Interest Rates

e l∩e rea an Interest rates are another important—and familiar—type of economic variable. An

nominal interest interest rate is a rate of return promised by a borrower to a lender.

If, for example,rates. the interest rate on a $100, one-year loan is 8%, the borrower has promised to repay the

lender $108 one year from now, or $8 interest plus repayment of the $100 borrowed.

As we discuss in more detail in Chapter 4, there are many different interest rates in the economy. Interest rates vary according to who is doing the borrowing, how long the funds are borrowed for, and other factors (see "In Touch with Data and Research: Interest Rates"). There are also many assets in the economy, such as shares of corporate stock, that do not pay a specified interest rate but do pay their

holders a return; for shares of stock, the return comes in the form of dividends and capital gains (increases in the stock's market price). The existence of so many different assets, each with its own rate of return, has the potential to complicate greatly the study of macroeconomics. Fortunately, however, most interest rates and other rates of return tend to move up and down together. For purposes of macroeconomic analysis we usually speak of "the" interest rate, as if there were only one. If we say that a certain policy causes "the" interest rate to rise, for example, we mean that interest rates and rates of return in general are likely to rise.

Real Versus Nominal Interest Rates. Interest rates and other rates of return share a measurement problem with nominal GDP: An interest rate indicates how quickly the nominal, or dollar, value of an interest-bearing asset increases over time, but it does not reveal how quickly the value of the asset changes in real, or purchasingpower, terms. Consider, for example, a savings account with an interest rate of 4% per year that has $300 in it at the beginning of the year.

At the end of the year the savings account is worth $312, which is a relatively good deal for the depositor if inflation is zero; with no inflation the price level is unchanged over the year, and $312 buys 4% more goods and services in real terms than the initial $300 did one year earlier. If inflation is 4% per year, however, what cost $300 one year earlier now costs $312, and in real terms the savings account is worth no more today than it was a year ago.To distinguish changes in the real value of assets from changes in nominal value, economists frequently use the concept of the real interest rate. The real interest rate (or real rate of return) on an asset is the rate at which the real value or purchasing power of the asset increases over time. We refer to conventionally measured interest rates, such as those reported in the media, as nominal interest rates, to distinguish them from real interest rates. The nominal interest rate (or nominal rate of return) is the rate at which the nominal value of an asset increases over time. The symbol for the nominal interest rate is i.

The real interest rate is related to the nominal interest rate and the inflation rate as follows:

real interest rate = nominal interest rate — inflation rate (2.13)

= i — π.

We derive and discuss Eq. (2.13) further at the end of the book in Appendix A, Section A.7.[31] For now, consider again the savings account paying 4% interest. If the inflation rate is zero, the real interest rate on that savings account is the 4% nominal interest rate minus the 0% inflation rate, which equals 4%. A 4% real interest rate on the account means that the depositor will be able to buy 4% more goods and services at the end of the year than at the beginning. But if inflation is 4%, the real interest rate on the savings account is the 4% nominal interest rate minus the 4% inflation rate, which equals 0%. In this case, the purchasing power of the account is no greater at the end of the year than at the beginning.

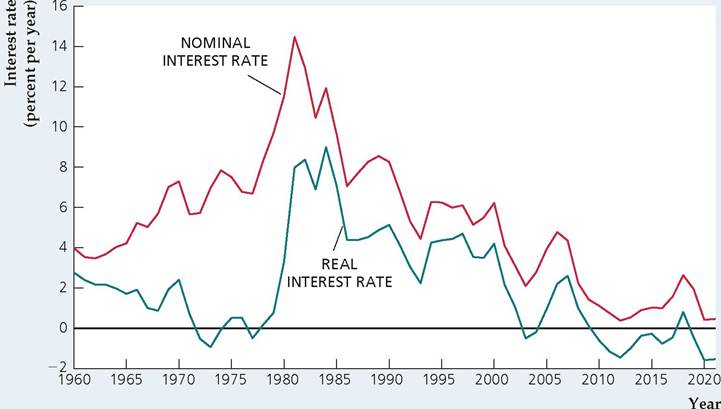

Nominal and real interest rates for the United States for 1960-2021 are shown in Figure 2.6.

The real interest rate was unusually low in the mid-1970s; indeed, it was negative, which means that the real values of interest-bearing assets actually were declining over time. Both nominal and real interest rates rose to record highs in the early 1980s before returning to more normal levels in the 1990s. But the real interest rate turned negative in the early 2000s and again beginning in 2010.FIGURE 2.6

Nominal and real interest rates in the United States, 1960-2021

The nominal interest rate shown is the interest rate on three-year Treasury securities. The real interest rate is measured as the nominal interest rate minus the average inflation rate (using the GDP deflator) over the current and subsequent two years. The real interest rate was unusually low (actually negative) in the mid-1970s. In the early 1980s, both the nominal and real interest rates were very high. Nominal and real interest rates returned to more normal levels in the 1990s and then fell sharply, with real interest rates becoming negative again in the early 2000s and 2010s.

Source: The implicit price deflator for GDP is the same as for Fig. 2.4. Inflation rates for 2022 and 2023 are assumed to be 2%. The nominal interest rate on three-year Treasury securities is from the Board of Governors of the Federal Reserve System, Statistical Release H15, Wwwfederalreserve.gov/releases.

The Expected Real Interest Rate. When you borrow, lend, or make a bank deposit, the nominal interest rate is specified in advance. But what about the real interest rate? For any nominal interest rate, Eq. (2.13) states that the real interest rate depends on the rate of inflation over the period of the loan or deposit—say, one year. However, the rate of inflation during the year generally can't be determined until the year is over. Thus, at the time that a loan or deposit is made, the real interest rate that will be received is uncertain.

Because borrowers, lenders, and depositors don't know what the actual real interest rate will be, they must make their decisions about how much to borrow, lend, or deposit on the basis of the real interest rate they expect to prevail. They know the nominal interest rate in advance, so the real interest rate they expect depends on what they think inflation will be. The expected real interest rate is the nominal interest rate minus the expected rate of inflation, or

where r is the expected real interest rate and πe is the expected rate of inflation.

Comparing Eqs. (2.13) and (2.14), you can see that if people are correct in their expectations—so that expected inflation and actual inflation turn out to be the same—the expected real interest rate and the real interest rate actually received will be the same.

The expected real interest rate is the correct interest rate to use for studying most types of economic decisions, such as people's decisions about how much to borrow or lend. However, a problem in measuring the expected real interest rate is that economists generally don't know exactly what the public's expected rate of inflation is. Economists use various means to measure expected inflation. One approach is to survey the public and simply ask what rate of inflation people expect. A second method is to assume that the public's expectations of inflation are the same as publicly announced government or private forecasts. A third possibility is to assume that people's inflation expectations are an extrapolation of recently observed rates of inflation. Unfortunately, none of these methods is perfect, so the measurement of the expected real interest rate always contains some error.

►