Inflation and Aggregate Fluctuations under a Taylor Rule

Because there is no capital and investment in this model, and no distinction between private and government consumption expenditure, product market equilibrium implies that output is equal to consumption:

This product market equilibrium condition allows us to substitute output for consumption in the money demand function and the Euler equation for consumption, and derive optimal aggregate money and output demand functions.

17.7.1 New Neoclassical Synthesis IS-LM Functions

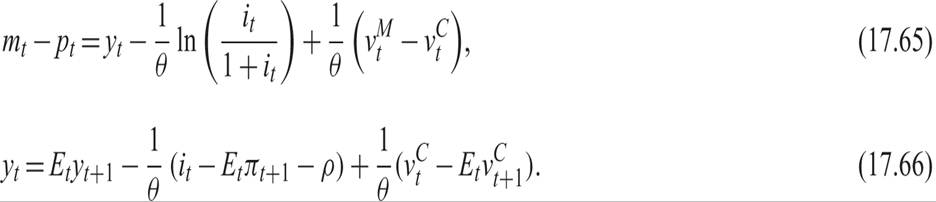

Substituting (17.64) in (17.14) and (17.15), we get the following money and output aggregate demand functions:

Equation (17.65) can be seen as the money market equilibrium condition, the equivalent of the LM curve in the traditional models of the neoclassical synthesis. Equation (17.66) is the product market equilibrium condition, the equivalent of the IS curve. Because (17.65) and (17.66) are derived from an explicit problem of intertemporal optimization by the representative household, let us refer to them the new neoclassical synthesis LM curve and IS curves, respectively.14

17.7.2 The Natural and Equilibrium Real Interest Rate

The real interest rate is defined by the Fisher [1896] equation, first introduced in chapter 2:

As with other real variables, let us distinguish between the current and the natural real interest rate. The natural real interest rate is determined by the product market equilibrium condition, when output is at its natural rate. From (17.42) and (17.66), the natural real interest rate is thus determined by

The natural real interest rate is equal to the pure rate of time preference, but it also depends positively on deviations of current shocks to consumption from anticipated future shocks, and negatively on deviations of current productivity shocks from anticipated future shocks.

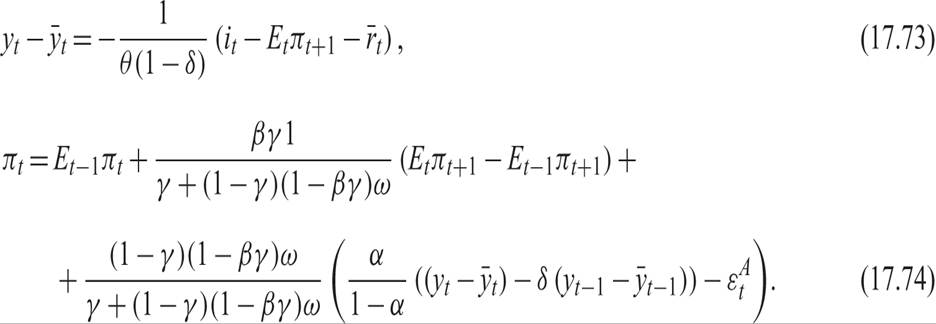

Hence, the natural real interest rate is affected by real shocks, such as productivity and consumption preference shocks. Productivity shocks, which cause a temporary increase in the natural level of output, lead to a reduction of the natural real rate of interest, inducing a corresponding increase in consumption and maintaining product market equilibrium. Real consumption preference shocks, which cause a temporary increase in consumption, require an increase in the natural real rate of interest, reducing consumption back to the natural level of output and maintaining product market equilibrium.Because of the existence of predetermined one-period nominal wage contracts, and because of staggered pricing, the current equilibrium real interest rate deviates from its natural rate to the extent that current output deviates from its own natural rate. Solving the new neoclassical synthesis IS curve (17.66) for the real interest rate and using (17.42) for the natural rate of output, we get that the current real interest rate is given by

Deviations of the current real interest rate from its natural rate depend negatively on deviations of output from its own natural rate. Because deviations of output from its natural rate tend to persist, deviations of the real interest rate from its own natural rate will tend to persist as well.

Shocks to inflation or productivity, which cause a temporary rise in current output relative to its natural rate, affect output by reducing the current real interest rate relative to its natural rate.15

17.7.3 Equilibrium Fluctuations with Exogenous Preference and Productivity Shocks

In what follows, let us assume that the logarithms of the exogenous shocks to preferences and productivity follow stationary AR(1) processes of the form

where the autoregressive parameters satisfy 0 < ηC, ηM, ηA < 1, and εC, εM, εA, are white noise processes.16

With these assumptions, for a given nominal interest rate, fluctuations in output and inflation will be determined by the new neoclassical synthesis IS relation (17.66), and the extended new Keynesian Phillips curve (17.63).

Expressing these as deviations from natural rates, we get

The natural rates of real variables, such as output,  , and the real interest rate rt, evolve as functions of the exogenous real shocks only. Using (17.70) and (17.72) to substitute for productivity and real consumption shocks in (17.42) and (17.68), we get

, and the real interest rate rt, evolve as functions of the exogenous real shocks only. Using (17.70) and (17.72) to substitute for productivity and real consumption shocks in (17.42) and (17.68), we get

alt=eq17-75-76.png>

Thus, deviations of real output from its natural rate depend on the current nominal interest rates, expected future inflation, and shocks to the natural real rate of interest; inflation is determined through the dynamic stochastic Phillips curve (17.74).

To solve the model, one needs an assumption about the determination of the nominal interest rate. Let us assume that this is determined by the central bank, which follows a Taylor rule of the form

where ϕπ, ϕy > 0 are policy parameters, and  is a white noise monetary policy shock. According to this rule, the central bank aims for a nominal interest rate that is equal to the natural real rate of interest, plus a target inflation rate equal to the steady state inflation rate π*. If actual inflation is higher than the target π*, then the central bank raises interest rates to reduce inflation toward its target. In addition, if output is higher than its natural rate, then the central bank increases nominal interest rates to reduce aggregate demand and bring output back to its natural rate.17

is a white noise monetary policy shock. According to this rule, the central bank aims for a nominal interest rate that is equal to the natural real rate of interest, plus a target inflation rate equal to the steady state inflation rate π*. If actual inflation is higher than the target π*, then the central bank raises interest rates to reduce inflation toward its target. In addition, if output is higher than its natural rate, then the central bank increases nominal interest rates to reduce aggregate demand and bring output back to its natural rate.17

We can use the Taylor rule (17.77) to substitute for the nominal interest rate in the aggregate demand equation (17.73), and then substitute for deviations of output from its natural rate in the dynamic stochastic Phillips curve (17.74), to derive an inflation equation that depends only on inflation terms and on real and nominal shocks.

Proceeding with these substitutions we get a transformed inflation process of the form18

where  = π − π* is the deviation of current inflation from steady state inflation (the target of the central bank), and the κ coefficients are defined as

= π − π* is the deviation of current inflation from steady state inflation (the target of the central bank), and the κ coefficients are defined as

To solve for inflation, we first take expectations of (17.78) conditional on information available up to the end of period t − 1. This yields

The process (17.80) will be stable if and only if

It is straightforward to show that a necessary and sufficient condition for (17.81) to hold is

Condition (17.82) reflects the Taylor principle. It requires that nominal interest rates react sufficiently strongly to deviations of current inflation from target inflation to affect real interest rates and aggregate demand in the desired direction. This is a necessary and sufficient condition for a stable and determinate process for expected (and actual) inflation.19

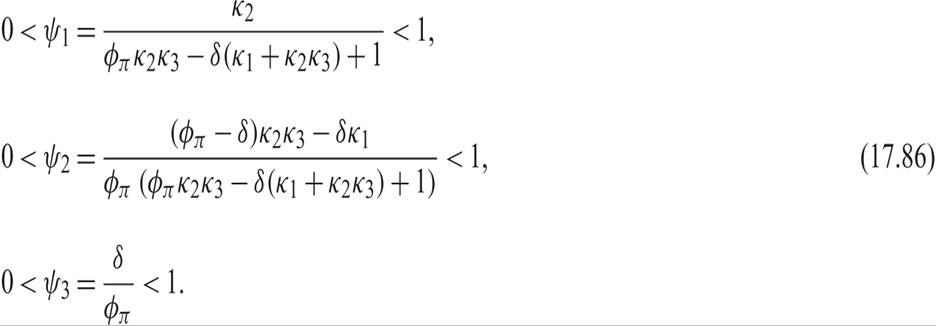

If (17.82) is satisfied, then it is straightforward to show that the expected inflation process has two roots that lie on either side of unity. The smaller root is δ, and the larger root is ϕπ. Thus, the solution for the expected inflation process (17.80) is given by

where δ < 1 is the smaller root of the characteristic polynomial of (17.81).

From (17.83), it follows that

Substituting (17.83) and (17.84) in the inflation process (17.78), the rational expectations solution for inflation is given by

where

From (17.85), fluctuations of inflation around the target of the monetary authorities π* are as persistent as fluctuations of unemployment and output around their natural rates. They are driven by the current innovation in productivity and current and past monetary policy shocks, as the central bank is using the short-run trade-off between inflation and unemployment to partly counteract the real effects of such shocks.

Note that the inflationary process displays persistence only because of the persistence of unemployment. This is because under the Taylor rule, the central bank seeks to counteract deviations of unemployment and output from their natural rates, something that conflicts with the objectives of wage setters, who are seeking to maintain persistent deviations of unemployment and output from their natural rates. It is because of the clash in the objectives of wage setters and the central bank that inflation persists.20

It is also worth noting that all structural parameters (including the parameters of the Taylor rule) affect the inflation process, through the expectations of consumers, wage setters, and firms, and through deviations of unemployment, output, and the real interest rate from their natural rates.

Because of the persistence of deviations of output from its natural rate, both current and past monetary policy shocks affect the inflationary process. The effects of productivity and monetary policy shocks on inflation also depend on all structural parameters, including the parameters of the Taylor rule.21

Having solved for inflation, the solution of the rest of the model is straightforward.

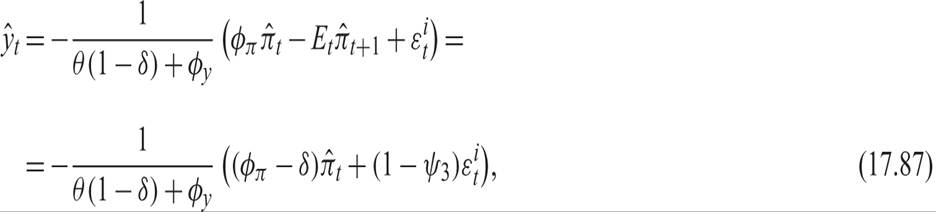

Substituting the Taylor rule (17.77) into the new neoclassical synthesis IS relation (17.73), which determines deviations of output from its natural rate, and solving for ŷt, we get

where  denotes deviations of output from its natural rate.

denotes deviations of output from its natural rate.

Substituting (17.85) in (17.87) and solving out for ŷt, we get

where

Finally, using the Okun relation (17.62) in conjunction with (17.88), we can solve for the fluctuations of the unemployment rate around its natural rate:

Fluctuations in both nominal variables (such as the inflation rate) and real variables (such as deviations of real output and the unemployment rate from their natural rates) display the same degree of persistence. This is a result of the clash in the objectives of central bankers and labor market insiders. The central bank, through the Taylor rule, seeks to stabilize both inflation and deviations of output from its natural rate. Labor market insiders seek to secure the maximum wage consistent with their own employment, which depends partly on lagged employment and partly on the natural rate.

To the extent that the short-term employment objectives of wage setters and the central bank differ, with the central bank seeking to minimize persistent deviations of unemployment from its natural rate, the only way for wage setters to ensure that the central bank does not surprise them is to adapt their inflationary expectations to the central bank rule. Because nominal interest rates react to the persistent fluctuations of deviations of output from its natural rate, inflation and inflationary expectations adapt too. Hence, inflation displays the same degree of persistence as output and unemployment.22

17.7.4 Does Staggered Pricing Matter for Inflation Persistence?

It is important to demonstrate that most of the results go through even in the absence of staggered pricing. Inflation displays persistence under a Taylor rule, even in the case where prices are fully flexible, as long as nominal wage contracts are predetermined, as assumed by the model.

To demonstrate that staggered pricing does not matter for inflation persistence, assume that γ = 0. Then, it follows that the dynamic stochastic Phillips curve (17.74) takes the form

Deviations of output from its natural rate still cause unanticipated inflation, but the extra terms involving expected future inflation drop out.

Using the Taylor rule (17.77) to substitute for the nominal interest rate in the aggregate demand equation (17.73), and then substituting for deviations of output from its natural rate in the Phillips curve (17.91), results in a transformed inflation process of the form

where κ3 is defined in the same way as before (equation (17.79)). However, because of the assumption that γ = 0, it follows from (17.79) that κ1 = 0 and that κ2 = 1.

The rational expectations solution for expected inflation is the same as before (given by (17.80)), as ex ante expected current inflation does not depend on staggered pricing, but only on the degree of persistence of unemployment δ and the Taylor rule response to inflation ϕπ.

The rational expectations solution for actual inflation is the same as (17.85), except that the parameters measuring the impact of the unanticipated shocks now simplify to

Hence, inflation follows a process similar to (17.85), with a degree of persistence equal to δ even in the absence of staggered pricing.

Substituting the modified inflation process in the new neoclassical synthesis IS relation (17.73), using the Taylor rule to substitute for the nominal interest rate, and solving out, the processes determining the fluctuations of real output and unemployment are given by equations similar to (17.88) and (17.90) with the ψ values redefined as in (17.93). Hence, staggered pricing does not matter for the persistence of either inflation or real variables in this model. It only matters for the transmission of current real and nominal shocks, through the ψ parameters.

Exercise 17.1 Consider the model with periodic wage contracts and unemployment persistence, but perfectly flexible prices. The expectations-augmented Phillips curve is given by (17.44). Solve the model for fluctuations in output, unemployment, and inflation, using the new neoclassical synthesis IS curve (17.66), the Taylor rule (17.77), the Okun-type relation (17.62), and the assumptions made about the exogenous shocks in (17.70)–(17.72). Discuss your findings, and compare them to the findings in the main text, in the presence of staggered pricing.

17.7.5 Inflation Stabilization and the Divine Coincidence

Note that, unlike the bechmark new Keynesian model with staggered prices, analyzed in chapter 16, this model is not characterized by the divine coincidence of output stabilization when inflation itself is stabilized. Stabilization of inflation around the target inflation rate of the central bank does not automatically lead to output and employment stabilization around their natural rates. This is because of the labor market distortions implied by the wage-setting behavior of insiders.23

To see this, assume that the central bank allows its response to deviations of inflation from its target ϕπ to become infinite. Then from the definition of the ψ parameters in (17.86), ψ1, ψ2, and ψ3 would be driven to zero, and neither nominal nor real shocks would affect inflation. Inflation would converge to the target rate of the central bank π*, and the variance of inflation would be driven to zero. Inflation would thus be fully stabilized.

However, from (17.88) and (17.90), real shocks would continue to affect deviations of real output and unemployment from their natural rates, even if ϕπ is driven to infinity.

Thus, the divine coincidence does not hold in this model. In the presence of real shocks, inflation stabilization does not result in unemployment and output stabilization, as there is always a trade-off between the stabilization of inflation and the stabilization of unemployment around its natural rate in the presence of real shocks.

17.8