistics from LIS countries using equivalized household income in the 2000s (LIS waves VI, VII, and VIII): (a) Atkinson coefficient (e=0.5), (b) Atkinson coefficient (e = 1), (c) P90/P50 ratio, and (d) Palma Index (S10/S40 ratio). The sample years range from 2002 to 2010. Data are from the authors' analysis of LIS data. (a)-(c) are from LIS published “key figures.” (d) is based on the authors' analysis of LIS data.

Table 8.3 Summary distribution statistics from LIS using equivalized disposable household income

| Australia, 2003 | Atkinson coefficient (« ¼ 0.5) 0.082 | Atkinson coefficient (« ¼ 1) 0.172 | Percentile ratio (90/50) 1.98 | Palma Index (S90/S40) 1.28 |

| Austria, 2004 | 0.061 | 0.120 | 1.79 | 1.00 |

| Belgium, 2000 | 0.068 | 0.129 | 1.74 | 1.08 |

| Brazil, 2006 | 0.192 | 0.345 | 3.27 | 3.00 |

| Canada, 2007 | 0.083 | 0.164 | 1.93 | 1.28 |

| China, 2002 | 0.208 | 0.392 | 3.77 | 3.33 |

| Czech Republic, 2004 | 0.060 | 0.113 | 1.85 | 0.96 |

| Denmark, 2004 | 0.045 | 0.092 | 1.56 | 0.82 |

| Estonia, 2004 | 0.100 | 0.197 | 2.17 | 1.49 |

| Finland, 2004 | 0.056 | 0.108 | 1.71 | 0.98 |

| France, 2005 | 0.066 | 0.128 | 1.84 | 1.04 |

| Germany, 2010 | 0.069 | 0.133 | 1.85 | 1.10 |

| Greece, 2010 | 0.096 | 0.194 | 1.97 | 1.26 |

| Hungary, 2005 | 0.071 | 0.134 | 1.87 | 1.10 |

| India, 2004 | 0.198 | 0.375 | 3.56 | 3.29 |

| Ireland, 2010 | 0.072 | 0.147 | 1.92 | 1.14 |

| Israel, 2010 | 0.117 | 0.228 | 2.30 | 1.69 |

| Italy, 2010 | 0.092 | 0.189 | 1.99 | 1.26 |

| Japan, 2008 | 0.077 | 0.154 | 1.88 | 1.13 |

| Luxembourg, 2010 | 0.060 | 0.120 | 1.85 | 0.96 |

| Netherlands, 2004 | 0.065 | 0.133 | 1.74 | 0.98 |

| Norway, 2004 | 0.061 | 0.119 | 1.60 | 0.98 |

| Poland, 2004 | 0.085 | 0.169 | 1.96 | 1.17 |

| Russia, 2010 | 0.105 | 0.210 | 2.24 | 1.45 |

| Slovak Republic, 2010 | 0.060 | 0.120 | 1.77 | 0.93 |

| Slovenia, 2010 | 0.056 | 0.119 | 1.66 | 0.95 |

| South Africa, 2010 | 0.287 | 0.505 | 5.70 | 7.81 |

| South Korea | 0.083 | 0.173 | 1.895 | 1.31 |

| Spain, 2010 | 0.096 | 0.209 | 2.06 | 1.32 |

| Sweden, 2005 | 0.049 | 0.097 | 1.63 | 0.85 |

| Switzerland, 2004 | 0.064 | 0.137 | 1.76 | 0.97 |

| Taiwan, 2005 | 0.077 | 0.147 | 2.02 | 1.26 |

| United Kingdom, 2010 | 0.109 | 0.216 | 2.13 | 1.56 |

| United States, 2010 | 0.119 | 0.241 | 2.19 | 1.75 |

Data are based on the authors' analysis of LIS project data. The Palma Indexwas Calculatedby the authors using LIS project data, the Atkinson coefficient, and P90/P50 from LIS published “key figures.”

8.4.1.3.4 Comparing Current Distributions of Pretax and Transfer Income and DHI

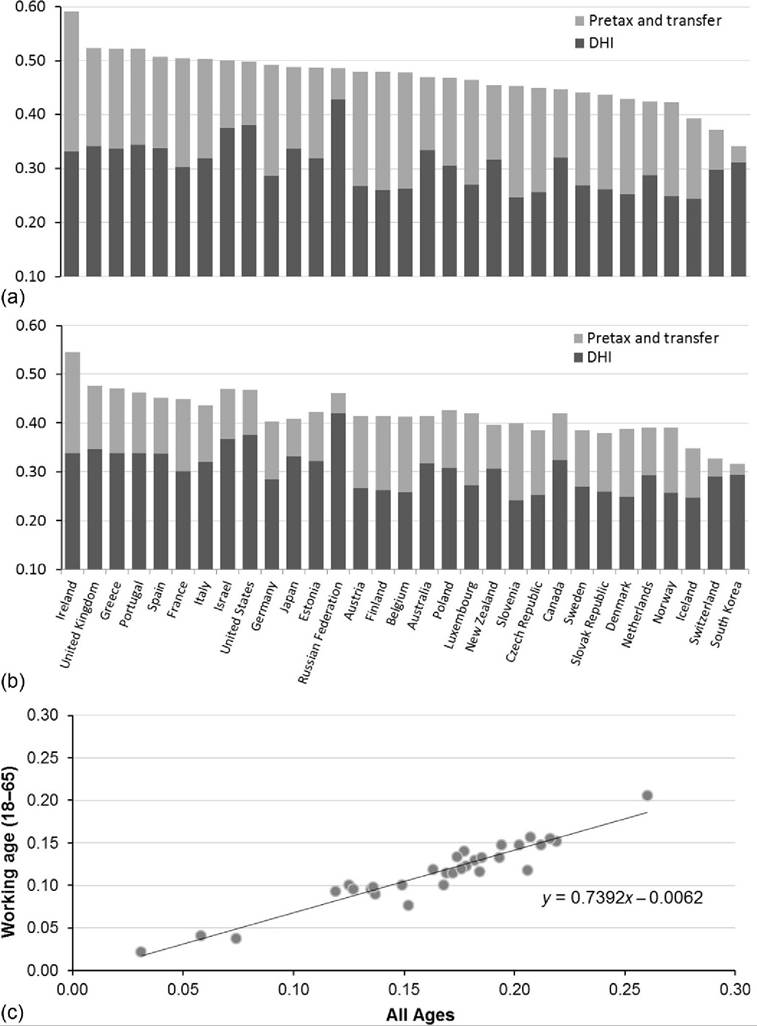

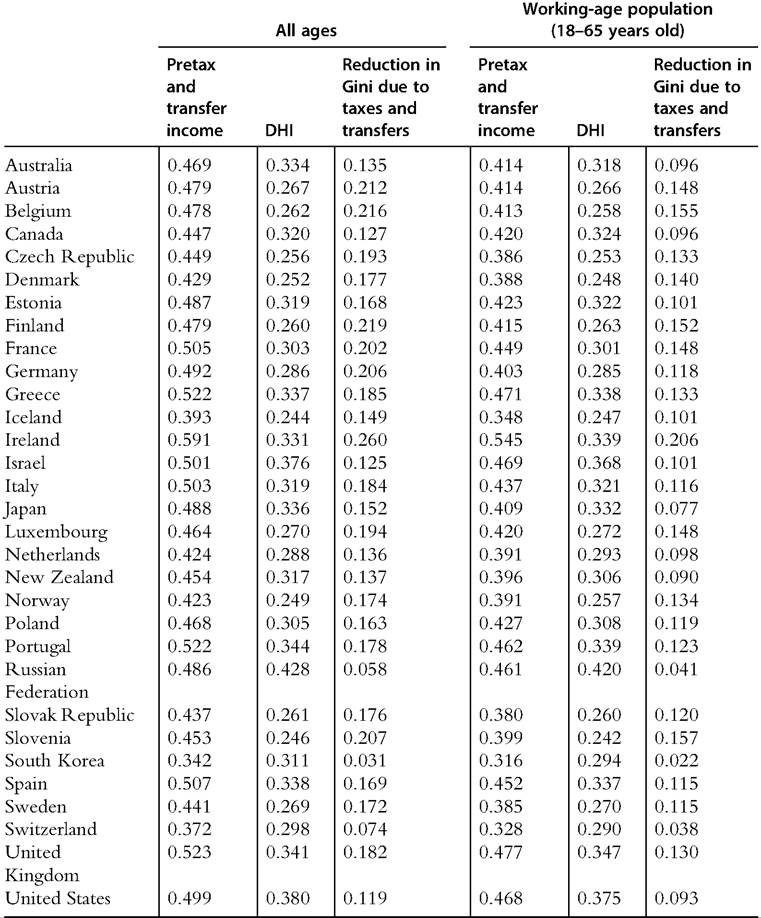

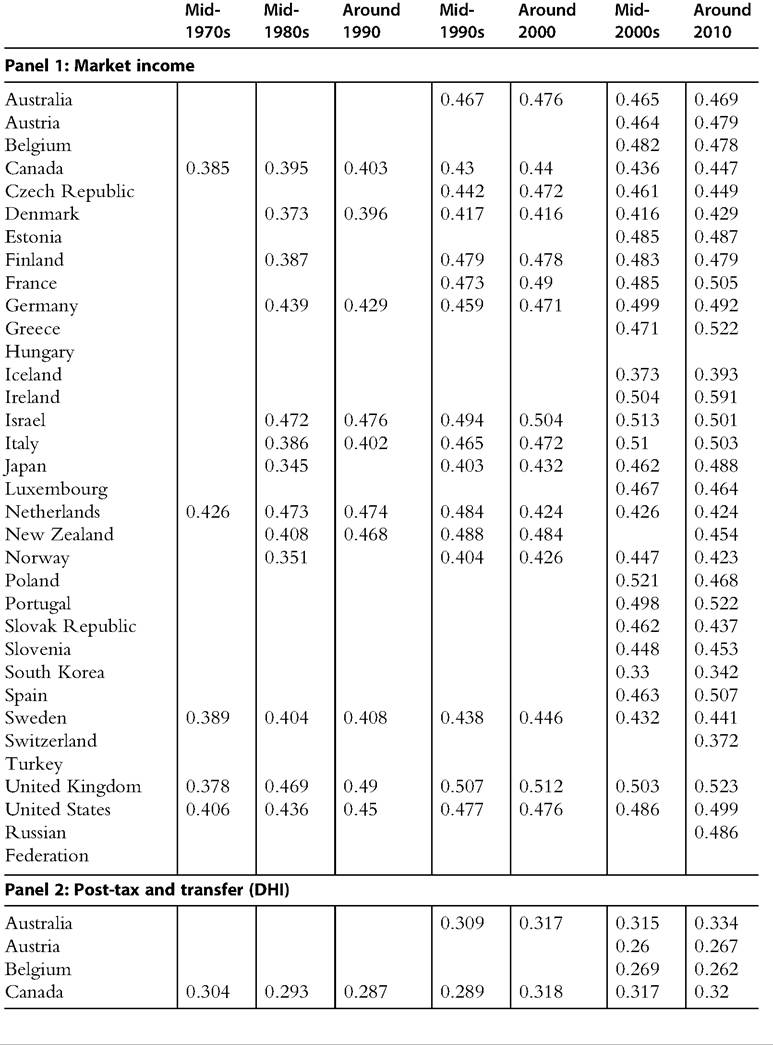

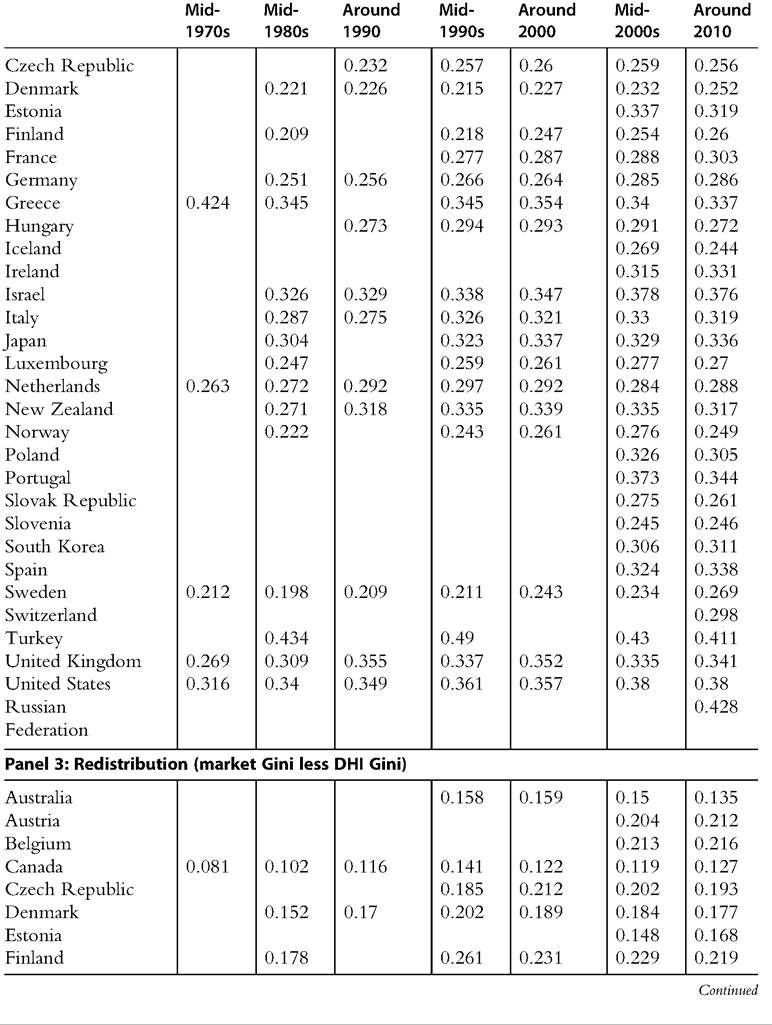

In almost every nation, and particularly among rich nations, the tax and transfer systems reduce the disparity of income. Whether taxes are paid at higher rates among upperincome households, benefits and transfer payments are directed disproportionately toward lower-income households, or both, measures of inequality are lower for DHI than for market income. The extent to which the tax and transfer systems reduce measured inequality varies substantially across countries. The distributions of DHI and pretax and transfer income, and the extent to which taxes and transfers reduce inequality, are shown in Figure 8.12 for a set of31 OECD countries. The figure shows Gini coefficients for DHI and pretax and transfer income (sorted on the latter) for all age levels (panel a) and for working-age (18-65 years old) individuals (panel b).

The rank ordering of countries based on inequality of pretax and transfer income for all ages (Figure 8.12a) is very different from the previously described rankings based on DHI. The United States does not have the most unequal distribution of pretax and transfer income, even among rich countries—it is ninth behind Ireland, Israel, the United Kingdom, and the southern European countries. The pretax and transfer income Gini for Italy is 0.50, 47% greater than South Korea, which has the lowest Gini among this set of countries. Also, instead of being clustered at the bottom, the Benelux countries are spread across the rankings based on the Gini coefficient for pretax and transfer income, and at least one Nordic country—Finland—rises to the middle.

Another important feature highlighted in Figure 8.12 is the substantial cross-national variation in the extent to which the tax and transfer systems reduce inequality. In several countries—notably the Russian Federation and South Korea—the tax and transfer systems have little impact on the distribution of income, and the Gini coefficient for DHI is only slightly smaller than the Gini for pretax and transfer income. In the case of Russia, low levels of redistribution leave the country with very high levels of inequality in DHI compared with other countries. In South Korea there is relatively little redistribution, but pretax and transfer income is distributed more evenly than in most countries, leaving a Gini for DHI that falls in the middle of the rankings.

In other countries, the tax and transfer system has a considerably larger impact on the distribution of income. In 11 countries the Gini coefficient is at least 40% lower for DHI than it is for market income. This is true for several of the Nordic and Benelux countries, as well as Ireland, Germany, and a number of eastern European countries. Substantial tax and transfer redistribution in these countries leaves them with the most equal distributions of DHI. In the case of the United States and Israel, above-average inequality in the distribution of market income combined with below-average levels of tax and transfer redistribution leave them with the highest Gini coefficients for DHI among the rich nations.

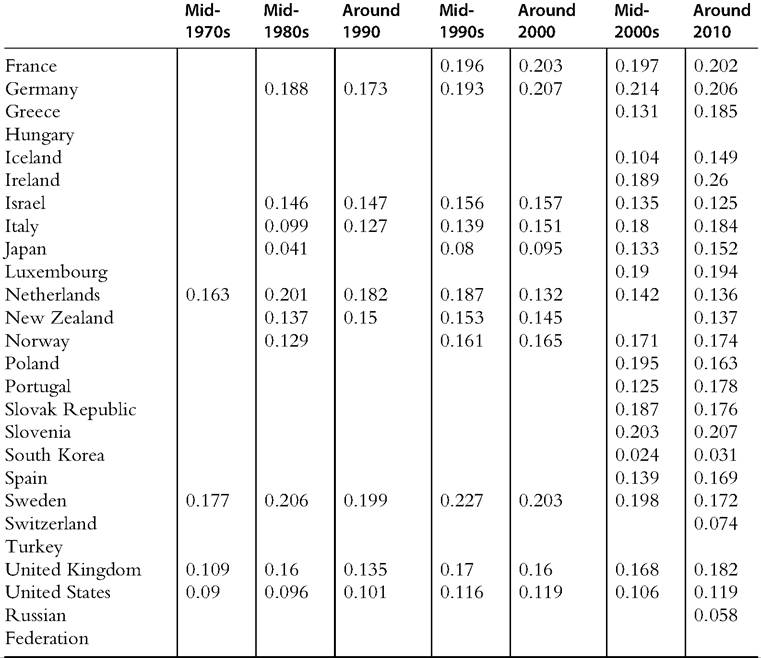

In this section we describe the difference between the Gini coefficients for pretax and transfer income and DHI as a measure of the extent of redistribution in a country. This measure of redistribution, however, has important limitations and warrants some caveats. One such caveat is that the gap between these two Gini coefficients is a distorted measure of “redistribution” because the tax and transfer policies carrying out said redistribution can be expected to cause some changes in household and firm economic behavior that

Figure 8.12 Gini coefficients around 2010 for pretax and transfer income and DHI for all ages (a), working age (18-65 years old) (b), and correlation between “redistribution” (pretax and transfer income Gini less DHI Gini) for all ages and the working-age populations (c). OECD member country data are primarily from 2010 with some exceptions: South Korea data are from 2011; Japan, New Zealand, and Switzerland data are from 2009;and the Russian Federation data are from 2008.

will be reflected in pretax and transfer income. Another limitation of this measure of redistribution is that similar types of income are classified as transfers in some countries but not in others, according to different institutional arrangements and policy choices. Retirement income systems are particularly relevant here. Countries with greater reliance on pensions provided directly by the public sector will seem to have greater redistribution than countries that finance retirement schemes through employers and private accounts (supported by tax incentives and potentially regulations).[382] A corollary is that countries with older populations (and otherwise equivalent pension systems) will seem to have greater redistribution by this measure.

We can compare the extent of redistribution across countries in a way that avoids some of these classification issues, at least in part, by using incomes from the working-age population (Figure 8.12b). Excluding retirees, who overwhelmingly rely on pension income, does not dramatically alter the rank ordering of countries based on the Gini coefficient for pretax and transfer income or the extent of redistribution observed across countries. The United States and the Anglo-Saxon and southern European countries remain the most unequal, whereas the Nordic and Benelux countries remain the least unequal. In a few countries, however, the cross-national ranking for inequality of pretax and transfer income jumps when elderly individuals are excluded; countries with notable increases include the United States, Canada, Israel, and the Russian Federation.

This extent of redistribution is greater among the total population than it is for the working-age population in every country. In the typical country the measure of redistribution for the working age is almost three quarters as large as it is for the total population (Figure 8.12c). The correlation between redistribution for all ages and for the working-age population is quite high. The simple correlation coefficient between the measures of redistribution for these two different age groups is 0.95. Countries that engage in relatively high levels of redistribution among the total population (including the elderly) also tend to engage in relatively high levels of redistribution among the working-age population. Table 8.4 contains all of the figures used in Figure 8.12.

8.4.1.4 Trends in the Distribution of Income Since 1970

Because income distribution data and statistics for some countries are only available for recent years, we are able to analyze trends in the distribution of income since the 1970s for a more limited set of countries than was discussed in the previous section. Here we first describe trends in the Gini coefficient for equivalized DHI since the mid-1970s for 10 rich nations. Then we turn to trends in the S80/S20 and P90/P10 measures, which are available for a somewhat larger number of OECD countries starting mostly in the

25

Table 8.4 Comparison of household market income and disposable household income: Gini coefficients for OECD countries around 2010

Source: OECD Inequality Database, accessed October 23, 2013. Data for most OECD countries are for 2010; exceptions include South Korea (from 2011); Ireland, Japan, New Zealand, and Switzerland (from 2009); and the Russian Federation (from 2008).

mid-1980s, but with data going back to the 1970s for a few.[383] Then we discuss trends in the Gini coefficient for pretax and transfer income and the extent to which taxes and transfers lower the Gini coefficient in a broader range of OECD countries. Finally, we compare trends in inequality since the mid-1980s using all three distributional statistics for working-age population and for all ages.

8.4.1.4.1 Trends in Equivalized DHI Gini Coefficients for 10 Rich Nations

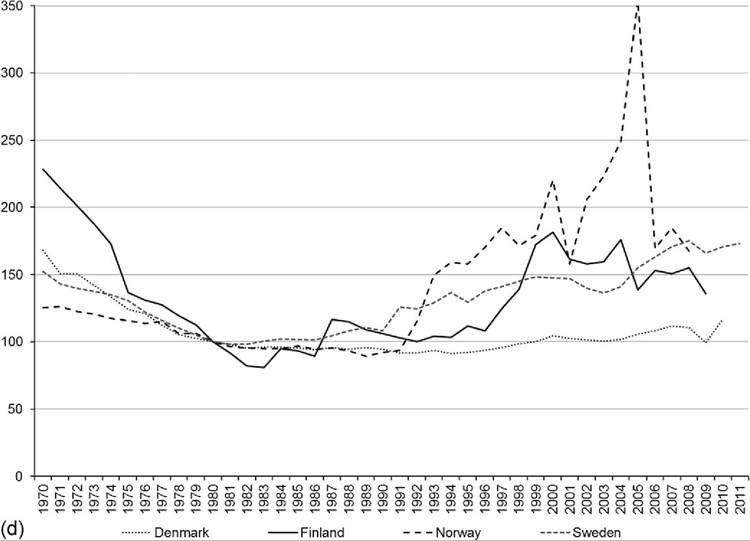

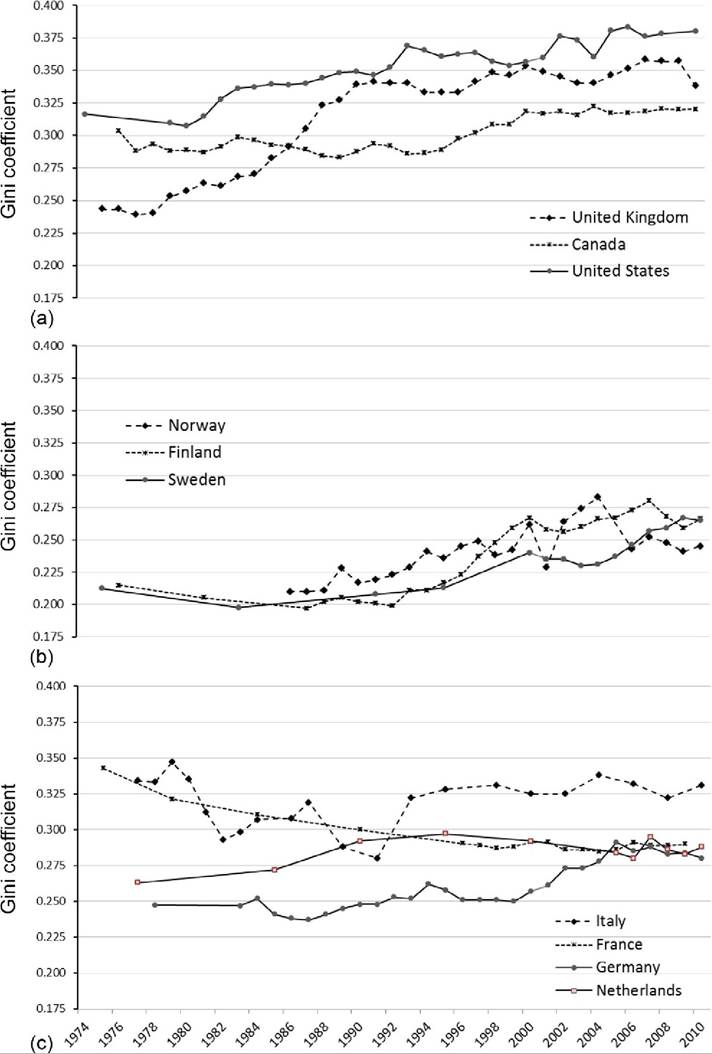

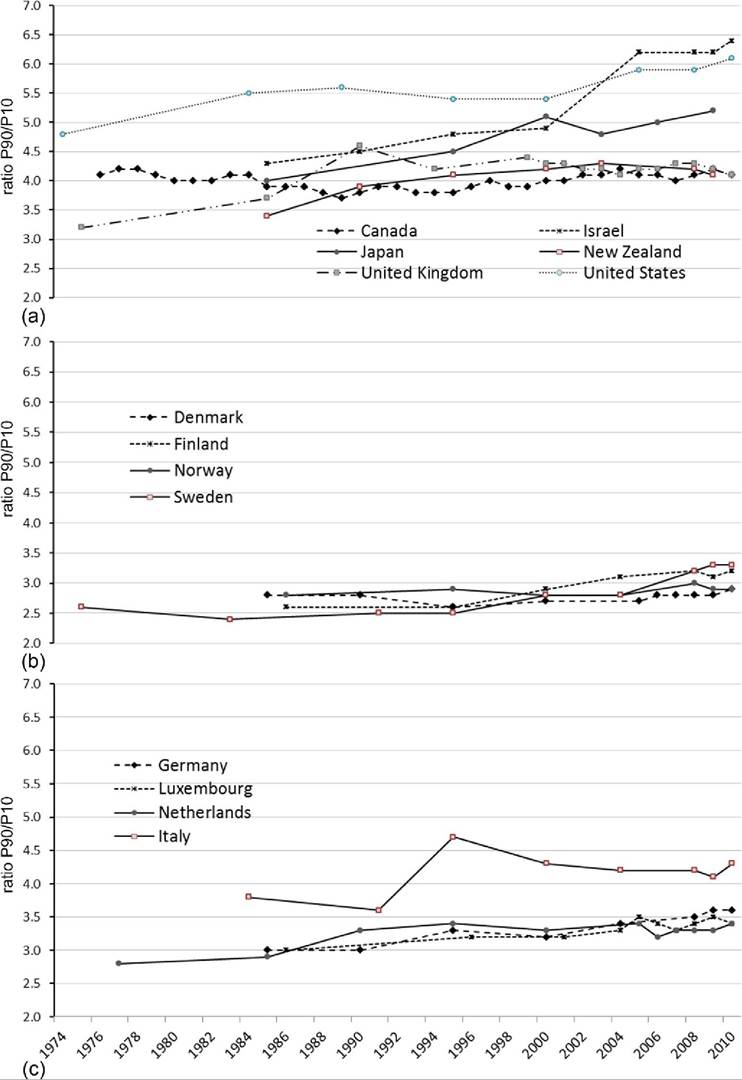

Most of the rich nations that have collected comparable, mostly annual, data since the early 1970s have experienced sizeable increases in the Gini coefficient[384] (Figure 8.13). For some countries those increases came in the 1980s (United States, United Kingdom, and the Netherlands), whereas for others they came in the 1990s and early 2000s (Canada, the Nordic countries, and Germany). Inequality trends in these countries can be thought of as following a J or U shape to varying degrees (see Gottschalk and Smeeding, 2000, for further discussion).

In Italy and France, inequality decreased in the 1980s, and since the mid-1990s the Gini coefficient has changed little in either country. Italy’s early 1980s declines were, however, offset by increases in the early 1990s (Brandolini and Vecchi, 2011). Most of the rich nations included in Figure 8.6 have experienced relatively small changes in their DHI inequality over the last 10 or 20 years, but many have witnessed marked cyclical fluctuations, particularly the United States, the United Kingdom, and the Nordic countries.

In most cases the rank ordering of countries remains unchanged after nearly 40 years of mostly rising inequality. The most dramatic shifts were undertaken by France, which had the most unequal distribution (among these rich nations) in the mid-1970s and now has a Gini coefficient only modestly higher than that of the Nordic countries. Also, the United Kingdom had among the least unequal distributions in the mid-1970s and has been among the most unequal since the early 1990s. The United States has had the most unequal distribution of income among rich nations since the early 1980s.

Rising inequality in the Nordic countries has produced relative but notable shifts as well. Through the early 1990s, the distribution of income in the Nordic countries was substantially less unequal than it was in other countries; since that time rising inequality in the Nordic countries and stable (France and the Netherlands) or modestly rising

Figure 8.13 Trends in equivalized DHI Gini coefficient in rich countries by country group, OECD, and statistical agency data: Anglo-Saxon countries and the United States (a), Nordic countries (b), and Continental and Southern Europe (c). Source: OECD income distribution data for Canada, Sweden, and United States. Inequality Chartbook (Atkinson and Morelli, 2012, 2014) based on figures published by statistical agencies for remaining countries and updated by authors. Data for Italy from Smeeding and Brandolini (2009), updated by Brandolini.

inequality (Germany) in other countries has produced some convergence in the inequality levels in continental Europe and the Nordic countries. In Germany, the Gini of DHI rose 14% (from 0.25 to 0.28) over the period.[385] Although the distribution of income was less unequal in the Lander of the former East Germany (EDHI Gini of 0.20 in East Germany and 0.25 in West Germany in 1991), reunification had little impact on the inequality trends for Germany (Fuchs-Schiindeln and Schiindeln, 2009; Grabka and Kuhn, 2012).

Compared with the early 1980s, the range of inequality measures of these 10 rich countries has become somewhat more compressed. The two nations that previously had the most equal distributions—Sweden and Finland—experienced some of the largest increases in inequality. Around 1980, this set of 10 rich countries had a mean DHI Gini of 0.265 with a variance of 0.0022; around 2010 the mean had increased to 0.30, while the variance had decreased to 0.0017.

8.4.1.4.2 Trends in the S80/S20 and P90/P10 Measures for Equivalized DHI for 14 OECD Countries

A somewhat larger group of countries has been collecting comparable income data at least since the early 1980s (with Denmark, Israel, Japan, Luxembourg, and New Zealand augmenting the 10 rich nations discussed in the previous section).[386] The OECD has analyzed the income surveys from those countries and calculated S80/S20 and P90/P10 ratios. Both of these alternative measures yield largely similar trends in income inequality to what we saw for the Gini coefficient in Figure 8.13.

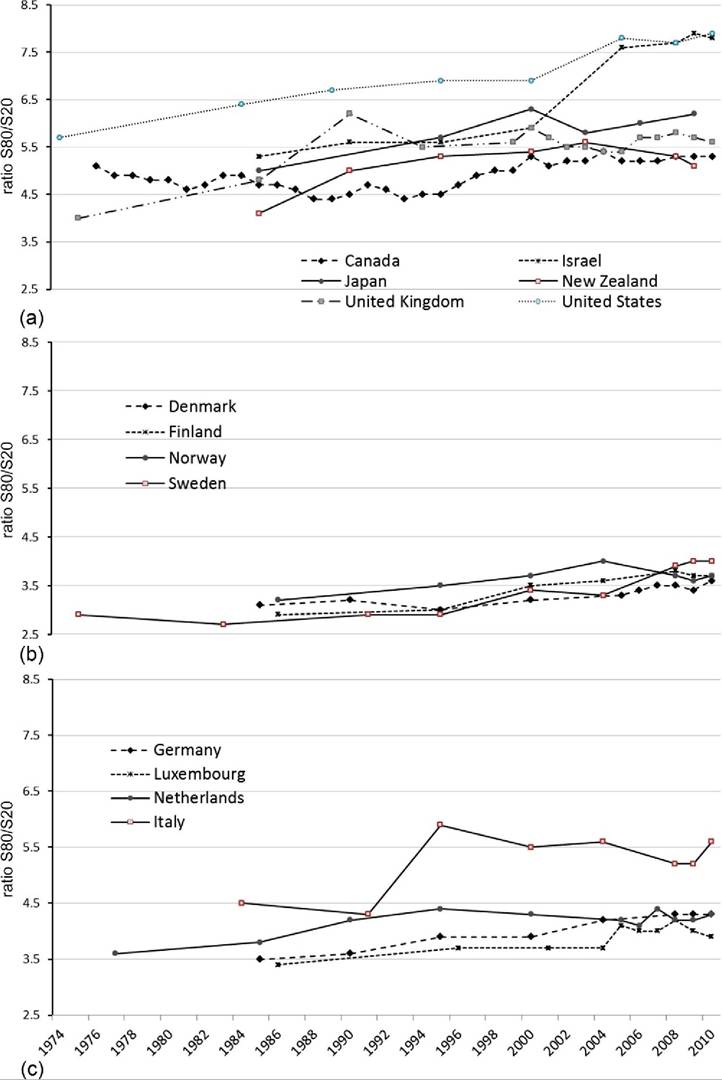

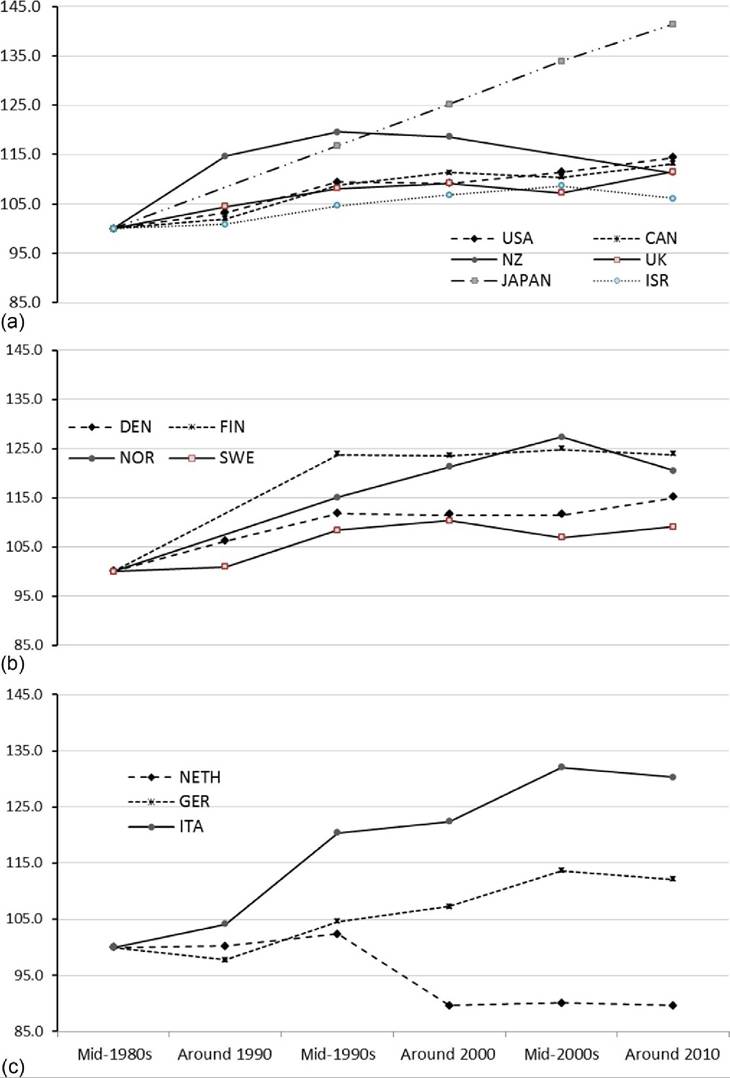

The share of income received by the top quintile divided by the share of income received by the bottom quintile (S80/S20) has increased in each of these countries since the early 1980s, but some countries experienced larger increases in inequality, and the rank ordering changed somewhat (Figure 8.14). Israel experienced the largest absolute change over this period, with its S80/S20 rising by 2.5, basically matching the United States for top spot with the top fifth of households receiving 7.8 times as much income as those in the bottom fifth. Israel’s inequality surge occurred in the late 1990s and early 2000s. Sweden experienced the largest relative increase over the same period—its S80/ S20 increased 48%. Canada experienced the smallest increase among these countries: its S80/S20 increased less than 10% higher than its lowest point in the 1980s.

Shifting to an inequality measure that further sharpens the contrast between the top and bottom of income distribution, the P90/P10 interdecile ratio does little to change the trends (Figure 8.15). Similar to the S80/S20 measure, income inequality did increase in each of the countries over this period. For Israel and Japan, the distribution seems to have

Figure 8.14 Trends in S80/S20 ratio for equivalized DHI by country group based on OECDdata: Anglo- Saxon countries, the United States, and others (a);Nordic countries (b);and Continental and Southern Europe (c). Source: OECD income distribution data.

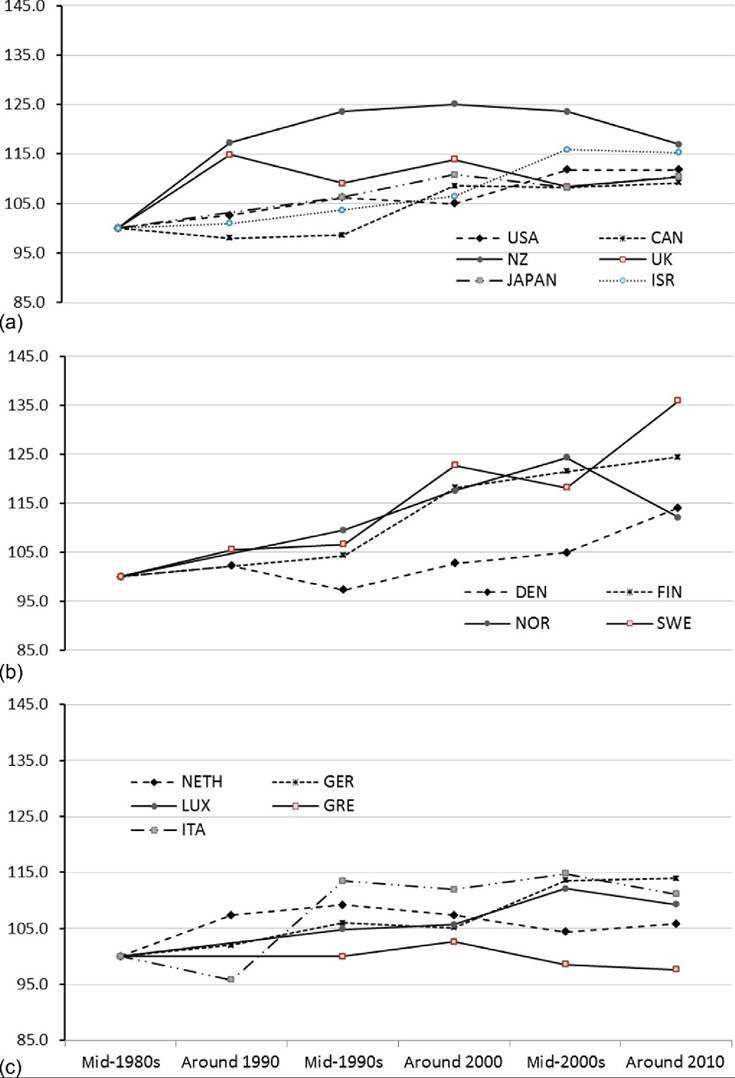

Figure 8.15 Trends in P90/P10 ratios for equivalized DHI by country group based on OECD data: Anglo-Saxon countries, the United States, and others (a);Nordic countries (b);and Continental and Southern Europe (c). Source: OECD income distribution data.

grown even more unequal using the P90/10 ratio. By the mid-2000s Israel had supplanted the United States as the most unequal rich nation, with households at the 90th percentile receiving DHIs 6.4 times greater than those at the 10th percentile. InJapan the P90/P10 ratio rose 30% over these three decades.

In most cases, though, the increase in inequality since the early 1980s is equivalent to or somewhat smaller than what is indicated by trends in the S80/S20. In the case of Canada, the 2010 value for the P90/P10 ratio was equal to its 1983 value but 0.4 above its low point in the 1980s. In all of the Nordic and continental European countries (except the Netherlands), the P90/P10 ratio increased less in percentage terms than the S80/S20 did over the same period.

8.4.1.4.3 Trends in Pretax and Transfer Gini Coefficients and the Extent of Redistribution for OECD Countries

Trends in the distribution of pretax and transfer income (using the Gini coefficient) and the extent of redistribution can be explored using the same data, which are available for an expanded set of OECD countries, though for some only since the mid-1990s.

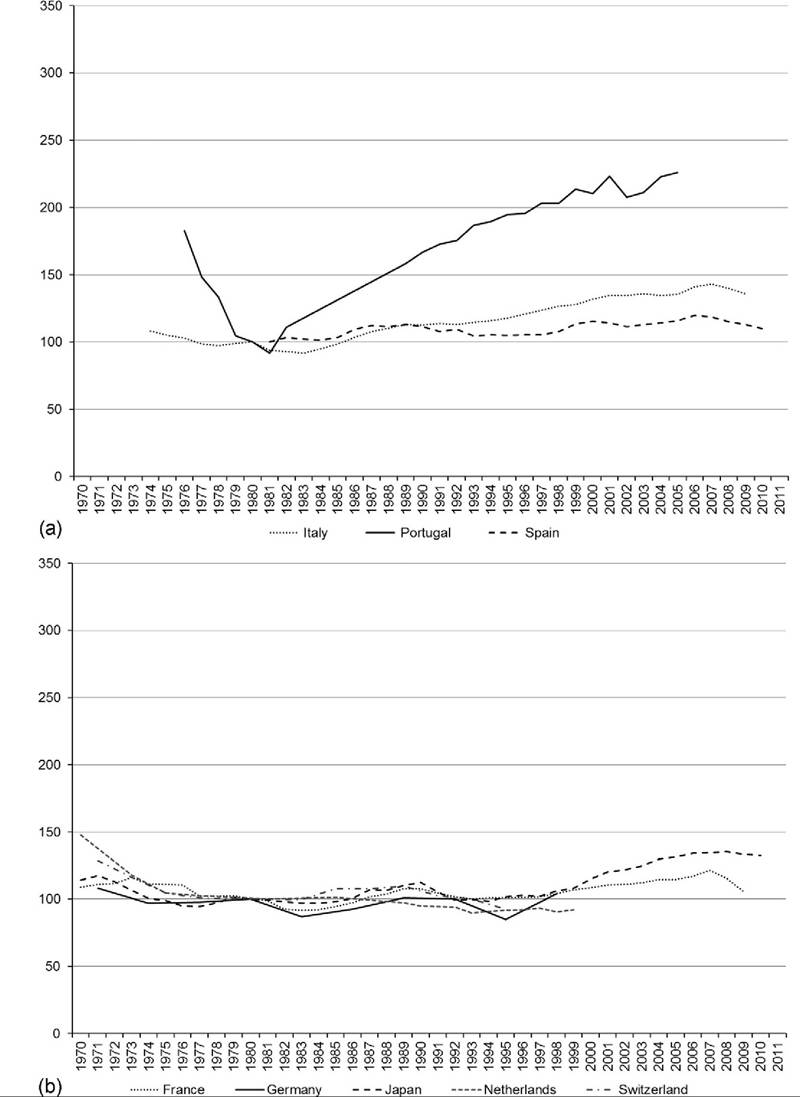

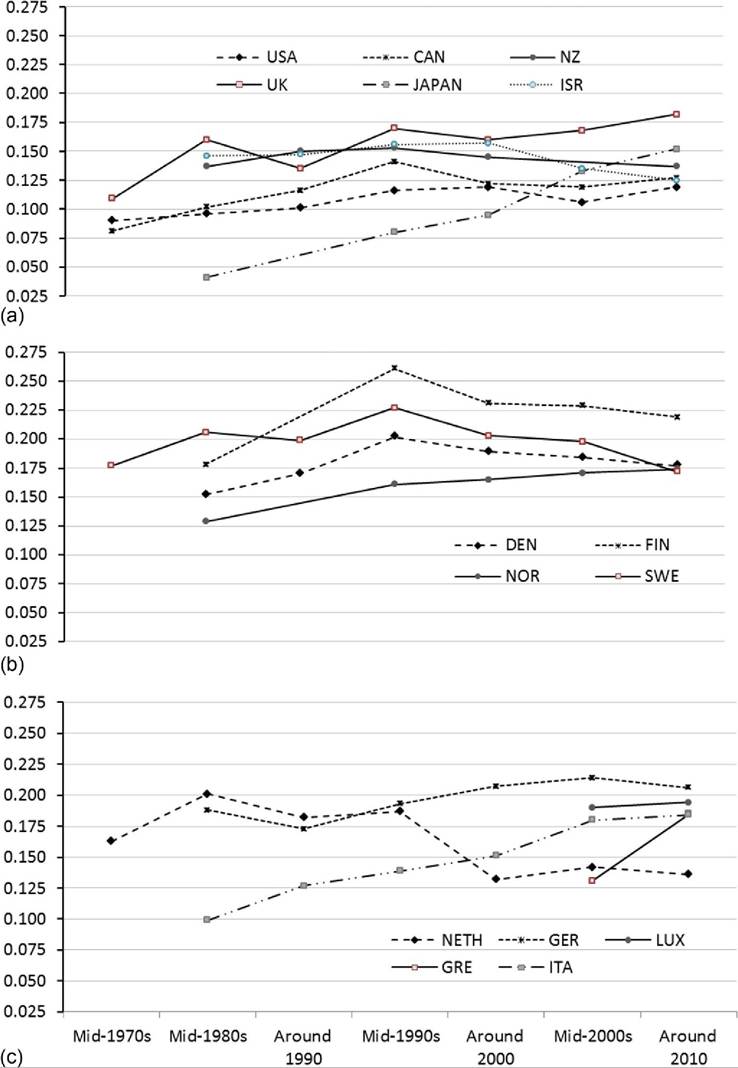

Japan is the country with the largest increase in pretax and transfer inequality among these high-income countries, increasing more than 40% and going from the least unequal distribution in the mid-1980s to one of the most unequal in 2010 (Figure 8.16a). (Figures 8.16 and 8.17 include only countries with data available for the mid-1980s and show the percentage change relative to the mid-1980s base.) Italy also experienced relatively large increases in inequality over this period, with its pretax and transfer Gini increasing 30% (Figure 8.16c). Pretax and transfer inequality increased in most of these countries. In the Anglo-Saxon countries and the United States, the increases were concentrated in the 1980s and early 1990s; in the Nordic and continental European countries Gini coefficients increased most in the early 1990s. The only country that seemed to avoid increased pretax and transfer inequality was the Netherlands. The pretax and transfer Gini actually fell more than 10% in Finland in the late 1990s. For the US, the Netherlands, and Finland, however, data are only available since the mid-1990s. In the Netherlands, increases in the pretax and transfer Gini coefficient in the 1980s were offset by decreases in the late 1990s. New Zealand also experienced declining inequality in the 2000s. A number of countries (including Finland, Israel, and Sweden) have witnessed very little change in pretax inequality over the past 15 years; Gini coefficients have fluctuated only slightly between the mid-1990s and 2010.[387]

Incorporating the influence of taxes and transfers can produce inequality trends that seem quite different, in some cases, than what we see in market or pretax and transfer

Figure 8.16 Change in pretax and transfer income Gini (mid-1890s = 100) for OECD countries, by country group: Anglo-Saxon countries, the United States, and others (a);Nordic countries (b);and Continental and Southern Europe (c). Source: OECD Inequality Database, accessed October 23, 2013.

Figure 8.17 Change in disposable household income Gini (mid-1980s = 100) for OECD countries, by country group: Anglo-Saxon countries, the United States, and others (a);Nordic countries (b);and Continental and Southern Europe (c). Source: OECD Inequality Database, accessed October 23, 2013.

income. (See Deding and Dall Schmidt, 2002 for an earlier analysis of this issue during the 1990s.) Trends in the Gini coefficients using equalized DHI for the same countries over the same period are shown in Figure 8.17. For some countries trends for the DHI and pretax and transfer Gini coefficients are very similar. The United States, for example, saw the pretax and transfer Gini coefficient increase 14% between the mid-1980s and 2010, while its DHI Gini coefficient increased 12%. The United States is one of the countries for which excluding trends for the 1970s substantially understates its increase in inequality; between the mid-1970s and 2010 the U.S. pretax and transfer Gini increased 23% and its DHI Gini increased 20%.

Denmark, Finland (Figure 8.17b), and Germany (Figure 8.17c) also saw similar increases in the Gini coefficient before and after the inclusion of taxes and transfers. For a number of countries, though, the inclusion of taxes and transfers produces markedly different trends in inequality. For Canada, Japan, Italy, Norway, and the United Kingdom, rising inequality in the distribution of income is blunted once taxes and transfers are included. Japan and Italy, the countries with the largest increases in pretax and transfer inequality in Figure 8.16, experienced increases in their DHI inequality only one-quarter and one-third as large, respectively. The opposite is the case for Sweden, the Netherlands, Israel, and New Zealand, which experienced larger increases in inequality after including taxes and transfers. In the case of Sweden, the Gini for pretax and transfer income increased 9% (from 0.40 to 0.44) between the mid-1980s and 2010, while the Gini for DHI increased 36% (from 0.19 to 0.27).

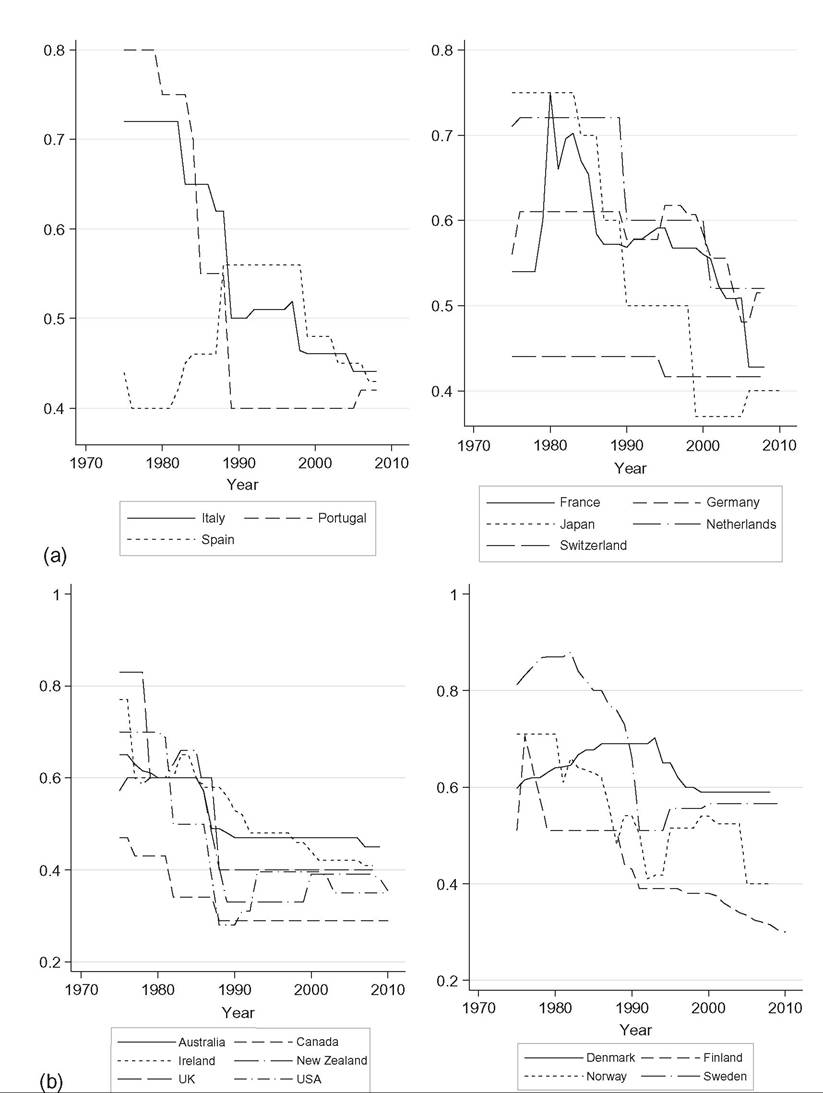

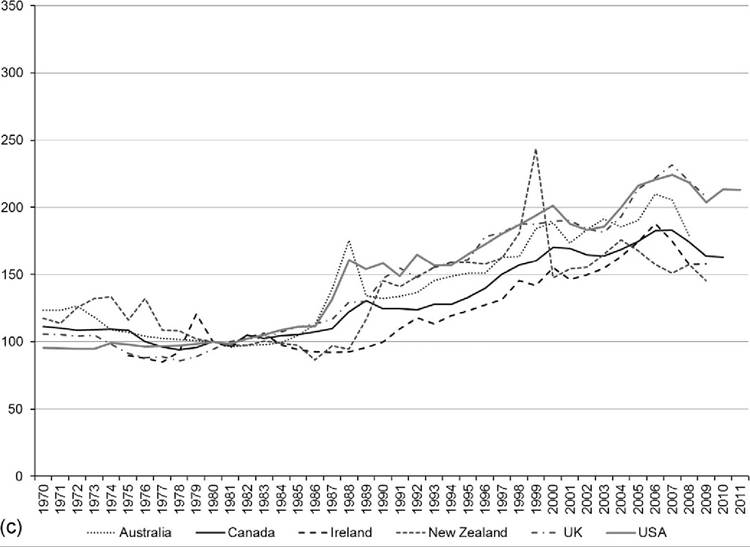

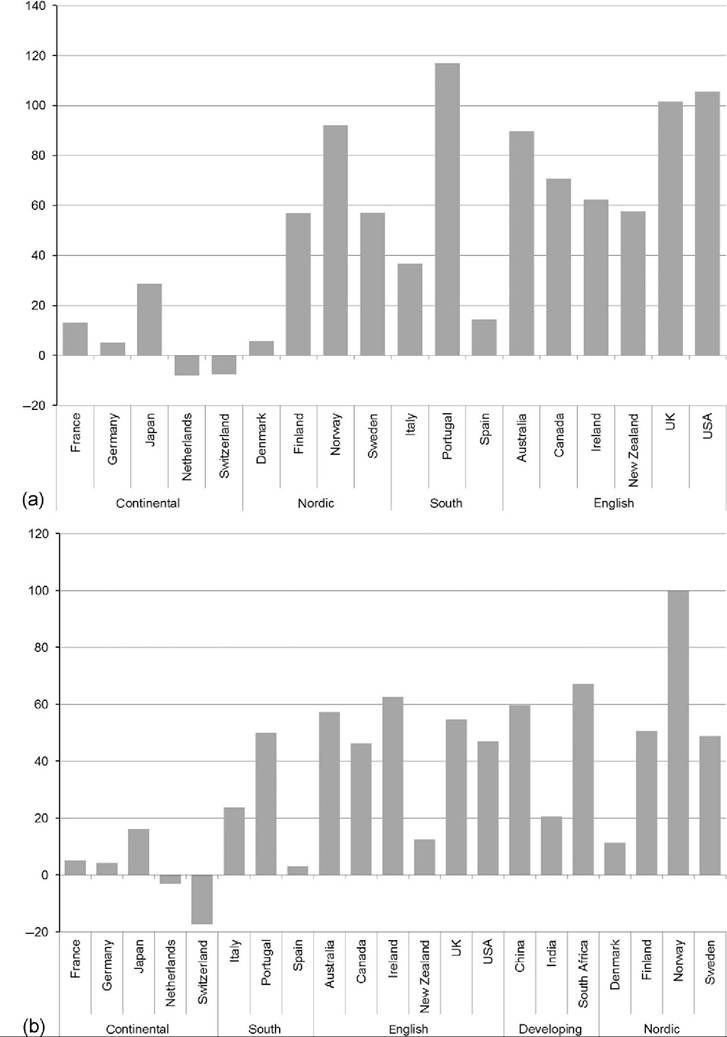

The differences in the trends illustrated in Figures 8.16 and 8.17 are partly a result of the evolution of the tax and transfer systems in these countries. (As mentioned previously, changes in the age of the population and other demographic and policy factors can influence these trends as well.) Figure 8.18 shows how the extent to which tax and transfers reduce the Gini coefficients for pretax and transfer incomes has changed over this period. The most striking pattern in Figure 8.18 is the dramatic and sustained increase in tax and transfer “redistribution” in most rich nations from the mid-1970s through the mid- 1990s, which was followed by steady declines in the decade and a half since. The Anglo-Saxon (Figure 8.18a) and Nordic countries (Figure 8.18b) in particular followed an inverse U-shaped pattern, with redistributive efforts increasing between the mid- 1970s and mid-1990s but declining after that point. Since around 2000, taxes and transfers also have played a smaller role in reducing market income inequality in Israel.

In some countries the redistributive impact did not subside in the 1990s. Japan (Figure 8.18a) and Italy (Figure 8.18c) both experienced steady increases in redistribution from the 1990s through the late 2000s. The impact of redistribution has fluctuated less in the United States than in most other high-income countries. Increased redistribution in Canada and Japan, though, has shifted the United States from having one of the lowest levels of redistribution to having the lowest among rich nations. (See Caminada et al., 2012; Immervoll and Richardson, 2011; Wang and Caminada, 2011, for more detailed

Figure 8.18 Reduction in Gini coefficient due to taxes and transfers trends for OECD countries, by country group: Anglo-Saxon countries, the United States, and others (a);Nordic countries (b);and Continental, Southern, and Eastern Europe (c). Source: OECD Inequality Database, accessed October 23, 2013.

discussion of the specific policies and their contribution to reducing market inequality in OECD and LIS countries.) Gini coefficients for pretax and transfer income, DHI, and the difference between the two for the OECD countries are shown in Table 8.5.

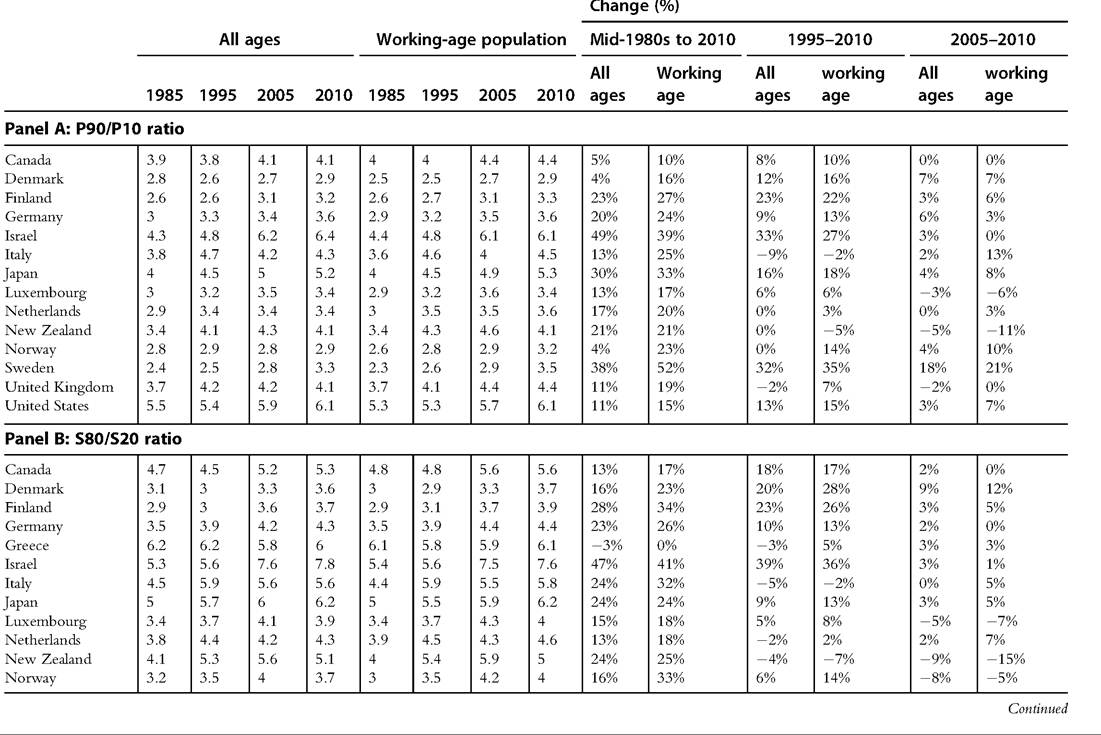

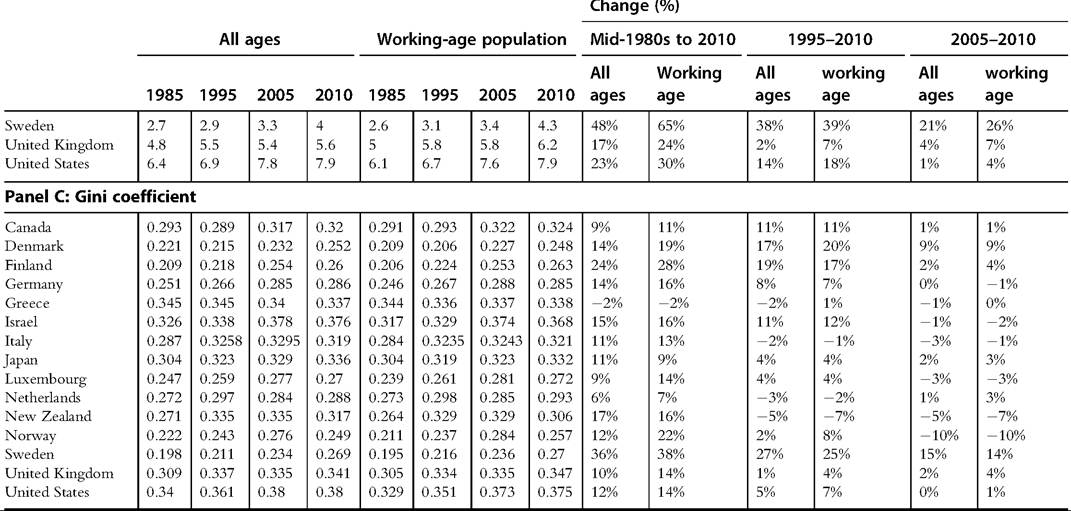

8.4.1.4.4 Comparing Trends in DHI Inequality for All Ages and the Working-Age Population We previously described how age composition is important in understanding how taxes and transfers affect cross-national rankings of income inequality. We can use the same OECD data to evaluate trends in income distribution statistics for the working-age population and contrast them with trends for the overall population. Table 8.6 includes S80/S20 and P90/P10 ratios, as well as Gini coefficients using equivalized DHI for a selection of years between the mid-1980s and 2010 for high-income OECD countries.

Over the entire 25-year period, the distribution of income grew even more unequal among the working-age population in almost every country. The largest differences can be seen among the Nordic countries. In Norway and Sweden, the P90/P10 ratio increased 20% and 15% more among the working-age than for the overall population, respectively, between the mid-1980s and 2010 (panel A). Smaller differences can be seen for the United States, United Kingdom, and Canada, which saw inequality increase between 4% and 8% more among the working-age than among all ages combined. Israel is the only country to see larger increases among the overall population than the workingage, although New Zealand also saw larger increases among the overall population after the mid-1990s. For some of the countries, though, there is no notable difference in the inequality trends between the working-age and the overall population at any point, or at least in more recent years.

The S80/S20 ratio measure yields a strikingly similar pattern of results (panel B) as the P90/P10 ratio, but differences in Gini coefficient trends between the age groups (panel C) are more muted. Norway and Denmark saw DHI Gini coefficients increase 10% and 5% more, respectively, among the working-age than the overall population between 1985 and 2010. In most countries, however, trends in the Gini coefficient were only modestly greater among the working-age population. The tails of the distribution have a greater impact on the S80/S20 and P90/P10 measures than they do on the Gini coefficient and seem to be particularly relevant to understanding any differences in inequality trends for different age groups.

8.4.2 Top Incomes

8.4.2.1 Introduction

The first empirical section of this chapter focused on incomes at the bottom of the distribution relative to the poverty line. The previous section discussed trends in the overall distribution ofincome (e.g., Gini coefficients), suggesting that the distribution of income has become more unequal in most countries since the 1970s. This section shifts attention to the top of the distribution. Top incomes deserve a separate discussion because top

Table 8.5 Gini index for market income and post-tax/transfer income and the extent of redistribution

Table 8.5 Gini index for market income and post-tax/transfer income and the extent of redistribution—cont'd

Table 8.5 Gini index for market income and post-tax/transfer income and the extent of redistribution—cont'd

Source: OECD Inequality Database, accessed October 23, 2013.

Note: For most OECD countries, “Around 2010” is for the year 2010, with some exceptions: for South Korea, data are for 2011; for Hungary, Ireland, Japan, New Zealand, Switzerland, and Turkey, data are for 2009; and for the Russian Federation, data are for 2008.

income measures taken from household surveys are typically less accurate because ofboth sampling and nonsampling errors.

The main objective of this section is to discuss the trends of the so-called top income shares as computed from administrative tax statistics. Different from Chapter 7, we focus here on the investigation of the four decades since 1970. Moreover, we mainly describe here the trends in top shares, leaving out a discussion of what may have driven such trends (see Part III of this volume). The methodological issues affecting the comparison of trends over time and across countries also define a substantial part of this section. Indeed, we start

Table 8.6 Comparing trends in equivalized DHI inequality for all ages and for the working-age population, by measure by country

Table 8.6 Comparing trends in equivalized DHI inequality for all ages and for the working-age population, by measure by country—cont'd

Source: OECD Income Distribution Database, accessed November 8, 2013. Some data for some countries are from the following years: Finland, 1986, 2004; Greece, 1986, 1994; Italy, 1984, 2004; Japan, 2006, 2009; Luxembourg, 1986, 1996; New Zealand, 2003, 2009; Norway, 1986, 2004; Sweden, 1983, 2004; United Kingdom, 1994; United States, 1984.

here with an overview of the main features and limitations of the data with the objective of highlighting how the latter can affect the comparability of the top shares over time and across countries. Where possible, we illustrate how income at the top can be decomposed by different sources, highlighting the role of capital and wage incomes. Similarly, we provide a brief description of the impact of fiscal policy on the top income shares after taxes. Differences in tax systems can affect differently the level as well the trend of top shares across countries. Finally, we discuss how we can complement the two sources of information (tax and survey statistics) to improve our understanding of the evolution ofincome inequality.

The analysis in this section uses data on total income of the families, tax units, and individuals above the 99th percentile of the distribution. Therefore, unlike Chapter 7, this chapter does not focus on different income groups within the top decile. The data are collected and assembled from tax statistics, available from the World Top Incomes Database (WTID) by Alvaredo et al. (2012). The database is the result of years of work in a line of research initiated by FrankelandHerzfeld (1943)31 and Kuznets (1953), revived by Piketty (2001), and carried on in subsequent collective works directed by Atkinson and Piketty (2007, 2010), who pulled together a number of contributions from different authors.

Motivations for the surge of interest in incomes at the top of the distribution vary. On one hand, the WTID database constitutes a unique source of information covering most of the twentieth century (and in a few cases the beginning of the twenty-first century as well). As shown in great detail in Chapter 7, this is a crucial advantage for studies of income distribution, which are usually plagued by data limitations.