VERTICAL RESTRAINTS IN INTERNET COMMERCE

Apart from the highly visible and hotly debated Google cases, there have been numerous cases in Europe regarding the use of vertical restraints in online markets. The development of the Internet as a powerful channel for the distribution of goods and services has created new platforms and sellers such as eBay, Amazon, Expedia, Booking.com and so on.

The most common vertical restraints in online commerce are the following:• general bans on online sales by manufacturers;

• agreements limiting the absolute quantity or percentage of online sales;

• dual pricing strategies with higher wholesale prices for online sales and lower wholesale prices for offline sales;

• selective distribution schemes; and

• across-platforms parity agreements (APPAs).

The most common restraint is probably the complete or partial restriction of online sales. One of the earliest cases was Yves Saint Laurent perfume. In this instance, in 2001 the European Commission approved that online sales could be restricted to retailers who were already operating brick-and-mortar stores.10 The Commission recognized that certain products cannot be properly supplied without specialized distributors, especially if the product’s quality needs to be preserved or its proper use ensured.

The French competition authority reached a very similar conclusion in 2006 and 2007, as did the appeals court, when a pure online retailer (Bijourama) wanted to enter the Festina France selective distribution system in the market for (expensive) watches. The authority and the court stressed that a manufacturer with a market share below 30 percent can limit online sales as long as the criteria are transparent and used consistently. Hence, the exclusion of a purely online dealer was ruled to be legal. A similar decision was reached in 2007 regarding several selective distribution systems for high-end cosmetics and hygiene products (Bioderma).

In 2002, a Belgian court ruled that even the complete ban on online sales that Makro imposed on its selective distribution networks of luxury perfumes and cosmetics was legal, because the products’ nature required personal expert guidance and the sales methods could not be replicated over the Internet.

The most prominent case was the Pierre Fabre ruling, where in 2009 the European Court of Justice ruled that a de facto ban on online sales (through the requirement of a qualified pharmacist to assist the sale) should be regarded as an infringement ‘by object’ of Article 101(1) TFEU. Put differently, the ban on Internet sales is regarded as a hardcore restriction, even though the Paris court to which the case was referred noted Pierre Fabre’s 20 percent market share and the lively inter-brand competition.

There are several other cases dealing with selective distribution systems, some of which are summarized in Buccirossi (2013, 2015), Dolmans and Leyden (2012), Vogel (2012), ICN (2015) and Dolmans and Mostyn (2015). In principle, European competition authorities tend to take a rather strict view, focusing on the protection of intra-brand competition without much analysis of the degree of inter-brand competition and the economic effects on consumers and the competitive process as such.

This is also reflected in proceedings against various companies for engaging in dual pricing. Dual pricing means that retailers are granted different wholesale prices depending on whether they intend to sell the product online or over the counter. While wholesale price discrimination between different retailers and different retail channels is perfectly in line with naive profit maximization in all but perfectly competitive industries, European competition authorities have - in contrast to the USA - viewed this pricing practice with great skepticism when applied to Internet commerce. For example, Bosch Siemens Home Appliances (BSH) introduced a new rebate system in 2013 with lower performance rebates for online sales.

BSH argued that different rebate levels were aimed at compensating brick-and-mortar dealers and sales for their high-quality sales services in comparison with online dealers. However, the German Cartel Office took the view that lower rebates for online sales create incentives for hybrid dealers to sell less online, which reduces competition through online sales and is therefore without further analysis anticompetitive. The German Cartel Office also suggested that BSH should compensate brick-and-mortar sales through fixed payments, thereby largely ignoring the lack of incentive effects that fixed lump-sum payments have.From an economic perspective the great attention paid to intra-brand competition is misguided, as long as there is active inter-brand competition. Moreover, it is unclear why excluding the Internet as a distribution channel should be considered a hardcore restriction. Many cases concern status products such as watches, perfumes, cosmetics and similarly expensive products. In these instances, consumers may actually purchase the product because of its (expensive) brand image. If online sales destroy the expensive image of the product, this may obviously harm the manufacturer, but also many consumers themselves, who buy status products exactly because they are expensive. However, given the current approach in Europe, it appears to be extremely onerous to prove such a case.

Dual pricing schemes are nothing but a form of price differentiation, which is common in almost all wholesale markets that are less than perfectly competitive. Prohibiting dual pricing and disallowing bans on online sales makes it much more difficult for companies to incentivize brick-and-mortar retailers and presence by which manufacturers can generate value from window-shopping effects, additional services that can be provided offline and the easier provision of after-sales services by bricks-and-mortar stores. All these features would contribute to maintaining a brand’s value, thereby intensifying inter-brand competition.

Furthermore, preventing dual pricing can make manufacturers more reluctant to offer special discounts for offline sales in regions where a presence may be valued (e.g., in order to have a nationwide presence), but retailer profits are lower (e.g., due to lower demand), as a dual pricing ban in the presence of intense online competition basically prevents manufacturers from charging different wholesale prices to different retailers. Consequently, input price differentiation becomes much more difficult, even though the welfare effects are at best unclear (see Dertwinkel-Kalt et al., 2015, 2016). Hence, European competition agencies should revisit their overly strict approach to vertical restraints in the Internet and take a more lenient approach similar to the USA.

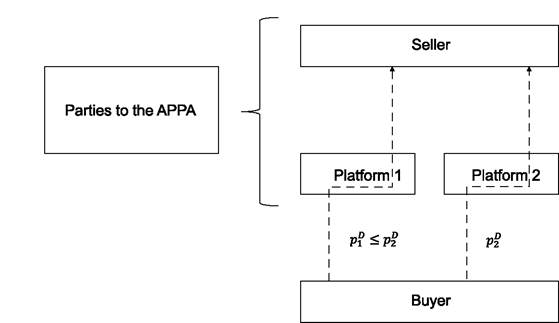

A final vertical restriction that has received much attention is across-platforms parity agreements (APPAs), illustrated in Figure 9.1. APPAs have most famously been used in the Apple e-book case and for travel and hotel booking platforms. With an APPA, a booking platform prohibits its content providers (e.g., e-book publishers or hotels) from offering their products at lower prices on any other platform. The standard theories of harm are either that this may lead to collusion among the content providers (e.g., publishers) or a foreclosure of the platform market, as no new platform can enter with lower prices. Other cases involve Amazon (in Germany and the UK) and motor insurance providers (in the UK).

Regarding the e-book case, when Apple entered the electronic books industry in 2010 it convinced book publishers (1) to adopt agency agreements under which final e-book prices are set by publishers, while retailers only receive a commission on every copy sold (in the case of Apple itself 30 percent), and (2) to adopt an APPA for their e-books that

Source: Buccirossi (2013, p. 22).

Figure 9.1 An across-platforms parity agreement (APPA)

allowed Apple to sell e-books at its competitors’ lowest price.

The agency agreements replaced the previous wholesale agreements that left the retail pricing decision with retailers. Around this time, the retail price of e-books sold by Amazon, the dominant retailer with a 90 percent market share in 2010, rose by about 18.6 percent on average, and the price of New York Times bestsellers rose by about 42.7 percent.11In April 2012, the US Department of Justice (DOJ) brought a case against Apple and a group of five major publishers for illegally conspiring to raise e-book prices, claiming that agency agreements played an instrumental role. The DOJ reached a settlement with the publishers and won the case against Apple. Both the court’s order and the settlement prohibited further use of agency agreements.

Similar proceedings against Apple and the five publishers were opened in the EU in December 2011. The European Commission had doubts concerning the companies’ joint switch from the wholesale model, where the e-book retail price is set by the retailer, to agency contracts that all contained the same key terms for retail prices - including an APPA, maximum retail price grids and the same 30 percent commission payable to Apple. The European Commission was particularly concerned ‘that the joint switch to the agency contracts may have been coordinated between the publishers and Apple, as part of a common strategy aimed at raising retail prices for e-books or preventing the introduction of lower retail prices for e-books on a global scale. This would violate Article 101 of the TFEU that prohibits cartels and restrictive business practices’ (European Commission, 2013). The Commission accepted commitments offered by Apple and four of the publishers in December 2012, while the fifth publisher settled on the same conditions in July 2013. The publishers and Apple offered commitments that contained the following three key provisions:

• Apple and the publishers terminate their then valid agency agreements.

• For a period of two years, the publishers cannot prevent e-book retailers from setting their own prices for e-books or, from offering discounts and promotions.

• For a period of five years neither the publishers nor Apple can set up agreements for e-books with retail-price APPAs (see European Commission, 2012).

In its defense Apple had claimed that its introduction of the iPad represented a major innovation that should be taken into account. Around the time Apple entered the e-book market it also introduced the iPad, thereby increasing competition in the market for e-book reading devices. In response, Amazon lowered the price of its reader, the Kindle, from $299 to $139 (and later even further) and also developed free software allowing its e-books to be read on the iPad and other devices.

In fact, the evidence on the e-book case is mixed. While De los Santos and Wildenbeest (2014) show that e-book prices increased following the APPA introduced by Apple, Gaudin and White (2014) also show that the e-book reader prices (the complementary asset) have fallen at the same time, making the overall effect less clear. Interestingly enough though, some European countries such as Germany are now about to introduce a legal resale price maintenance requirement for e-books.

With respect to hotel booking platforms and online travel agencies (OTAs), several European authorities have investigated the OTAs' APPA. Parallel investigations took place in several countries, including France, Germany, Italy, Sweden and the UK. In Germany, the Federal Cartel Office concluded that the APPA foreclosed the market and softened competition in the distinct market for searching, comparing and booking hotels online, as new entrant platforms would not be able to undercut existing platforms’ hotel rates. While the OTA platforms argued that an APPA was needed to safeguard their platforms’ investments, as hotels could otherwise free-ride on the platform’s investment by charging lower prices in own channels, the German Federal Cartel Office did not accept this argument and ruled that APPAs were anticompetitive and a violation of competition law.

In contrast, the joint investigation started under the coordination of the European Commission, in Italy, France and Sweden, concluded in April 2015 with a commitment by Booking.com to abstain from using a general APPA and use a so-called narrow APPA (or NAPPA) instead. Under a NAPPA, price parity clauses will only apply to prices and other conditions publicly offered by the hotels through their own online sales channels (such as their own website), in order to prevent the most obvious possibility for free-riding. However, hotels are free to set prices and conditions to other OTAs and to offline channels. This decision appears to be more balanced than the rather strict prohibition by the German Cartel Office, especially since the office’s theory of harm - namely that competition between platforms is not possible between OTAs in the presence of an APPA - must be called into question when it is noticed that the leading OTA, called Hotel Reservation Service (HRS), saw its market share reduced from more than 40 percent to almost exactly 30 percent over a period of two years. Even with APPAs, competition between platforms could occur through general rebates provided to users by the platform itself. In general, though, APPAs are an interesting new form of most-favored-customer clause, where more analysis is needed before robust results can be used.

9.5