Financial Frictions in a New Keynesian Model with Staggered Pricing

In this section, we investigate the macroeconomic effects of a financial shock in the context of the new Keynesian model with staggered pricing. We introduce a financial shock, which, in the presence of financial frictions, results in a rise in the external finance premium.

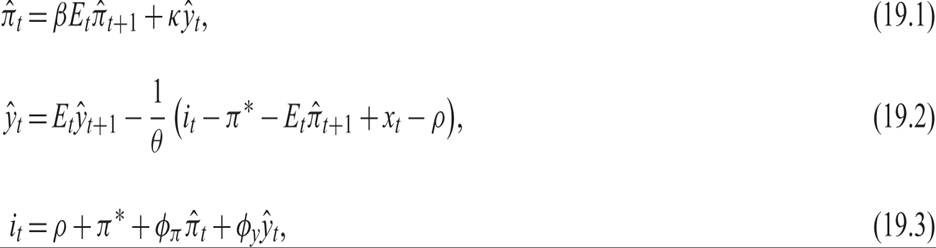

It is assumed that the real interest rate faced by private sector agents, such as households, is the safe real interest augmented by an external finance premium x.The model consists of the new Keynesian Phillips and IS curves and a Taylor rule. It is the same as the model in chapter 16, although the interest rate relevant for private sector borrowing is no longer equal to the central bank real interest rate: Because of financial frictions, it equals the central bank interest rate augmented by an external finance premium x. For analytical simplicity, let us abstract from productivity shocks and monetary policy shocks, because their effects were analyzed in chapter 16.

The model can be written as

where  = π − π* and

= π − π* and  denote the deviations between current and target (steady state) inflation and between the current (log) real output and its natural rate, respectively; and xt is the external finance premium relevant for private borrowing. Thus, the real interest rate on the new Keynesian IS curve (19.2) is the central bank real interest rate, augmented by the external finance premium.

denote the deviations between current and target (steady state) inflation and between the current (log) real output and its natural rate, respectively; and xt is the external finance premium relevant for private borrowing. Thus, the real interest rate on the new Keynesian IS curve (19.2) is the central bank real interest rate, augmented by the external finance premium.

The external finance premium is assumed exogenous and temporary, following an AR(1) process of the form

where 0 < ηx < 1 is the degree of persistence of the external finance premium, and  is a white noise shock to the external finance premium.5

is a white noise shock to the external finance premium.5

Solving the model under rational expectations in the same manner as in chapter 16, we get that the closed-form solutions for deviations of inflation from its steady state level and deviations of output from its natural rate are given by

where

The deflation and the recession occur despite the fact that, through the Taylor rule, the central bank reduces nominal interest rates. Substituting (19.5) and (19.6) in the Taylor rule (19.3), one can see that the nominal interest rate also reacts negatively to shocks in the external finance premium.

However, this reaction is not in general sufficient to neutralize this financial shock:

Thus, a financial crisis that raises the external finance premium will cause a fall in inflation and a recession, despite the reduction of nominal interest rates through the Taylor rule.

The typical Taylor rule is clearly suboptimal in the case where a recession is due to financial frictions. The optimal response would have required an infinitely large response of interest rates to deviations of inflation from target, or deviations of output from its natural rate. For example, as ϕπ tends to infinity, Λx tends to zero, and the shock to the external finance premium is completely neutralized, as it does not affect either inflation or output. Thus, in the case of financial frictions, the optimal monetary policy response is the Fisher [1919] response of completely stabilizing inflation at the target inflation rate π*.6

It is also straightforward to prove that higher persistence in the shock to the external finance premium implies both a higher and more persistent deflation and recession under the Taylor rule.

Finally, the real effects of a financial crisis would not occur in a model without nominal rigidities, as for example, the new classical model of chapter 14.7

Exercise 19.1 Derive the rational expectations solution of the model consisting of equations (19.1)–(19.4), and prove the results discussed in the text.

Exercise 19.2 In the model consisting of equations (19.1)–(19.4), replace the exogenous process of the external finance premium by the following process:

where 0 < χ < 1, and  is a white noise process. Derive the rational expectations solution of the resulting model. How would you interpret the feedback loop between deviations of output from its natural rate and the external finance premium? Discuss your findings.

is a white noise process. Derive the rational expectations solution of the resulting model. How would you interpret the feedback loop between deviations of output from its natural rate and the external finance premium? Discuss your findings.

19.3