Individual R&D Uncertainty and the Stock Market

The final issue I discuss in this chapter involves uncertainty in the research process. As discussed at the beginning of the chapter, it is reasonable to presume that the output of research will be uncertain.

This implies that individual firms undertaking research will face a stochastic revenue stream. When individuals are risk averse, this may imply that there should be a risk premium associated with such stochastic streams of income. This is not necessarily the case, however, when the following three conditions are satisfied:(1) there are many firms involved in research;

(2) the realization of the uncertainty across firms is independent;

(3) households and firms have access to a “stock market,” where each consumer can hold a balanced portfolio of various research firms.

In many of the models presented in the next two chapters, firms will face uncertainty (for example, regarding whether their R&D will be successful or how long their monopoly position will last), but the three conditions outlined here will be satisfied. When this is the case, even though each firm’s revenue is risky, the balanced portfolio held by the representative household will have deterministic returns. Here I illustrate this with a simple example.

EXAMPLE 12.2. Suppose that the representative household has a utility function over consumption given by u (c), where u (∙) is strictly increasing, differentiable and strictly concave, so that individual is risk averse. Moreover, let us assume that limc→o u0 (c) = ∞, so that the marginal utility of consumption at zero is very high. The household starts with an endowment equal to ó > 0. This endowment can be consumed or it can be invested in a risky R&D project. Imagine that the R&D project is successful with probability p and will have a return equal to 1 + R > 1/p per unit of investment.

It is unsuccessful with probability 1 — p, in which case it will have a zero return. When this is the only project available, the household would be facing consumption risk if it invests in this project. In particular, the maximization problem that determines how much it should invest will be a solution to the following expected utility maximization

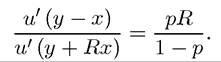

The first-order condition of this problem implies that the optimal amount of investment in the risky research activity will be given by:

The assumption limc→o u' (c) = ∞ implies that x < ó, thus less than the full endowment of the individual will be invested in the research activity, even though this is a positive expected return project. Intuitively, the household requires a risk premium to bear the consumption risk associated with the risky investment.

Next imagine a situation in which many different firms can invest in similar risky research ventures. Suppose that the success or failure of each pro ject is independent of the others. Imagine that the individual invests an amount x/N in each of N projects. The Strong Law of Large Numbers implies that as N → ∞, a fraction p of these projects will be successful and the remaining fraction 1 — p will be unsuccessful. Therefore, the household will receive (almost surely) a utility of

Since 1 + R > 1/p, this is strictly increasing in x, and implies that the individual would prefer to invest all of its endowment in the risky projects, that is, x = y. Therefore, the ability to hold a balanced portfolio of projects with independently disputed returns allows the household to diversify the risks and act in a risk-neutral manner. A similar logic will apply in many of the models presented in the next three chapters; even though individual firms will have stochastic returns, the representative household will hold a balanced portfolio of all the firms in the economy and thus will have risk-neutral preferences in the aggregate. This observation also implies that the ob jective of each firm will be to maximize expected profits (without a risk premium).

12.6.