Effects of the Growth Rate of the Money Supply in the Ramsey Monetary Model

The evolution of real variables in the Ramsey model with money is determined by the Euler equation for consumption (7.18) and the capital accumulation equation (7.28). These two determine the paths of private consumption and the capital stock.

All other real variables are functions of the capital stock (per efficiency unit of labor) or private consumption. Output is determined by the production function (7.19). The real interest rate and real wage are determined by the marginal productivity conditions, which are only a function of capital per effective unit of labor k. The demand for real money balances is determined by the money demand function (7.11), the nominal interest rate is determined by the Fisher equation (7.5), and inflation is determined by equation (7.14).

As for the government, let us make similar assumptions to the ones made in chapter 6. Assume that the government chooses a constant level of primary expenditure  and government debt

and government debt  per efficiency unit of labor, and it uses taxes to satisfy the government budget constraint. The government also chooses, through the central bank, a constant rate of growth μ for the money supply. All seigniorage revenue accrues to the government budget.

per efficiency unit of labor, and it uses taxes to satisfy the government budget constraint. The government also chooses, through the central bank, a constant rate of growth μ for the money supply. All seigniorage revenue accrues to the government budget.

Under these assumptions, private consumption and the accumulation of capital are determined by the pair of differential equations

As one can see from (7.29) and (7.30), neither the stock of money nor the growth rate of the money supply affects the evolution of private consumption (savings) or the accumulation of capital (investment). The determination of consumption and the capital stock is the same as in a model without money.

The only government policy variable that appears to affect the economy is real primary government expenditure.The model is the same as the Ramsey model without money in chapter 6. The growth rate of the money supply affects inflation, nominal interest rates, and the demand for money, but no other real variables (such as output, consumption, the capital stock, real wages, and real interest rates). This can be seen by examining the balanced growth path.

7.3.1 The Balanced Growth Path in the Ramsey Model with Money

As in the Ramsey model without money, it is straightforward to prove that the economy possesses a unique balanced growth path and a unique saddle path leading to the balanced growth path.

On the balanced growth path, all variables that have been defined per efficiency unit of labor remain constant, and the same applies to interest rates (real and nominal) and inflation.

From (7.29), on the balanced growth path, the real interest rate must be equal to the pure rate of time preference plus the exogenous rate of technical progress multiplied by the inverse of the intertemporal elasticity of substitution. Therefore, steady state capital per efficiency unit of labor is determined by the condition

Steady state consumption per efficiency unit of labor is determined by the steady state version of (7.30) to be

Primary government expenditure has a one-to-one negative effect on private consumption and does not affect the steady state capital stock or steady state output.

Real output per efficiency unit of labor on the steady state is determined by the production function (7.19):

The steady state real interest rate and the real wage per efficiency unit of labor are determined by the marginal productivity conditions:

Equations (7.31)–(7.35) determine the evolution of all real variables on the balanced growth path, with the exception of real money balances.

Capital, output, the real wage, and consumption per efficiency unit of labor are constant on the balanced growth path, as is the real interest rate. All per capita variables grow at the exogenous rate of technical progress g.In this model, the method of financing government expenditure, the money stock, and the growth rate of the money supply do not affect the balanced growth path. Thus, Ricardian equivalence, the neutrality of money, and the superneutrality of money hold in a representative household model.

7.3.2 The Superneutrality of Money and Inflation

The superneutrality of money was first analyzed by Sidrauski [1967], who demonstrated that in a representative household model, the growth rate of the money supply does not affect real variables on the balanced growth path.

On the balanced growth path, the inflation rate is determined by the difference between the growth rate of the money supply from the long-term growth rate n + g. This can be seen from the inflation determination equation (7.14). Assuming a constant growth rate of the money supply, the inflation rate on the balanced growth path equals

where n + g is the steady state growth rate of total private consumption (and output).

Moving from (7.14) to (7.36) we have assumed that the nominal interest rate is constant on the balanced growth path. From the Fisher equation (7.5), the steady state nominal interest rate is indeed constant and equal to

Finally, real money balances per efficiency unit of labor are also constant on the balanced growth path. They are determined from the money demand equation (7.11) and are given by

Note that the elasticity of money demand with respect to the nominal interest rate is equal to the elasticity of intertemporal substitution 1/θ.

The higher the growth rate of the money supply is, given the other structural parameters of the model, the higher the inflation rate and the nominal interest rate and the lower the stock of real money balances on the balanced growth path will be.

A permanent increase in the growth rate of the money supply by 5 percentage points causes an increase in inflation and in nominal interest rates by 5 percentage points as well. It also causes a decrease in the demand for real money balances. In a representative household model, real money balance is the only real variable affected by the growth rate of the money supply on the balanced growth path. As mentioned at the start of this chapter, this has been termed the superneutrality of money.

It also follows that the neutrality of money holds in this model, as the level of the money supply only affects the price level and not real variables. From the definition of real money balances per efficiency unit of labor, we have

where h0 and L0 are the efficiency of labor and the labor force at time 0, respectively. Real money balances are also growing at a rate g + n on the balanced growth path. From (7.39), the only effect of a rise in the money stock is an equiproportionate rise in the price level. Thus, the neutrality of money also holds in this model.

Exercise 6.2 Derive the steady state for all real and nominal variables using the model consisting of equations (7.11), (7.18)–(7.21), and (7.28). Assume a Cobb-Douglas production function, a unitary intertemporal elasticity of substitution of consumption, constant government expenditure and government debt per efficiency unit of labor, and a constant growth rate of the money supply. Discuss how the various exogenous parameters of the model affect real and nominal steady state variables. By linearizing the model around the steady state, analyze and discuss the properties of the adjustment path.

7.3.3 The Welfare Costs of Inflation in a Ramsey Model

Does the superneutrality of money mean that inflation does not matter in a representative household model? Far from it. Inflation implies a distortion in that the demand for real money balances, and therefore, the liquidity services of money decrease as the rate of inflation and nominal interest rates increase. Hence, the welfare of the representative household goes down with the rate of inflation, as the representative household economizes on real money balances and enjoys lower liquidity services.

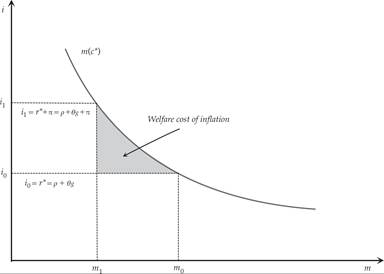

The analysis of the welfare costs of inflation can be simplified by using the steady state money demand function (7.38). This is depicted graphically in figure 7.1 for a given steady state consumption per efficiency unit of labor.

Figure 7.1 The demand for real money balances and the welfare cost of inflation.

The figure compares two equilibria. At one of them, inflation is zero, and the nominal interest rate is equal to the real steady interest rate ρ + θg. At the other, the positive inflation rate is π. The welfare cost of inflation is measured by the area of the gray triangle in figure 7.1, which is the loss of consumer surplus that does not translate into a higher inflation tax. This is the net welfare cost of inflation, which measures the reduction in the welfare of the representatitve household that does not translate into higher government revenue from inflation. One can easily show that the higher the inflation rate is, the higher the welfare cost of inflation will be.

Hence, inflation matters in the representative household model: It causes a reduction in the demand for real money balances and thus lower liquidity services from money. To the extent that the liquidity services of money yield utility, this reduction implies a welfare cost.4

7.4