Labor Contracts and Nominal-Wage Rigidity

In the Keynesian theory, the nonneutrality of money is a consequence of nominal rigidity. In this chapter we emphasized nominal-price rigidity. An alternative nominal rigidity that could account for the nonneutrality of money, which many Keynesians emphasize, is nominal-wage rigidity.

Nominal-wage rigidity could reflect long-term labor contracts between firms and unions in which wages are set in nominal terms (the case we study here). In terms of the AD-AS framework the difference between nominal-price rigidity and nominal-wage rigidity is that nominal- price rigidity implies a horizontal short-run aggregate supply curve, whereas nominal-wage rigidity implies a short-run aggregate supply curve that slopes upward. However, this difference doesn't really affect the results obtained from the Keynesian model. In particular, in the Keynesian model with nominal-wage rigidity, money remains nonneutral in the short run and neutral in the long run.The Short-Run Aggregate Supply Curve with Labor Contracts

In the United States most labor contracts specify employment conditions and nominal wages for a period of three to five years. Although labor contracts specify the nominal wage rate, they usually don't specify the total amount of employment. Instead, employers unilaterally decide how many hours will be worked and whether workers will be laid off. These factors imply that the short-run aggregate supply curve slopes upward.

We can see why the short-run aggregate supply curve slopes upward when labor contracts prespecify the nominal wage by considering what happens when the price level increases. With the nominal wage, W, already determined by the contract, an increase in the price level, P, reduces the real wage, w, or W/P. In response to the drop in the real wage, firms demand more labor. Because firms unilaterally choose the level of employment, the increase in the amount of labor demanded leads to an increase in employment and therefore an increase in output.

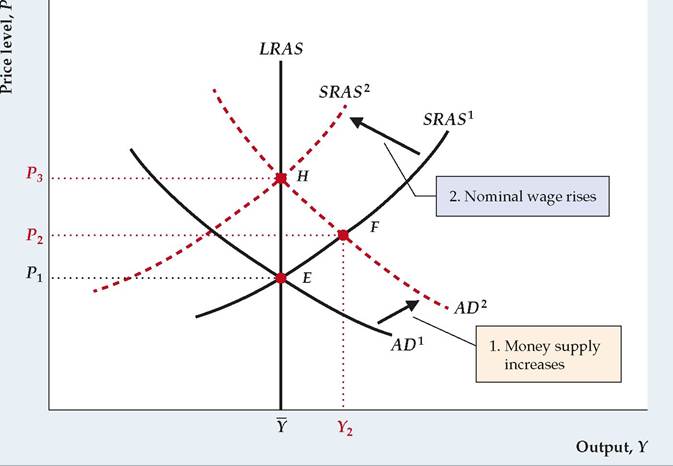

Thus an increase in the price level leads to an increase in the amount of output supplied, as shown by the SRAS curves in Figure 11.A.1.Nonneutrality of Money

Money is nonneutral in the short run in the model with long-term labor contracts, as illustrated in Fig. 11.A.1. The initial general equilibrium is at point E, where the initial aggregate demand curve, AD1, intersects the short-run aggregate supply curve, SRAS1. A 10% increase in the money supply shifts the AD curve up to AD2. (For any level of output the price level is 10% higher on AD2 than on AD1.) In the short run, the increase in the money supply raises the price level to P2 and

FIGUREJ1.A.1

Monetary nonneutrality with long-term contracts

With labor contracts that fix the nominal wage in the short run, an increase in the price level lowers the real wage and induces firms to employ more labor and produce more output. Thus the short-run aggregate supply curve SRAS1 slopes upward. When nominal wages are rigid, money isn't neutral. From the initial equilibrium point, E, a 10% increase in the money supply shifts the AD curve up, from AD1 to AD 2. In the short run, both output and the price level increase, as shown by point F. Over time, contracts are renegotiated and nominal wages rise to match the increase in prices. As wages rise, the short-run aggregate supply curve shifts up, from SRAS1 to SRAS 2, so that general equilibrium is restored at H. At H both the price level, P, and the nominal wage, W, have risen by 10%, so the real wage is the same as it was initially, and firms supply the fullemployment level of output, Y.

output to Y2 at point F. Output at F is higher than its full-employment level because the rise in prices lowers the real wage, which leads firms to employ more labor and produce more output.

At the short-run equilibrium point, F, however, workers will be dissatisfied because their real wages are lower than they had expected. Over time, as contracts are renewed or renegotiated, nominal wages will rise to offset the increase in prices. At any price level, a rise in the nominal wage also raises the real wage, inducing firms to employ less labor and produce less output. Thus rising nominal wages cause the short-run aggregate supply curve to shift up and to the left, from SRAS1 to SRAS 2. Eventually, general equilibrium is restored at point H.

In the long run at point H, the price level rises to P3, which is 10% higher than its initial value, P1. At H the nominal wage, W, has also increased by 10% so that the real wage, W/P, has returned to its initial value. With the real wage back at its original value, firms employ the same amount of labor and produce the same amount of output (Y) as they did at the initial equilibrium point, E. Thus as in the Keynesian model based on efficiency wages and price stickiness, in the Keynesian model with nominal-wage rigidity, money is neutral in the long run but not in the short run.

Although nominal-wage rigidity arising from labor contracts can explain short-run monetary nonneutrality, some economists object to this explanation. One objection is that about one-ninth of workers in the United States are unionized and covered by long-term labor contracts. However, many nonunion workers receive wages similar to those set in union contracts. For example, although most nonunion workers don't have formal wage contracts, they may have "implicit contracts" with their employers, or informal unwritten arrangements for comparable wages.

A second objection is that many labor contracts contain cost-of-living adjustments (COLAs), which tie the nominal wage to the overall price level, as measured, for example, by the consumer price index. Contracts with complete indexation increase the nominal wage by the same percentage as the increase in the price level.

If wages are completely indexed to the price level, the short-run aggregate supply curve is vertical and money is neutral. To show why, let's suppose that the price level increases by 6%. If labor contracts are completely indexed, nominal wages also increase by 6% and the real wage, W/P, remains unchanged. Because the real wage doesn't change, firms choose the same levels of employment and output independent of the price level.However, in most U.S. labor contracts, wages aren't completely indexed to prices. For example, under a contract that calls for 50% indexation, the nominal wage will increase by 50% of the overall rate of increase in prices. Thus if the price level increases by 6%, the nominal wage increases by 3%. As a result, the real wage falls by 3% (a 3% increase in the nominal wage, W, minus a 6% increase in the price level, P). The reduction in the real wage induces firms to increase employment and production. Thus with partial indexation the short-run aggregate supply curve again slopes upward, and money isn't neutral in the short run.

A third and final objection is that this theory predicts that real wages will be countercyclical, contrary to the business cycle fact that real wages are procyclical. For example, at point F in Fig. 11.A.1, output is higher than the full-employment level, but the real wage is lower than at full employment (indeed, the low real wage induces firms to produce the extra output). Thus the theory holds that real wages will fall in booms—that is, the real wage is countercyclical—which is inconsistent with the evidence.

However, perhaps both supply shocks and aggregate demand shocks affect real wages. For the real business cycle theory we showed that, if productivity shocks cause cyclical fluctuations, the real wage should be procyclical, perhaps strongly so. A combination of supply shocks (which cause the real wage to move procyclically) and aggregate demand shocks (which, as in Fig. 11.A.1, cause the real wage to move countercyclically) might average out to a real wage that is at least mildly procyclical. Some evidence for this view was provided in a study by Scott Sumner of Bentley College and Stephen Silver[CCX] of Virginia Military Institute, which shows that the real wage has been procyclical during periods dominated by supply shocks but has been countercyclical during periods in which aggregate demand shocks were more important.