CHAPTER C Brief Review of Dynamic Games

This chapter provides a very brief overview of some basic definitions, results and notation for infinite-horizon dynamic games. The reader is already assumed to be familiar with basic game theory, and the notions of Nash Equilibrium and Subgame Perfect Nash Equilibrium in finite games.

A review of these notions as well as much of the material covered here can be found in standard graduate game theory textbooks such as Fudenberg and Tirole (1994), Myerson (1991), Osborne and Rubinstein (1994) as well as Part 2 of Mascolell, Whinston and Green (1995). My focus is throughout on games of complete information (or the so-called games of perfect monitoring). These types of games were used in Section 14.4 in Chapter 14, as well as in Chapters 22 and 23. The material I present here is also included in Fudenberg and Tirole (1994).C. 1. Basic Definitions

I will consider the following class of dynamic infinite-horizon games. As the name suggests, these games are not finite and they are also somewhat more general than repeated games, since the stage game played at each date is a function of actions taken in the past.

More formally, there is a set of players denoted by N. This set will be either finite, or when it is infinite (especially uncountable), there will be more structure to make the game tractable and thus variants of the theorems here applicable. In particular, in many of the applications, especially in those considered in Chapters 22 and 23, there will be a continuum of players, but these will be in distinct finite groups and the game can be viewed as one between those distinct groups. With this motivation, in this Appendix I focus on the case in which N is finite, consisting of N players. Each player i ∈ N has a strategy set Ai (k) C Rni at every date, where k ∈ K C Rn is the state vector, with value at time t denoted by k (t).

A generic element of Ai (k) at time t is denoted by ai (t), and a (t) = (ai (t),...,a∏ (t)) denotes the vector of actions (or the “action profile”) at time t, i.e.,

I use the standard notation to denote the vector

to denote the vector

of actions without i’s action, thus we can also write Notice that,

Notice that,

consistent with the types of models analyzed in the text, the action set of each player Ai (k) is only a function of the state variable k and not of calendar time.

Each player has an instantaneous utility function ů (a (t),k (t)) where

is assumed to be continuous and bounded. This notation emphasizes that each player’s payoff depends on the entire action profile in that period (and not on past actions) and also on a common vector of state variables, denoted by k (t). Past actions will only have an effect on current payoffs through this vector of state variables.

As usual, each player’s objective at time t is to maximize their discounted payoff

S 0

S 0

where β ∈ (0,1) is the discount factor and Et is the expectations operator conditional on information available at time t. The games I focus on here have potential uncertainty about the evolution of the state variable in the future and also strategic uncertainty resulting because of mixed strategies. However, they will not feature asymmetric information, since I did not use incomplete information or asymmetric information dynamic games in this book. Consequently, the expectations operator Et is not indexed by i.

The law of motion of the state vector k (t) is given by the following Markovian transition function

which denotes the probability density that next period’s state vector is equal to k (t + 1) when the time t action profile of all the agents is a (t) ∈ A (k (t)) and the state vector is k (t) ∈ K.

I refer to this transition function Markovian, since it only depends on the current profile of actions and the current state. Naturally, the probability of all possible states tomorrow integrate to 1:

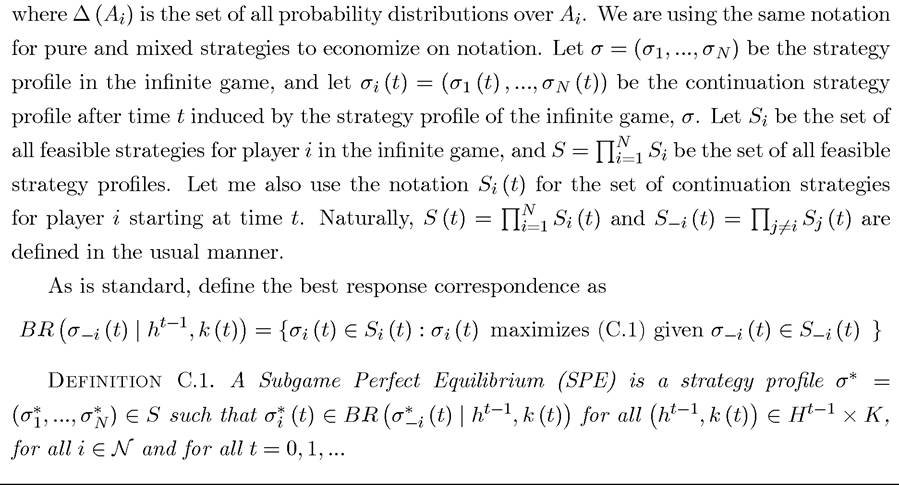

Next, we need to specify the information structure of the players. We focus on games with perfect observability or perfect monitoring, so that individuals observe realizations of all past actions (in case of mixed strategies, they observe realizations of actions not the strategies). Then, the public history at time t, observed by all agents up to time t, is therefore

the history of the game up to and including time t. With mixed strategies, the history would naturally only include the realizations of mixed strategies not the actual strategy. Let the 1180

set of all potential histories at time t be denoted by Ht. It should be clear that any element ht ∈ Ht for any t corresponds to a subgame of this game.[LVI]

Let a (pure) strategy for player i at time t be

i.e., a mapping that determines what to play given the entire past history ht-1 and the current value of the state variable k (t) ∈ K. This is the natural specification of a strategy for time t given that ht-1 and k (t) entirely determine which subgame we are in.

A mixed strategy for player i at time t is

Therefore, a SPE requires strategies to be best responses to each other given all possible histories, which is a minimal requirement.

What is “strong” (or “weak” depending on the perspective) about the SPE is that strategies are mappings from the entire history. As a result, in infinitely repeated games, there are many subgame perfect equilibria. This has prompted game theorists and economists to focus on a subset of equilibria. One possibility would be to look for “stationary” SPEs, motivated by the fact that the underlying game itself is stationary, i.e., payoffs do not depend on calendar time. Another possibility would be to look at the “best SPEs,” i.e., those that are on the Pareto frontier, and maximize the utility of one player subject to the utility of the remaining players not being below a certain level.Perhaps the most popular alternative concept often used in dynamic games is that of Markov Perfect Equilibrium (MPE). The MPE differs from the SPE in only conditioning on the payoff-relevant “state”. The motivation comes from dynamic programming where, as we have seen, an optimal plan is a mapping from the state vector to the control vector. MPE can be thought of as an extension of this reasoning to game-theoretic situations. The advantage of the MPE relative to the SPE is that most infinite games will have many fewer MPEs tha SPEs in general. The disadvantage, naturally, is that some economically interesting SPEs will be ignored when we focus on MPEs.

We could define payoff relevant history at time t in general as the smallest partition of Pt of Ht such that any two distinct elements of Pt necessarily lead to different payoffs or strategy sets for at least one of the players holding the action profile of all other players constant.

In this case, it is clear that given the Markovian transition function above, the payoff relevant state is simply k (t) ∈ K. Then we define a pure Markovian strategy as  and a mixed Markovian strategy as

and a mixed Markovian strategy as

Define the set of Markovian strategies for player i by and naturally,

and naturally,

Notice that I have dropped the t subscript here.

Given the way we have specified the game, time is not part of the payoff relevant state. This is a feature of the infinite-horizon nature of the game. With finite horizons, time would necessarily be part of the payoff-relevant state. Naturally, it is possible to imagine more general infinite-horizon games where the payoff function is Ui (ai (t),k (t),t), with calendar time being part of the payoff-relevant state.

Let us next define:

C. 2. Some Basic Results

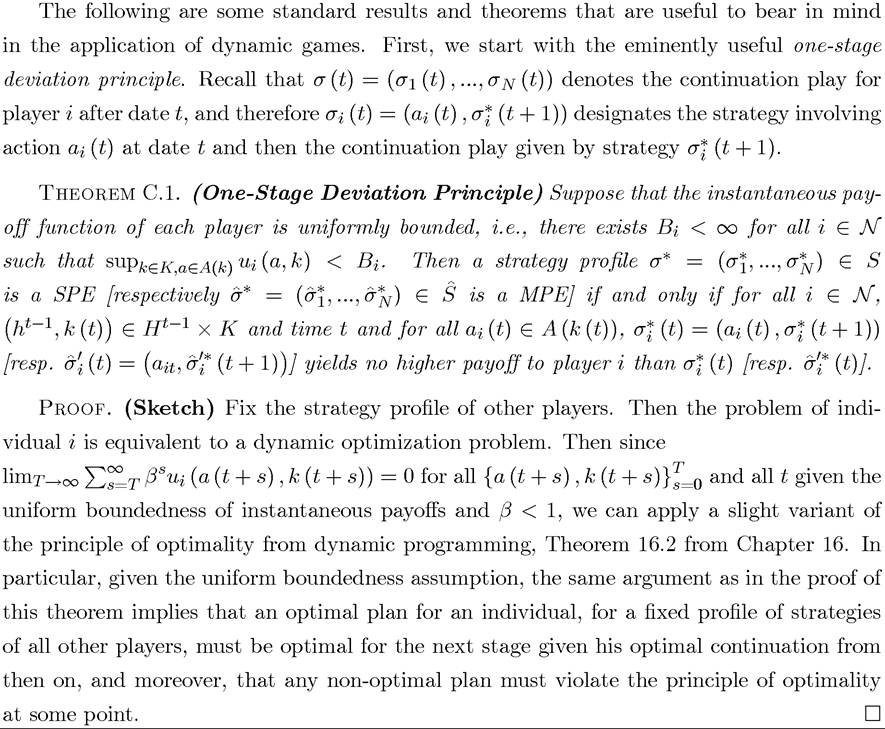

This theorem basically implies that in dynamic games, we can check whether a strategy is a best response to other players’ strategy profile by looking at one-stage deviations, keeping the rest of the strategy profile of the deviating player as given. The uniform boundedness assumption can be weakened to require “continuity at infinity”, which essentially means that discounted payoffs converge to zero along any history (and this assumption can also be relaxed further).

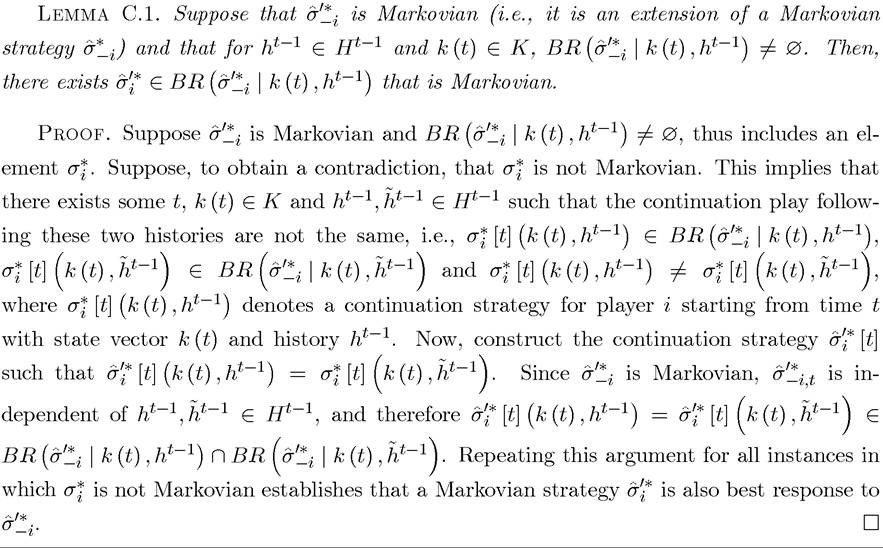

This lemma states that when all other players are playing Markovian strategies, there exists a best response that is Markovian for each player. This does not mean that there are no other best responses, but since there is a Markovian best response, this gives us hope in constructing Markov Perfect Equilibria. Consequently, we have the following theorem:

Existence of SPEs when K and Ai (k) are uncountable sets is much easier to guarantee.

For example, compactness and convexity of K and Ai (k) is sufficient for existence of pure strategy equilibria when Uit is quasi-concave in σ⅛ for all i ∈ N (in addition to the continuity assumptions above). In the absence of convexity of K and Ai (k) or quasi-concavity of Ui (t), mixed strategy equilibria can always be guaranteed to exist under some very mild additional

This theorem implies that every MPE strategy profile corresponds to a SPE strategy profile and any equilibrium-path play supported by a MPE can be supported by a SPE.

a-i (σ*-i) | k (t),ht~1} + βEUf [t + 1] (k (t + 1),ht | ⅛)1,

i in all subgames, and in response, the best that player i can do is to play an equilibrium strategy.

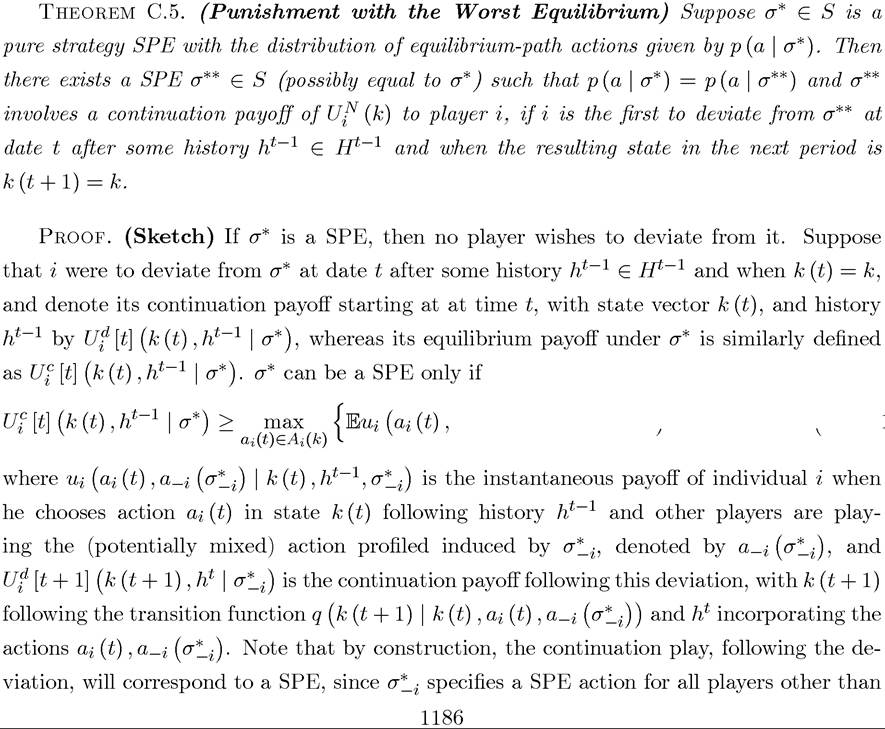

By definition of a SPE and the minimum equilibrium payoff of player i defined in (C.3), we have

This theorem therefore states that when looking for the set of SPEs, we can limit attention to those involving the most severe equilibrium punishments.

A stronger version of this theorem is the following:

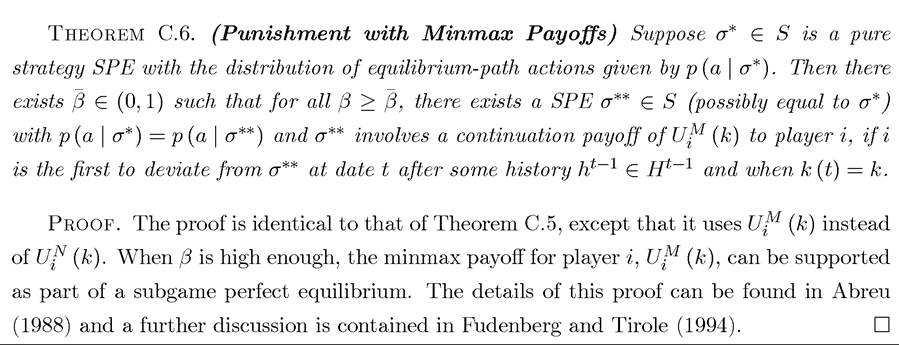

C. 3. Application: Repeated Games With Perfect Observability

For repeated games with perfect observability, both SPE and MPE are easy to characterize and their properties are well-known. In particular, suppose that we have the same stage game played an infinite number of times, so that payoffs are given by

which is only different from (8.3) because there is no conditioning on the state variable k (t). Let us refer to the game {ui (a),a ∈ A } as the stage game. Define

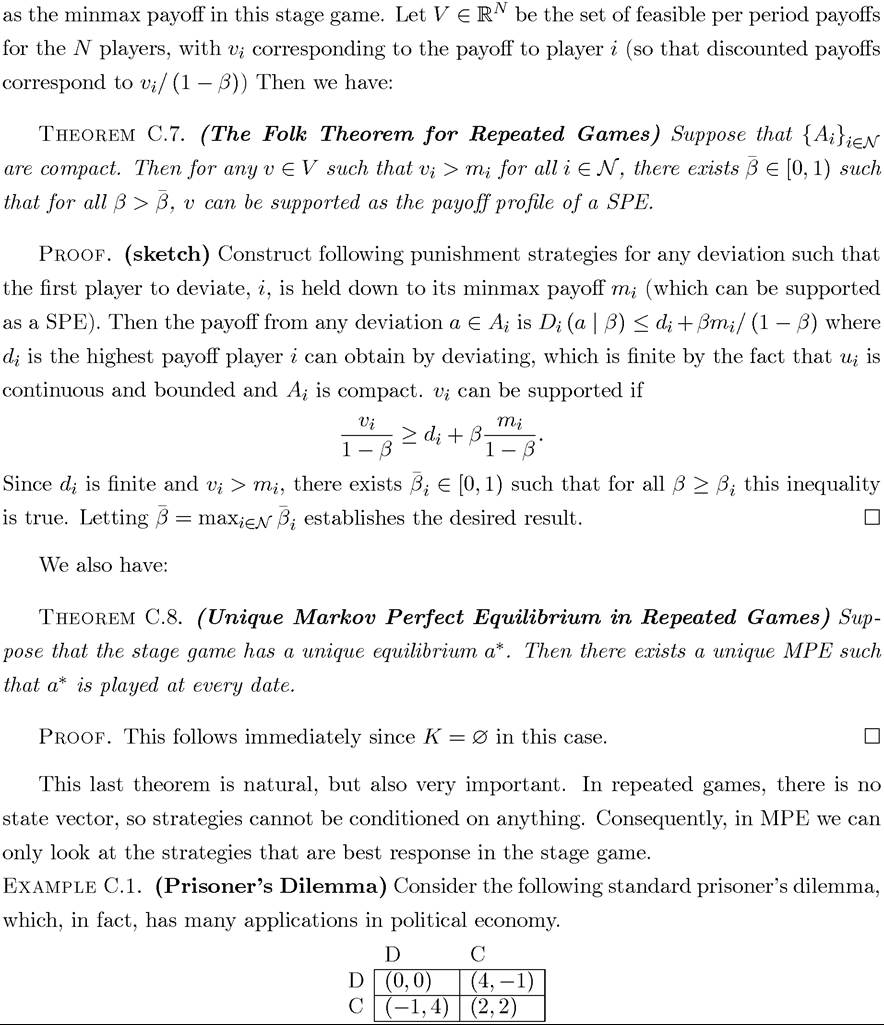

The stage game has a unique equilibrium, which is (D,D). Now imagine this game being repeated an infinite number of times with both agents having discount factor β. The unique MPE is playing (D,D) at every date.

In contrast, when β > 1/2, then (C,C) at every date can be supported as a SPE. To see this, recall that we only need to consider the minmax punishment, which in this case is (0, 0). Playing (C,C) leads to a payoff of 2/ (1 — β), whereas the best deviation leads to the payoff of 4 now and a continuation payoff of 0. Therefore, β > 1/2 is sufficient to make sure 1188

that the following grim strategy profile implements (C,C) at every date: for both players, the strategy is to play C if ht includes only (C,C) and play D otherwise.

Why this strategy combination is not a MPE is also straightforward to see. The grim strategy ensures cooperation by conditioning on past history, i.e., it conditions on whether somebody has defected at any point in the past. This history is not payoff relevant for the future of the game given the action profile of the other player—fixing the action profile of the other player, whether somebody has cheated in the past or not has no effect on future payoffs.

C. 4. Exercises

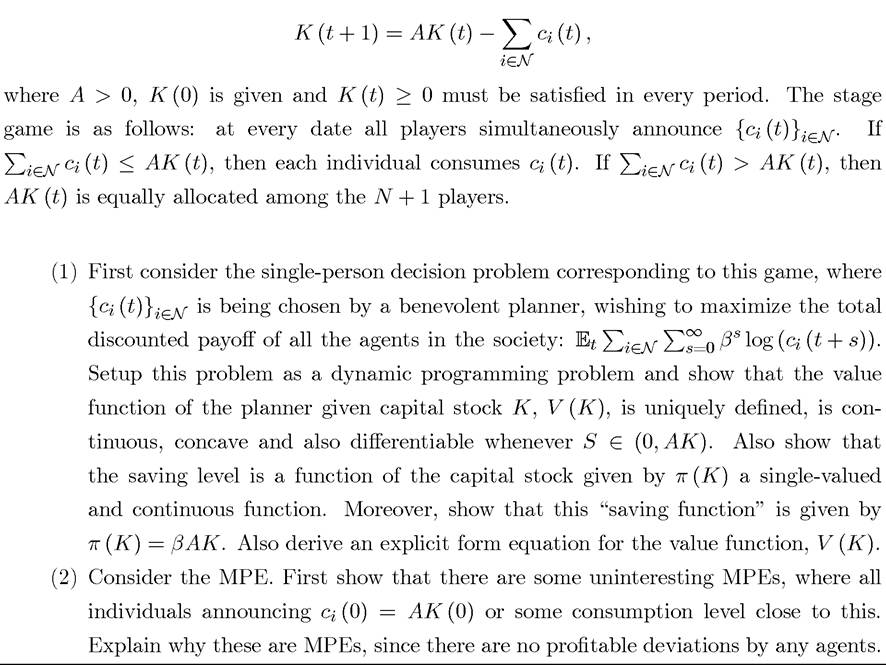

EXERCISE C.1. A simple application of the ideas in this appendix are common pool games. Consider a society consisting of N + 1 < ∞ players each with payoff function

at time t where β ∈ (0,1) and Ci (t) denotes consumption of individual i ∈ N at time t. The society has a common resource, denoted by K (t), which can be thought of as the capital stock at time t. This capital stock follows the non-stochastic law of motion:

Explain this expression and provide an intuition.

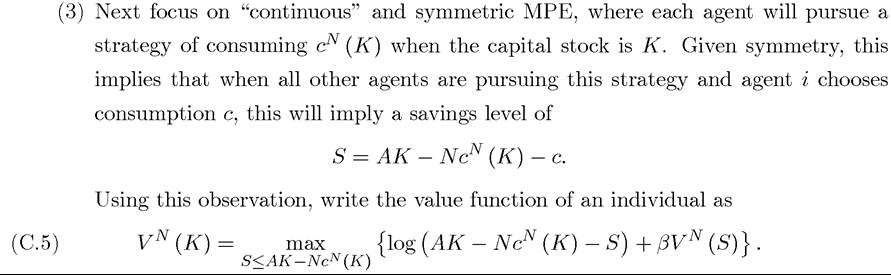

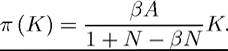

(4) Assuming differentiability, derive the first-order condition of the maximization problem in (C.5) and show that there exists a symmetric equilibrium where the equilibrium aggregate saving level in the economy will be given by

Compare this expression to that in Part 2. What is the effect of an increase in N? Provide in intuition for this.

(5) Show that if βA > 1 > βA∕ (1 + N - βN), than the single-person decision problem would involve growth over time, while the MPE would involve the resources shrinking over time.

(6) Next show that in this game there always exists subgame perfect equilibria that implements the single-person solution for any value of β > 0. Explain this result.

(7) Now suppose that βA = 1 and again focus on MPE. Suppose that the game starts with capital stock K (0) and consider following discontinuous Markovian strategy profile:

Show that when all players other than i' pursue this strategy, it is a best response for player i' to play this strategy as well, and along the equilibrium path, the singleperson solution is implemented. Carefully provide an intuition for this result. Show that the same result cannot be obtained when Why not?

Why not?