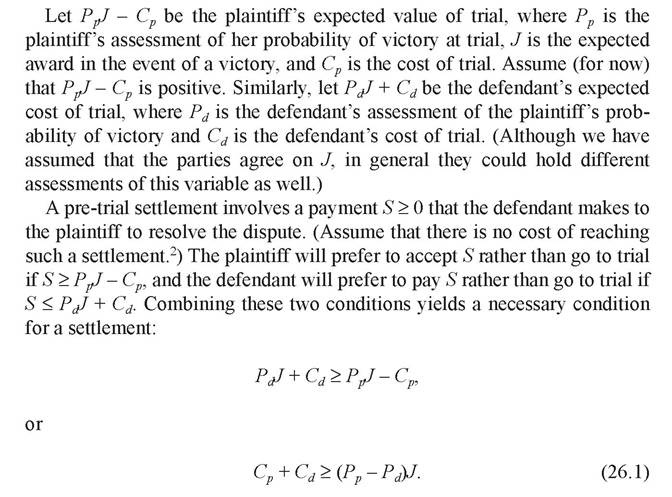

Modelling the settlement-trial decision

Consider the following simple model of a legal dispute. A plaintiff files a lawsuit in an effort to recover monetary damages against a defendant.1 Prior to trial, the parties engage in bargaining in an effort to arrive at a settlement.

In fact, the vast majority of civil actions result in settlements and therefore never go to trial. An economic model of dispute resolution seeks to explain this fact by showing the mutual gains to the parties from settling outside of court. This turns out to be easy; the more difficult task is to explain why a small percentage of cases actually go to trial. A simple model illustrates both the gains from settlement and possible reasons for trial.

reasons for trial. If this condition holds, there exists a value of S that is mutually acceptable to the parties compared to trial. That is, a ‘settlement range’ exists.

Note that this condition necessarily holds if Pp = Pd, or if the parties agree on the expected outcome of a trial. This makes sense since, if the parties agree on how the court will settle the dispute, they can implement the same outcome in a settlement while saving the joint cost of trial, Cp + Cd. An additional reason for settlement not captured in this model is that risk-averse disputants will prefer the certain outcome of a settlement as compared to the uncertain outcome of a trial.

The simple bargaining model of litigation thus provides two reasons for out-of-court settlements: avoiding the costs of a trial and avoiding the uncertain outcome of a trial. However, it remains to explain why, despite these gains, some cases still end up at trial. One explanation for a trial is that the inequality in (26.1) is reversed so that a range for S' does not exist. Note that this requires Pp - Pd to be positive and larger than the ratio of the joint costs of a trial to the expected judgment. One way Pp - Pd can be positive is if the parties hold differing perceptions about the outcome of a trial.3 In particular,

Pp > Pd reflects optimism by both parties about their prospects at trial.

Optimism about the outcome of a trial can arise from different views by the parties about the strengths of their cases, about the relevant law, or it may simply arise from irrationality (Cooter and Ulen, 1988, p. 487).Another reason why (26.1) may not hold in a given case is that the parties may possess asymmetric information about the value of trial.4 For example, suppose that a particular plaintiff knows her probability of victory at trial, Pp, but the defendant only knows the distribution of Pp across the population of all plaintiffs, where the variation in Pp could reflect, in the case of an accident, differences in the extent to which plaintiffs were contributorily negligent.5 Suppose that, in this setting, the defendant makes a single, take-it-or-leave-it settlement offer, 5, to minimize his expected costs.6 As long as the costminimizing choice of 5 (denoted 5*) is less than the expected value of trial for the plaintiff with the highest expected value in the population, some cases will go to trial. In particular, plaintiffs with PpJ - Cp £ 5 will accept the offer and settle, while plaintiffs with PpJ - Cp > 5 will reject the offer and go to trial.

Even when inequality (26.1) is satisfied, implying the existence of a settlement range, a trial can still occur if the parties are unable to decide on the division of the gains from settlement. If they cannot agree on the division, bargaining may break down and a trial will ensue (Cooter et al., 1982).