Fiscal Policy and the Current Account

Analyze the relationship between the government budget deficit and the current account deficit.

During the 1980s and 1990s the United States often had both large government budget deficits and large current account deficits.

Are these two phenomena related? Many economists and other commentators argue that they are, suggesting that in fact the budget deficit is the primary cause of the current account deficit. Those supporting this view often use the phrase "twin deficits" to convey the idea that the government budget deficit and the current account deficit are closely linked. Not all economists agree with this interpretation, however; some argue that the two deficits are largely unrelated. In this section we briefly discuss what the theory has to say about this issue and then turn to the evidence.The Critical Factor: The Response of National Saving

In theory, the issue of whether a link exists between the government budget deficit and the current account deficit revolves around the following proposition: An increase in the government budget deficit will raise the current account deficit only if the increase in the budget deficit reduces desired national saving.

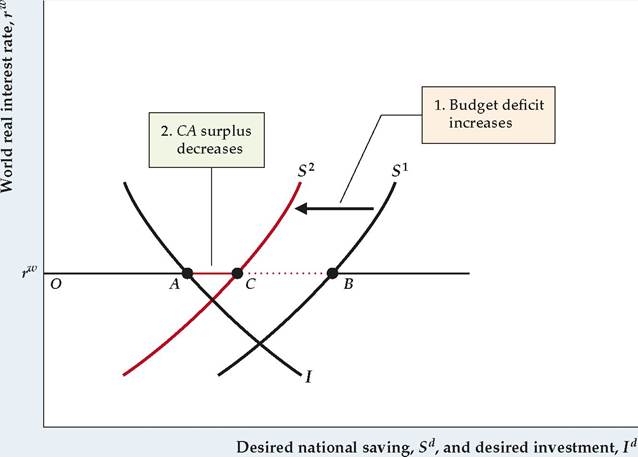

Let's first look at why the link to national saving is crucial. Figure 5.8 shows the case of the small open economy. The world real interest rate is fixed at rw. We draw the initial saving and investment curves, S1 and I, so that, at the world real interest rate, rw, the country is running a current account surplus, represented by distance AB. Now suppose that the government budget deficit rises. For simplicity, we assume throughout this section that the change in fiscal policy doesn't affect the tax treatment of investment so that the investment curve doesn't shift. Hence as Fig. 5.8 shows, the government deficit increase will change the current account balance only if it affects desired national saving.

The usual claim made by supporters of the twin-deficits idea is that an increase in the government budget deficit reduces desired national saving. If it does, the increase in the government deficit shifts the desired national saving curve to the left, from S1 to S2. The country still has a current account surplus, now equal to distance AC, but it is less than the original surplus, AB.

We conclude that in a small open economy an increase in the government budget deficit reduces the current account balance by the same amount that it reduces desired national saving. By reducing saving, the increased budget deficit reduces the amount that domestic residents want to lend abroad at the world real interest rate, thus lowering financial outflows. Equivalently, reduced national

FIGURE 5.8

The government budget deficit and the current account in a small open economy An increase in the government budget deficit affects the current account only if the increased budget deficit reduces national saving. Initially, the saving curve is S1 and the current account surplus is distance AB. If an increase in the government deficit reduces national saving, the saving curve shifts to the left, from S1 to S2. With no change in the effective tax rate on capital, the investment curve, I, doesn't move. Thus the increase in the budget deficit causes the current account surplus to decrease from distance AB to distance AC. In contrast, if the increase in the budget deficit has no effect on national saving, the current account also is unaffected and remains equal to distance AB.

saving means that a greater part of domestic output is absorbed at home; with less output to send abroad, the country's current account balance falls. Similar results hold for the large open economy (you are asked to work out this case in Analytical Problem 4 at the end of the chapter).

The Government Budget Deficit and National Saving

Let's now turn to the link between the budget deficit and saving and consider two cases: a budget deficit arising from an increase in government purchases and a deficit originating from a cut in taxes.

A Deficit Caused by Increased Government Purchases. Suppose that the source of the government budget deficit is a temporary increase in government purchases, perhaps owing to a military buildup. In this case there is no controversy: Recall (Chapter 4) that with output, Y, held constant at its full-employment level, an increase in government purchases, G, directly reduces desired national saving, Sd = Y — Cd — G.[85],[86] Because economists agree that a deficit owing to increased government purchases reduces desired national saving, they also agree that a deficit resulting from increased government purchases reduces the nation's current account balance.

A Deficit Resulting from a Tax Cut. Suppose instead that the government budget deficit is the result of a cut in current taxes, with current and planned future

government purchases unchanged. With government purchases, G, unchanged and with output, Y, held constant at its full-employment level, the tax cut will cause desired national saving, Sd = Y — Cd — G, to fall only if it causes desired consumption, Cd, to rise.

Will a tax cut cause people to consume more? As we discussed in Chapter 4, believers in the Ricardian equivalence proposition argue that a lump-sum tax change (with current and future government purchases held constant) won't affect desired consumption or desired national saving. These economists point out that a cut in taxes today forces the government to borrow more to pay for its current purchases; when this extra borrowing plus interest is repaid in the future, future taxes will have to rise. Thus, although a tax cut raises consumers' current after-tax incomes, the tax cut creates the need for higher future taxes and lowers the after-tax incomes that consumers can expect to receive in the future.

Overall, according to this argument, a tax cut doesn't benefit consumers and thus won't increase their desired consumption.If the Ricardian equivalence proposition is true, a budget deficit resulting from a tax cut will have no effect on the current account because it doesn't affect desired national saving. However, as we noted in Chapter 4, many economists argue that— despite the logic of Ricardian equivalence—in practice many consumers do respond to a current tax cut by consuming more. For example, consumers simply may not understand that a higher deficit today makes higher taxes tomorrow more likely. Or some consumers may face binding borrowing constraints, so that a current tax cut allows them to spend more today, which they find desirable. If for any reason consumers do respond to a tax cut by consuming more, the deficit resulting from a tax cut will reduce national saving and thus also will reduce the current account balance.

Application

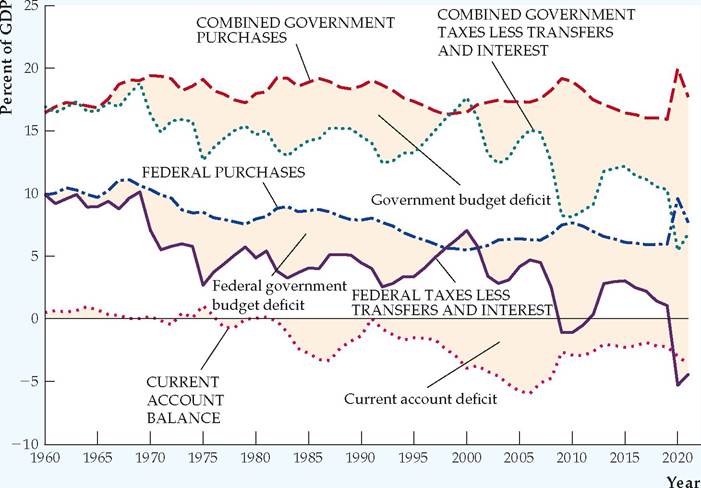

FIGURE 5.9

The government budget deficit and the current account in the United States, 1960-2021

Shown are government purchases, net government income (taxes less transfers and interest), and the current account balance for the United States for 1960-2021. All data series are measured as a percentage of GDP. The government deficit (beige) is the excess of government purchases over net government income. The simultaneous appearance of the government budget deficit and the current account deficit in the 1980s and early 1990s is the twin-deficits phenomenon.

Sources: Total government and Federal government receipts, current expenditures, interest, and transfers: BEA website, www.bea.gov, NIPA Tables 3.1 and 3.2. GDP: BEA website, NIPA Table 1.1.5. Current account balance: BEA website, International transactions accounts Table 1.1.

The apparently close relationship between the U.S. government budget deficit and the current account deficit in the 1980s and the first half of the 1990s is consistent with the twin-deficits idea that budget deficits cause current account deficits.

Because the rise in budget deficits primarily reflected tax cuts (or increases in transfers and interest payments, which reduced net government income) rather than increased government purchases, this behavior of the two deficits also seems to contradict the Ricardian equivalence proposition, which says that tax cuts should have no effect on saving or the current account.Even though the U.S. experience during the 1980s and first half of the 1990s seems to confirm the link between government budget and the current account, evidence from other episodes is less supportive of the twin-deficits idea. For example, the United States simultaneously ran large government budget deficits and large current account surpluses in the periods around World War I and II (compare Figs. 1.5 and 1.6). In the late 1990s, the Federal government budget and the combined government budget were both in surplus, yet the U.S. current account balance remained deeply in deficit because private saving fell and investment rose as a share of GDP at the same time. And from 2008 to 2011, the government budget deficit grew substantially as the government increased spending to stimulate the economy, but the current account deficit fell considerably as consumers cut back on their purchases of imported goods and services.

The evidence from other countries on the relationship between government budget and current account deficits is also mixed. The International Monetary Fund (IMF) conducted a systematic analysis of the twin deficits in a group of 17 countries over the period 1978-2009.[87] Almost two-thirds of the 291 changes in fiscal policy in this sample of countries were reductions in the government budget deficit. The IMF found that a change in fiscal policy that reduces the government budget deficit by 1% of GDP typically reduces the current account deficit by a little more than 0.5% of GDP. Nevertheless, a good deal of disagreement persists among economists about the relationship between government budget deficits and current account deficits.[88] We can say for sure (because it is implied by the uses-of-saving identity, Eq. [2.11]) that if an increase in the government budget deficit is not offset by an equal increase in private saving, the result must be a decline in domestic investment, a rise in the current account deficit, or both.

►