Financial Frictions in a Model with Unemployment Persistence and Nominal Wage Contracts

In this section, we introduce financial frictions in the form of an exogenous external finance premium in the model of nominal wage contracts of chapter 17. Assume that prices are fully flexible, but nominal wage contracts are predetermined.

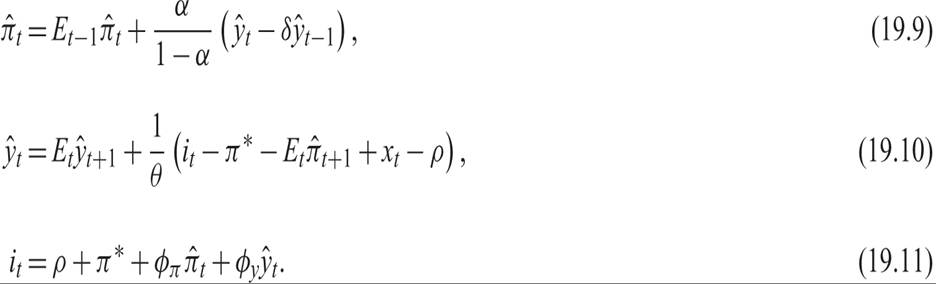

We explore the rational expectations solution of the model and analyze the macroeconomic effects of financial frictions. We will see that only unanticipated shocks to the external finance premium affect aggregate fluctuations in this model. The reason is that anticipated shocks cause wage setters to adjust wages in advance, to counteract the effects of financial shocks on output and employment. Yet deviations of output and unemployment from their natural rates persist, as the degree of persistence depends on the dynamics of the group of insiders.The model is that presented in chapter 17, simplified so that there is no staggering of prices. It is described by

Equation (19.9) is the expectations-augmented Phillips curve in the presence of one-period nonindexed wage contracts set by labor market insiders; (19.10) is the new neoclassical synthesis IS curve, determining the demand for output; and (19.11) is the Taylor rule for the determination of the central bank interest rate. In these equations,  denotes deviations of current inflation from the central bank target π*, and ŷt denotes deviations of output from its natural rate.

denotes deviations of current inflation from the central bank target π*, and ŷt denotes deviations of output from its natural rate.

We have simplified the model by abstracting from productivity shocks and shocks to the interest rate rule of the central bank, to concentrate on shocks to the external finance premium xt. In the model, ρ is the pure rate of time preference, which, in the absence or productivity shocks, is assumed to be equal to the natural real rate of interest, and 1/θ is the intertemporal elasticity of substitution of consumption.

The other parameters are as defined in chapter 17. The process determining xt is given by equation (19.4). Thus, the external finance premium is assumed to follow a zero-mean stationary AR(1) process, as in section 19.1.The rational expectations solution of the model is straightforward and can be derived in the same way as for the solution in chapter 17. Deviations of inflation from the central bank target and deviations of output from its natural rate are given by

where

In this model, and in the absence of staggered pricing, it is only unanticipated financial shocks that cause negative deviations of inflation from the central bank target and of output from its natural rate. However, the effects of such shocks persist, as they are propagated by the degree of employment persistence δ, which also determines the persistence of output and unemployment from their natural rates.

Obviously, unemployment is also affected by financial shocks in this model. Using the Okun-type relation (17.41), linking deviations of output from its natural rate to deviations of unemployment from its own natural rate, we get the following relation linking financial shocks to fluctuations in the unemployment rate:

Thus, financial shocks, such as shocks to the external finance premium, cause unemployment to rise relative to its natural rate. The rise in unemployment persists because of the degree of persistence in the labor market. The reduction of nominal interest rates through the Taylor rule is not a sufficient response to a financial crisis, as the optimal response would require an infinitely large response of interest rates to deviations of inflation from target, or deviations of output from its natural rate.

For example, as ϕπ tends to infinity, ψ tends to zero, and the shock to the external finance premium is completely neutralized—it does not affect either inflation or output. Thus, as in the case of the model with staggered pricing, the optimal monetary policy response to financial shocks is the Fisher [1919] response of completely stabilizing inflation at the target inflation rate π*. However, this policy requires an infinitely elastic response of interest rates and may not always be feasible, especially in the presence of a zero lower bound on interest rates.Exercise 19.3 In the model consisting of equations (19.9)–(19.11), replace the exogenous process of the external finance premium by the following process:

where 0 < χ < 1, and  is a white noise process. Derive the rational expectations solution of the resulting model. Derive the response of the unemployment rate to financial shocks, assuming the Okun relation (17.41). How would you explain the feedback loop between deviations of output from its natural rate and the external finance premium? Discuss your findings.

is a white noise process. Derive the rational expectations solution of the resulting model. Derive the response of the unemployment rate to financial shocks, assuming the Okun relation (17.41). How would you explain the feedback loop between deviations of output from its natural rate and the external finance premium? Discuss your findings.

19.4