Dynamic Effects of Distortionary Taxation

Until now we have assumed that taxation takes the form of lump sum taxes that do not distort factor prices and relative prices faced by households and business firms. However, lump sum taxes, are a very rare breed.

Most forms of taxation, such as income and consumption taxes, are levied in ways that distort the incentives of households and firms to work, save, and invest. In this section, we investigate the dynamic effects of such distortionary taxes in the representative household model of economic growth.6.4.1 Distortionary and Nondistortionary Taxes

To keep things simple, assume that the government runs a continuously balanced budget and has no government debt. The government engages in primary government expenditure and transfers to households, and it levies taxes on income from capital and labor, business profits before interest and depreciation, and on the consumption of households. Thus, at every instant, the government budget constraint per efficiency unit of labor is given by

where cg is primary government expenditure, v is real transfers to households and firms, τw is the tax rate on labor income, τk is the tax rate on capital income, τc is the tax rate on consumption, and τf is the tax rate on firms’ profits before interest and depreciation. All variables, apart from tax rates and the real interest rate r, are defined per efficiency unit of labor.

The existence of income and consumption tax rates and government transfers affects the intertemporal budget constraints of both households and firms (and thus their optimal savings and investment decisions). The first-order condition for the maximization of profits by firms now takes the form

Firms now equate the post-tax marginal product of capital with the pre-tax user cost of capital r + δ, because taxes are levied on profits before interest and depreciation.

The Euler equation for consumption of the representative household now takes the form

Because income from capital is taxed, it is the net-of-tax real interest rate that drives savings decisions.

From (6.23) and (6.24), it follows that

The accumulation equation for capital is not affected by the existence of distortionary taxes, because the government budget constraint (6.22) shows that the revenue from distortionary taxes minus transfers is equal to primary government expenditure. Thus, the accumulation of capital (per efficiency unit of labor) is determined by the usual accumulation equation of the form

The behavior of the economy is determined by (6.25) and (6.26). The only distortionary taxes that enter these two equations are the tax rate τk on interest income and the tax rate τf on the profits of firms before interest and depreciation.

The tax rate τw on labor income does not affect the behavior of the economy. The reason is that we have assumed that labor supply is inelastic: Every household member supplies one unit of labor, irrespective of the real wage. If labor supply were elastic, then taxes on labor income would imply distortions and have real effects.

In addition, the consumption tax τc does not enter the Euler equation for consumption, as we have assumed that this tax rate is constant and does not affect the intertemporal substitution of consumption (savings). And because labor supply is also assumed to be exogenous, the tax rate on consumption does not affect labor market incentives, as there is no substitution between consumption and leisure.

Thus in the Ramsey model with inelastic labor supply, as we have assumed throughout, the only distortionary taxes are those on income from capital and those on profits of business firms before interest and depreciation.

All other taxes are nondistortionary.6.4.2 Dynamic Effects of Capital Income and Business Gross Profits Taxation

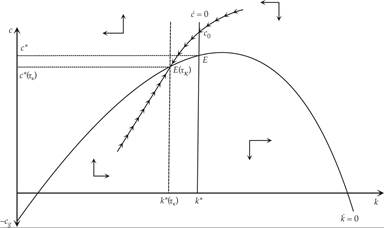

The dynamic effects of capital income taxes are analyzed in figure 6.8. Assume that initially, the taxation of income from capital is zero and the economy is at the balanced growth path E. The government announces a previously unanticipated capital income tax at a rate τk. The proceeds are returned to households in the form of transfer payments.

Figure 6.8 Short- and long-run effects of capital income taxation in the Ramsey model.

The steady state consumption line moves to the left, because on the new balanced growth path, the pre-tax real interest rate must rise, something that requires a lower steady state capital stock per efficiency unit of labor. As the capital stock is a predetermined variable, the pre-tax real interest rate is also a predetermined variable. The introduction of the tax thus causes a reduction in post-tax real interest rates for households. Consumption rises to c0, and savings fall immediately. The economy enters into a process of capital decumulation, rising real interest rates, and falling consumption. In the new balanced growth path at E(τk), the capital stock per efficiency unit of labor is lower, and so is total output and private consumption.

A similar process will take place if there is an increase in the tax rate on business profits before interest and depreciation (gross profits). This will initially cause a fall in the real interest paid out to households, a temporary increase in private consumption, a process of decumulation of capital, and adjustment to a new balanced growth path. This new path will have a lower capital stock, lower output and income, lower real wages, and lower consumption per efficiency unit of labor.

The dynamic effects of distortionary taxation would be qualitatively similar in OLG models, such as the model of Blanchard and Weil.

Exercise 6.2 Introduce distortionary taxes in the Blanchard-Weil OLG model, and analyze the impact of a proportional income tax levied on the labor and capital income of households. The tax proceeds are returned to households without affecting the distribution of income. Assume that initially, the taxation of income from capital is zero and the economy is on the balanced growth path. The government announces a previously unanticipated income tax at a rate τ. Primary government expenditure and debt remain at their previous path.

6.4.3 Dynamic Simulations of Increases in Capital Income and Business Gross Profits Taxation

To quantitatively examine the dynamic effects of an increase in capital income taxation in the Ramsey model, we can simulate, for the specific values of the parameters of the model assumed so far, the transition from a balanced growth path without capital income taxation to a balanced growth path after the introduction of capital income taxation.

The parameter values used in the simulations are the same as those used in the simulations of the Ramsey model in chapter 4. Thus, we assume a Cobb-Douglas production function, and the parameters take the values A = 1, α = 0.333, ρ = 0.02, θ = 1, n = 0.01, g = 0.02, δ = 0.03.

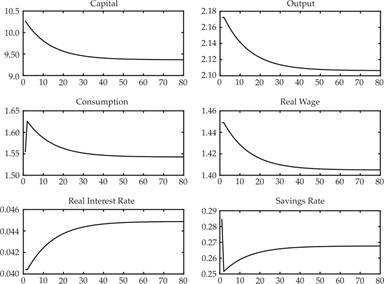

In the simulation depicted in figure 6.9, the economy is on its original balanced growth path, without capital income taxation. In period 1, the government imposes a previously unanticipated 10% tax on interest income (increase of τk). This increase, as predicted theoretically in the analysis of figure 6.8, leads to a decrease in the net real interest rate enjoyed by households. This decreased rate causes an increase in consumption and a fall in the savings rate, which initiate a process of capital decumulation, a gradual decline in real output and real wages, and a gradual increase in the pre-tax real interest rate.

Figure 6.9 Dynamic effects of a 10% tax on interest income in the calibrated Ramsey model.

The reduction in real wages and the increase in the pre-tax real interest rate are a result of the declining capital stock, which causes a falling marginal product of labor and a rising marginal product of capital. The economy gradually converges to a new balanced growth path. On this path, capital per efficiency unit of labor is lower by approximately 8.9% compared to the original balanced growth path, output and real wages are lower by 3.0%, consumption is lower by 0.7% (due to the decline in the savings rate), and the (pre-tax) real interest rate has increased by 0.44 percentage points (or approximately 10%). The steady state savings rate, which is endogenous in this model, falls from 28.5% to 26.8%.

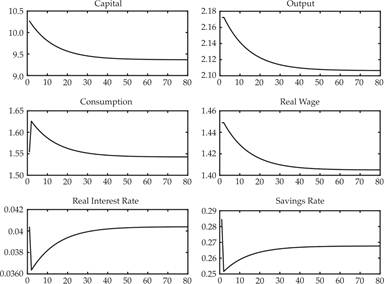

The dynamic real effects of a 10% tax on on business profits before interest and depreciation are exactly the same. The only real variable that behaves differently is the pre-tax real interest rate, which initially falls and then gradually returns to its original steady state value through the decumulation of capital. The results of this simulation are presented in figure 6.10.

Figure 6.10 Dynamic effects of a 10% tax on business profits, before interest and depreciation, in the calibrated Ramsey model.

As one can deduce from these simulations, even a relatively low rate of capital income taxation or taxation of business net income (before interest and depreciation) causes relatively large declines in per capita output and income, as it leads to a significant reduction of savings and capital accumulation.

6.5