Saving and Investment in a Small Open Economy

Discuss the factors that affect saving and investment and determine the current account balance in a small open economy.

To show how saving and investment are related to international trade and lending, we first present the case of a small open economy.

A small open economy is an economy that is too small to affect the world real interest rate. The world real interest rate is the real interest rate that prevails in the international capital market—that is, the market in which individuals, businesses, and governments borrow and lend across national borders. Because changes in saving and investment in the small open economy aren't large enough to affect the world real interest rate, this interest rate is fixed in our analysis, which is a convenient simplification. Later in this chapter we consider the case of an open economy, such as the U.S. economy, that is large enough to affect the world real interest rate.As with the closed economy, we can describe the goods market equilibrium in a small open economy by using the saving-investment diagram. The important new assumption that we make is that residents of the economy can borrow or lend in the international capital market at the (expected) world real interest rate, rw, which for now we assume is fixed. If the world real interest rate is rw, the domestic real interest rate must be rw as well, as no domestic borrower with access to the international capital market would pay more than rw to borrow, and no domestic saver with access to the international capital market would accept less than rw to lend.[84]

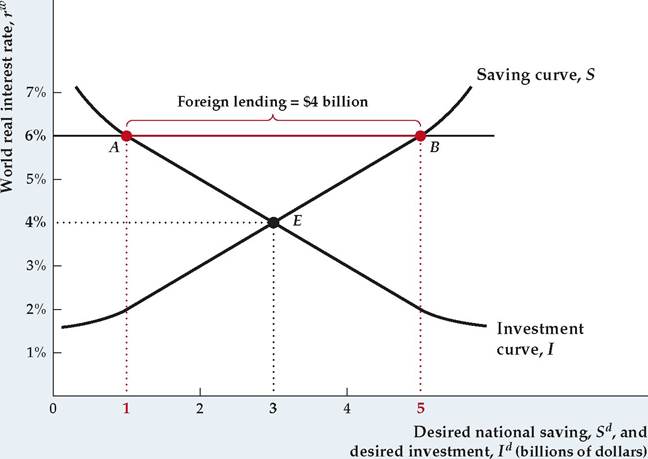

Figure 5.2 shows the saving and investment curves for a small open economy. In a closed economy, goods market equilibrium would be represented by point E, the intersection of the curves. The equilibrium real interest rate in the closed economy would be 4% (per year), and national saving and investment would be $3 billion (per year).

In an open economy, however, desired national saving need not equal desired investment. If the small open economy faces a fixed world real interest rate, rw, higher than 4%, desired national saving will be greater than desired investment. For example, if rw is 6%, desired national saving is $5 billion and desired investment is $1 billion, so desired national saving exceeds desired investment by $4 billion.

Can the economy be in equilibrium when desired national saving exceeds desired investment by $4 billion? In a closed economy it couldn't. The excess saving would have no place to go, and the real interest rate would have to fall to bring desired saving and desired investment into balance. However, in the open economy the excess $4 billion of saving can be used to buy foreign assets. This financial outflow uses up the excess national saving so that there is no disequilibrium. Instead, the goods market is in equilibrium with desired national saving of $5 billion, desired investment of $1 billion, and net foreign lending of $4 billion (see Eq. 5.4 and recall that net exports, NX, and net foreign lending are equal).

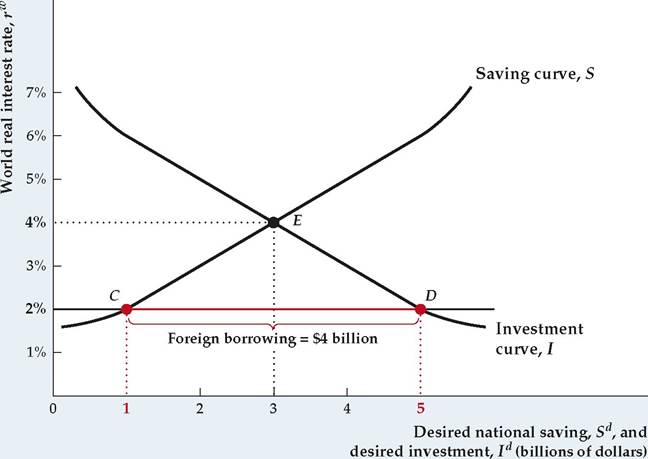

Alternatively, suppose that the world real interest rate, rw, is 2% instead of 6%. As Figure 5.3 shows, in this case desired national saving is $1 billion and desired investment is $5 billion so that desired investment exceeds desired saving by $4 billion. Now firms desiring to invest will have to borrow $4 billion in the international capital market. Is this also a goods market equilibrium? Yes it is, because desired national saving ($1 billion) again equals desired investment ($5 billion) plus net foreign lending (minus $4 billion). Indeed, a small open economy can achieve goods market equilibrium for any value of the world real interest rate. All that is required is that net foreign lending equal the difference between the country's desired national saving and its desired investment.

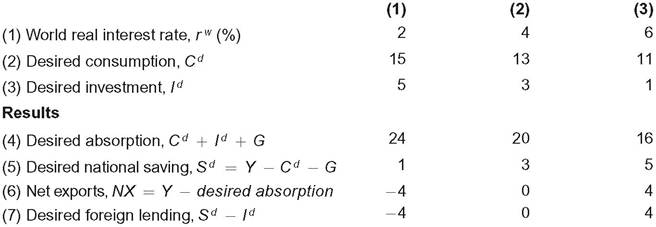

A more detailed version of the example illustrated in Figs. 5.2 and 5.3 is presented in Table 5.3. As shown in the top panel, we assume that in this small country gross domestic product, Y, is fixed at its full-employment value of $20 billion

FIGURE 5.3

A small open economy that borrows abroad

The same small open economy shown in

Fig. 5.2 now faces a fixed world real interest rate of 2%. At this real interest rate, national saving is $1 billion (point C) and investment is $5 billion (point D). Foreign borrowing of $4 billion (distance CD) makes up the difference between what investors want to borrow and what domestic savers want to lend.

TABLE 5.3

Goods Market Equilibrium in a Small Open Economy: An Example (Billions of Dollars)

Given

Gross domestic product, Y 20

Government purchases, G 4

Effect of real interest rate on desired consumption and investment

Note: We assume that net factor payments, NFP, and net unilateral transfers equal zero.

and government purchases, G, are fixed at $4 billion. The middle panel shows three possible values for the world real interest rate, rw, and the assumed levels of desired consumption and desired investment at each of these values of the real interest rate. Note that higher values of the world real interest rate imply lower levels of desired consumption (because people choose to save more) and lower desired investment. The bottom panel shows the values of various economic quantities implied by the assumed values in the top two panels.

The equilibrium in this example depends on the value of the world real interest rate, rw. Suppose that rw = 6%, as shown in Fig. 5.2. Column (3) of Table 5.3 shows that, if rw = 6%, desired consumption, Cd, is $11 billion (row 2) and that desired investment, Id, is $1 billion (row 3).

With Cd at $11 billion, desired national saving, Y — Cd — G, is $5 billion (row 5). Desired net foreign lending, Sd — Id, is $4 billion (row 7)—the same result illustrated in Fig. 5.2.If rw = 2%, as in Fig. 5.3, column (1) of Table 5.3 shows that desired national saving is $1 billion (row 5) and that desired investment is $5 billion (row 3). Thus desired foreign lending, Sd — Id, equals —$4 billion (row 7)—that is, foreign borrowing totals $4 billion. Again, the result is the same as illustrated in Fig. 5.3.

An advantage of working through the numerical example in Table 5.3 is that we can also use it to demonstrate how the goods market equilibrium, which we've been interpreting in terms of desired saving and investment, can be interpreted in terms of output and absorption. Suppose again that rw = 6%, giving a desired consumption, Cd, of $11 billion and a desired investment, Id, of $1 billion. Government purchases, G, are fixed at $4 billion. Thus when rw is 6%, desired absorption (the desired spending by domestic residents), Cd + Id + G, totals $16 billion (row 4, column 3).

In goods market equilibrium a country's net exports—the net quantity of goods and services that it sends abroad—equal gross domestic product, Y, minus desired absorption (Eq. 5.6). When rw is 6%, Y is $20 billion and desired absorption is $16 billion so that net exports, NX, are $4 billion. Net exports of $4 billion imply that the country is lending $4 billion abroad, as shown in Fig. 5.2. If the world real interest rate drops to 2%, desired absorption rises (because people

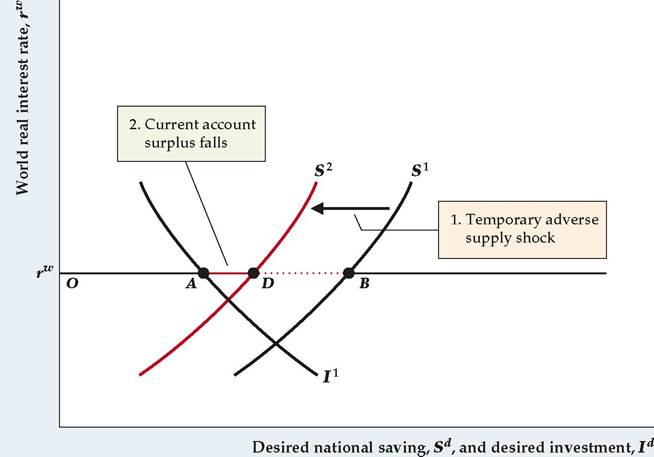

FIGURE 5.4

A temporary adverse supply shock in a small open economy Curve S1 is the initial saving curve, and curve 11 is the initial investment curve of a small open economy. With a fixed world real interest rate of rw, national saving equals the distance OB and investment equals distance OA.

The current account surplus (equivalently, net foreign lending) is the difference between national saving and investment, shown as distance AB. A temporary adverse supply shock lowers current output and causes consumers to save less at any real interest rate, which shifts the saving curve left, from S1 to S2.National saving decreases to distance OD, and the current account surplus decreases to distance AD.

want to consume more and invest more) from $16 billion to $24 billion (row 4, column 1). Because in this case absorption ($24 billion) exceeds domestic production ($20 billion), the country has to import goods and services from abroad (NX = — $4 billion). Note that desired net imports of $4 billion imply net foreign borrowing of $4 billion, as shown in Fig. 5.3.

The Effects of Economic Shocks in a Small Open Economy

The saving-investment diagram can be used to determine the effects of various types of economic disturbances in a small open economy. Briefly, any change that increases desired national saving relative to desired investment at a given world real interest rate will increase net foreign lending, the current account balance, and net exports, which are all equivalent under our assumption that net factor payments from abroad and net unilateral transfers are zero. A decline in desired national saving relative to desired investment reduces those quantities. Let's look at an example.

Suppose that a small open economy is hit with a severe drought—an adverse supply shock—that temporarily lowers output. The effects of the drought on the nation's saving, investment, and current account are shown in Figure 5.4. The initial saving and investment curves are S1 and 11, respectively. For the world real interest rate, rw, initial net foreign lending (equivalently, net exports or the current account balance) is distance AB.

The drought brings with it a temporary decline in income. A drop in current income causes people to reduce their saving at any prevailing real interest rate, so the saving curve shifts left, from S1 to S2. If the supply shock is temporary, as we have assumed, the expected future marginal product of capital is unchanged. As a result, desired investment at any real interest rate is unchanged, and the investment curve does not shift. The world real interest rate is given and does not change.

In the new equilibrium, net foreign lending and the current account have shrunk to distance AD. The current account shrinks because the country saves less and thus is not able to lend abroad as much as before.

In this example, we assumed that the country started with a current account surplus, which is reduced by the drought. If, instead, the country had begun with a current account deficit, the drought would have made the deficit larger. In either case the drought reduces (in the algebraic sense) net foreign lending and the current account balance.

5.4