Saving and Investment in Large Open Economies

Discuss the factors that affect saving and investment and determine the current account balance in a large open economy.

Although the model of a small open economy facing a fixed real interest rate is appropriate for studying many of the countries in the world, it isn't the right model to use for analyzing the world's major developed economies.

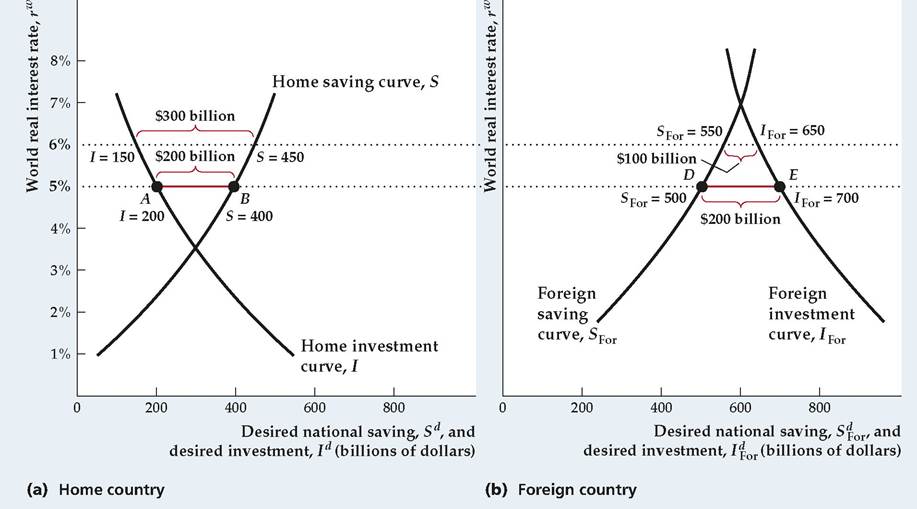

The problem is that significant changes in the saving and investment of a major economy can and do affect the world real interest rate, which violates the assumption made for the small open economy that the world real interest rate is fixed. Fortunately, we can readily adapt the analysis of the small open economy to the case of a large open economy, that is, an economy large enough to affect the world real interest rate.To begin, let's think of the world as comprising only two large economies: (1) the home, or domestic economy, and (2) the foreign economy (representing the economies of the rest of the world combined). Figure 5.5 shows the saving-investment diagram that applies to this case. Figure 5.5(a) shows the saving curve, S, and the investment curve, I, of the home economy. Figure 5.5(b) displays the saving curve, SFor, and the investment curve, I For, of the foreign economy. These saving and investment curves are just like those for the small open economy.

Instead of taking the world real interest rate as given, as we did in the model of a small open economy, we determine the world real interest rate within the model for a large open economy. What determines the value of the world real interest rate? Remember that for the closed economy the real interest rate was set by the condition that the amount that savers want to lend must equal the amount that investors want to borrow. Analogously, in the case of two large open economies, the world real interest rate will be such that desired international lending by one country equals desired international borrowing by the other country.

To illustrate the determination of the equilibrium world real interest rate, we return to Fig. 5.5. Suppose, arbitrarily, that the world real interest rate, rw, is 6%. Does this rate result in a goods market equilibrium? Figure 5.5(a) shows that, at a 6% real interest rate, in the home country desired national saving is $450 billion and desired investment is $150 billion. Because desired national saving exceeds desired investment by $300 billion, the amount that the home country would like to lend abroad is $300 billion.

To find how much the foreign country wants to borrow, we turn to Fig. 5.5(b). When the real interest rate is 6%, desired national saving is $550 billion and desired investment is $650 billion in the foreign country. Thus at a 6% real interest rate the foreign country wants to borrow $100 billion ($650 billion less $550 billion) in the international capital market. Because this amount is less than the $300 billion the home country wants to lend, 6% is not the real interest rate that is consistent with equilibrium in the international capital market.

FIGURE 5.5

The determination of the world real interest rate with two large open economies

The equilibrium world real interest rate is the real interest rate at which desired international lending by one country equals desired international borrowing by the other country. In the figure, when the world real interest rate is 5%, desired international lending by the home country is $200 billion ($400 billion desired national saving less $200 billion desired investment, or distance AB), which equals the foreign country's desired international borrowing of $200 billion ($700 billion desired investment less $500 billion desired national saving, or distance DE). Thus 5% is the equilibrium world real interest rate. Equivalently, when the interest rate is 5%, the current account surplus of the home country equals the current account deficit of the foreign country (both are $200 billion).

At a real interest rate of 6%, desired international lending exceeds desired international borrowing, so the equilibrium world real interest rate must be less than 6%. Let's try a real interest rate of 5%. Figure 5.5(a) shows that at that interest rate desired national saving is $400 billion and desired investment is $200 billion in the home country, so the home country wants to lend $200 billion abroad. In Fig. 5.5(b), when the real interest rate is 5%, desired national saving in the foreign country is $500 billion and desired investment is $700 billion, so the foreign country's desired international borrowing is $200 billion. At a 5% real interest rate, desired international borrowing and desired international lending are equal (both are $200 billion), so the equilibrium world real interest rate is 5% in this example.

Graphically, the home country's desired lending when rw equals 5% is distance AB in Fig. 5.5(a), and the foreign country's desired borrowing is distance DE in Fig. 5.5(b). Because distance AB equals distance DE, desired international lending and borrowing are equal when the world real interest rate is 5%.

We defined international equilibrium in terms of desired international lending and borrowing. Equivalently, we can define equilibrium in terms of international flows of goods and services. The amount the lending country desires to lend (distance AB in Fig. 5.5a) is the same as its current account surplus. The amount the borrowing country wants to borrow (distance DE in Fig. 5.5b) equals its current account deficit. Thus saying that desired international lending must equal desired international borrowing is the same as saying that the desired net outflow of goods and services from the lending country (its current account surplus) must equal the desired net inflow of goods and services to the borrowing country (its current account deficit).

In summary, for a large open economy the equilibrium world real interest rate is the rate at which the desired international lending by one country equals the desired international borrowing of the other country.

Equivalently, it is the real interest rate at which the lending country's current account surplus equals the borrowing country's current account deficit.Unlike the situation in a small open economy, for large open economies the world real interest rate is not fixed but will change when desired national saving or desired investment changes in either country. Generally, any factor that increases desired international lending relative to desired international borrowing at the initial world real interest rate causes the world real interest rate to fall. Similarly, a change that reduces desired international lending relative to desired international borrowing at the initial world real interest rate will cause the world real interest rate to rise.

Application

The Impact of Globalization on the U.S. Economy

Section 5.1, "Balance of Payments Accounting," showed how the international balance of payments accounts keep track of international trade and investment. These accounts reveal that the world's economies have become increasingly interdependent, as the volume of trade in goods and services has increased and as people in one country have increased their investment in other countries. This globalization is not without its consequences, and some people have argued that the United States needs to rein in the degree of globalization, restricting trade or international investment. To evaluate such proposals, we need to examine the facts about globalization, including how it has affected U.S. trade with other countries, how trade in services has changed, and how international investment has been altered.

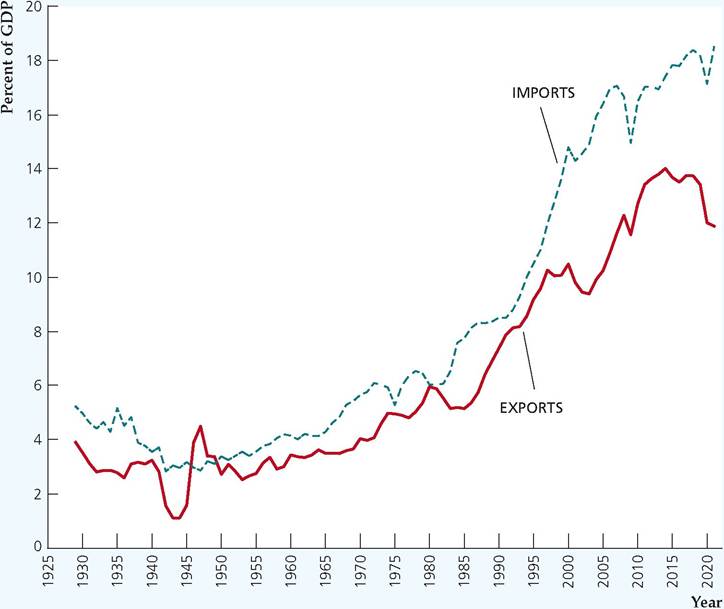

To begin, let's look at how U.S. trade with other countries has changed over time. If we examine exports of goods and services as a percentage of our GDP, we can see the relative importance of exports in the economy; similarly for imports. Figure 5.6 shows both statistics from 1929 to 2021. After World War II, both exports and imports rose gradually relative to GDP until the mid 1980s, when both began growing more rapidly.

From the mid 1980s to 2006, imports generally outpaced exports, thereby leading to a trade deficit that peaked at about 6.0% of GDP. The recession from 2007 to 2009 led to a reduction in imports relative to GDP, reducing the trade deficit to about 3%. Since 2014, the trade deficit rose, reaching over 6% of GDP by 2021.In addition to increased trade in goods and services, investors have also increased their investments in foreign countries since the mid 1980s. As we saw in Fig. 5.1 in the Application "The United States as International Debtor," ownership of foreign assets by U.S. investors has increased rapidly, and ownership of U.S. assets by foreign investors has increased even more rapidly, so that the

FIGURE 5.6

Exports and imports of goods and services as a percent of GDF* 1929-2021

The chart shows annual values for exports of goods and services from the United States and imports into the United States for the period 1929 to 2021.

Sources: Exports and imports: Bureau of Economic Analysis, Trade in Goods and Services, available at fred.stlouisfed.org/ series/EXPGSCA and IMPGSCA. GDP: Bureau of Economic Analysis, National Income and Product Accounts, available at fred.stlouisfed.org/series/GDPCA.

United States has gone from being a net international creditor prior to the mid 1980s (with U.S. ownership of foreign assets exceeding foreign ownership of U.S. assets) to a net international debtor (with U.S. ownership of foreign assets being less than foreign ownership of U.S. assets) today.

As the U.S. economy has become more interdependent with other economies, there have been some costs and complaints. Increased openness means that jobs in some sectors of the U.S. economy may be eliminated, as a particular good is produced by workers in another country. Often workers complain that they have lost their jobs to foreign workers. And there have been instances, widely reported in the U.S.

business press, in which a company shuts down a facility in the United States and opens one to do the same work in a foreign country. There are costs in foreign countries as well. In the fourth quarter of 2008, U.S. GDP declined at an annualized rate of about 8% because of the financial crisis and recession. But countries in Asia that produced many goods that they export to the United States suffered declines of 12% (at an annualized growth rate) and more in their GDPs, as U.S. demand for their products declined dramatically.Some people conclude that international trade destroys jobs. But international trade also creates jobs. Generally, the gains from increasing trade between countries exceed the costs. But the adjustment period can be painful in areas where jobs have been lost. A possible role for the government could be to help people adjust, for example, by helping them retrain to find new jobs. Otherwise, there may be people who lose from increased trade.

Research by David H. Autor of MIT, David Dorn of CEMFI, and Gordon H. Hansen of the University of California, San Diego, analyzed the impact of imports from China on U.S. labor markets from 1990 to 2007.8 They found that imports from China into the United States led to increased unemployment, lower wages for workers, and reduced labor force participation in many local labor markets that produced goods that were directly exposed to competition from Chinese imports. Compared with the past, the shock to local labor markets was much larger and more abrupt. As a result, transfer payments in the form of unemployment benefits and disability payments to displaced workers were substantial. Although trade with other countries brings benefits, there are significant costs that governments should understand.

8"The China Syndrome: Local Labor Market Effects of Import Competition in the United States,” American Economic Review, October 2013, pp. 2121-2168.

Application

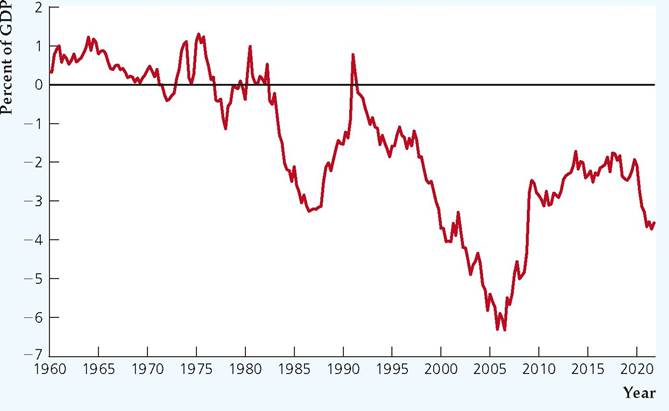

FIGURE 5.7

Current account balance as a percent of GDP, 1960Q1-2021Q4

The chart shows quarterly values for the current account balance as a percent of GDP for the period from the first quarter of 1960 to the fourth quarter of 2021.

Sources: Balance on current account: Bureau of Economic Analysis, available online at fred.stlouisfed.org/series/NETFI. GDP: Bureau of Economic Analysis, available at fred.stlouisfed.org/series/GDP.

up foreign exchange reserves, and became net lenders to foreign countries instead of net borrowers.

After 2005, other developments contributed to a continuation of the global increase in saving, including an increase in the current account balances of Germany and other countries in Europe. The consequence has been low global interest rates. Those rates may begin to rise when the reasons for the increased saving diminish in the future.

A country can have a current account deficit overall but have bilateral current account surpluses with some countries and current account deficits with other countries. Those bilateral balances reflect the specific nature of trade between the countries. For example, suppose a country like China has many manual laborers with low wages. Firms bring many unfinished goods to China from other countries and assemble them into final products in China. Because U.S. consumers buy many manufactured goods and because China is the final assembly point for many such goods, the United States runs a large bilateral trade deficit with China. That bilateral trade deficit thus mainly arises because U.S. consumers desire manufactured goods. The size of the bilateral trade deficit is exacerbated by the fact that in the international trade statistics, the entire value of the final manufactured good is counted as an import into the United States from China, even though many of the component parts may have come from other countries. Thus the bilateral trade balance is a misleading indicator of the value of U.S. trade with China.

Here is a simple example of how this works and why the U.S. bilateral trade deficit with China is not something we should worry about. Consider a hair stylist who produces haircuts and a butcher who produces meat in a grocery. The stylist buys meat from the butcher and thus has a trade deficit with the stylist. But the stylist sells haircuts to many other people and uses the income from those haircuts to pay for the meat from the butcher. Thus the stylist's trade surpluses with others covers the bilateral trade deficit with the butcher.

What might happen if a country imposes restrictions, such as tariffs, on imported goods? The demand for the goods with tariffs will decline because they

will become more expensive. But, most likely, the other country will retaliate with tariffs of its own. As a result, tariffs are unlikely to reduce the bilateral trade balance or the overall trade balance. Most likely, both countries will produce less total output, as the gains from comparative advantage will be lost.10 Thus both countries will be worse off, and the trade balances are unlikely to change significantly.

10Comparative advantage is the idea that some countries are relatively good at producing certain goods, while other countries are relatively good at producing other goods. Ideally, each country produces the goods that it is relatively better at producing and trades with other countries, and thus the total output of the world economy is higher.

5.5