Money Growth, Seigniorage, and Inflation

If the growth rate of the money supply eventually translates into higher inflation, why don’t governments and central banks keep the growth rate of the money supply low and stable to tackle the problem of inflation?

The answer is that governments often have other policy motives besides tackling inflation.

Perhaps the most important incentive for the issuance of new money by governments is to finance expenditure that they cannot (or do not wish to) finance through other methods, such as higher taxes or higher government debt.The main cause of all episodes of high inflation or hyperinflation appears to have been the need of governments to use revenue from money creation (seigniorage) to finance wars and war reparations, revolutions, extraordinary costs related to natural disasters, or sudden reductions in their capacity to borrow from financial markets or to raise revenue from taxes and customs revenues.

In this section, we explore the relationship between the growth rate of the money supply, inflation, and the needs of governments to raise revenue through seigniorage. We examine both the case in which the required income from seigniorage can be raised on the balanced growth path (which results in sustained high inflation), and the case in which the required revenue from seigniorage is so high that it cannot be raised on the balanced growth path. In the latter case, the economy is driven into hyperinflation.

The generally accepted definition of hyperinflation is due to Cagan [1956]. Cagan [1956, p. 25] defined a period of hyperinflation as one “beginning in the month in which the rise in prices exceeds 50% and as ending in the month before the monthly rise in prices drops below that amount and stays below for at least a year.”

The first modern periods of hyperinflation occurred in Europe in the aftermath of World War I, as well as during and in the aftermath of World War II.

In the past 40 years, very high inflation rates and hyperinflation reappeared in some Latin American countries, some transition economies after the collapse of the Soviet Union, and in some war-torn countries in Asia and Africa. Moreover, without reaching hyperinflation, many countries have experienced high inflation (from 100% to 1,000% per year) for quite long periods.14

12.9.1 Relations between Monetary Growth, Seigniorage, and Inflation

To study the relation between the rate of growth of the money supply, inflation and revenue from seigniorage, we start from the general money demand function (12.2). In equilibrium, the demand for money equals the supply of money, so it follows that

To simplify matters, let us use a linear logarithmic form of the money demand function m:

where κ is a constant, e is the base of natural logarithms, and η > 0 is the semi-elasticity of money demand with respect to the nominal interest rate i.

The nominal interest rate is defined by the Fisher equation

where r is the real interest rate, and πe is expected inflation.

Real output Y is considered exogenous and is assumed to grow at a rate g + n > 0. The rate of growth of the nominal money supply M is equal to μ > 0.

Under these assumptions, inflation on the balanced growth path is determined by

Assuming rational expectations, we can substitute (12.79) in (12.78) and the resulting equation in (12.77). The money demand function can thus be written as

To further simplify matters, assume that the golden rule applies on the balanced growth path, which implies that r = g + n.

Under this additional assumption, (12.80) simplifies to

Because of the golden rule, the nominal interest rate is equal to the rate of growth of the money supply μ.15

We can now define seigniorage revenue S. This is equal to the real resources that the government commands by issuing additional money, and buying goods and services. Seigniorage is thus given by

where S denotes total seigniorage revenue from money creation. The money demand equation (12.81) has been substituted in the right-hand side of (12.82).

As a proportion of total output, seigniorage revenue is defined by

where s is seigniorage revenue relative to total output.

Taking the first derivative of (12.83) with respect to μ, we can see how the seigniorage to output ratio depends on the growth rate of the money supply:

Equation (12.84) is positive for as long as the growth rate of the money supply μ is smaller than 1/η. When μ exceeds 1/η, the change in seigniorage revenue as a proportion of total output becomes negative when μ increases further. For μ > 1/η, a further increase in the growth rate of the money supply has a negative effect on government revenue from money creation. This happens because the reduction in real money holdings by household and firms, which is the basis of this revenue, is greater than the rise in μ.

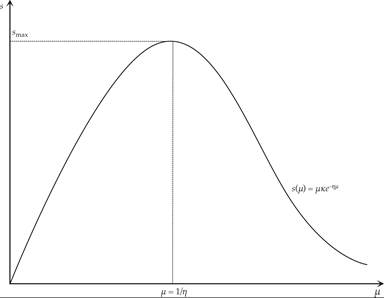

12.9.2 The Seigniorage Laffer Curve

Figure 12.8 depicts the revenue from seigniorage as a percentage of total output, as a function of the growth rate of the money supply.

As can be seen from the figure, the revenue from money creation is characterized by a Laffer curve, because up to a point, the rise in the growth rate of the money supply increases revenues from seigniorage as a percentage of output, but after that point, it begins to reduce them, because the reduction in real money demand exceeds the rise in the rate of growth of the money supply.16

Figure 12.8 The seigniorage Laffer curve.

It is interesting to calculate the percentage of total output at which seigniorage revenue is maximized. The maximum seigniorage revenue smax that can be extracted occurs when μ = 1/η. From (12.83), it follows that

alt=pg368-1.png>

Using annual data, Cagan [1956] estimated that η lies between 1/2 and 1/3. Consequently, he estimated the growth rate of the money supply that maximizes revenues from seigniorage as a percentage of total output (and the corresponding inflation) as between 200% and 300% per year. Assuming that κ = 0.10 in (12.81), the maximum revenue from seigniorage as a percentage of total output is between 7 and 11%. For the period 1975–1985, Sachs and Larrain [1993] estimated actual revenue from seigniorage at about 5–6.5% for high inflation countries, such as Italy, Bolivia, Turkey, and Peru, and much lower for a series of other countries.

12.9.3 The Demand for Seigniorage and Equilibrium with High Inflation

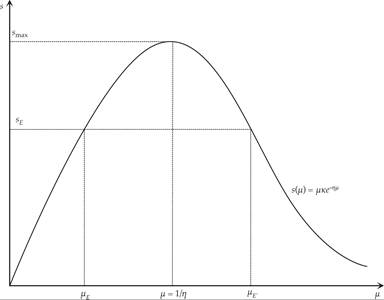

Let us now consider a government that needs to fund a proportion of its public spending through seigniorage. Assume that this financing requirement, as a proportion of total output, is equal to sE, which is less than the maximum seigniorage smax that the government can achieve by setting the growth rate of the money supply at μ = 1/η. The equilibrium is depicted in figure 12.9. There are two options to achieve revenue equal to sE.

One is with a growth rate of the money supply μE < 1/η, and the other is with a growth rate of the money supply μE′ > 1/η. Assume that the government dislikes inflation and therefore chooses the lowest growth rate of the money supply that is compatible with the objective of raising revenue sE from seigniorage.

Figure 12.9 Equilibrium with high inflation.

For as long as the government needs to raise revenue equal to a proportion sE of its output through seigniorage, the economy is trapped in an equilibrium with a growth rate of the money supply equal to μE and the corresponding high inflation rate. For example, if the government wants to raise seigniorage corresponding to 6% of total output, assuming η = 1/2, then the annual growth rate of the money supply (and corresponding steady state inflation) is equal to about 100%.

12.9.4 The Transition to Hyperinflation

But how can hyperinflation arise? Unlike high inflation, hyperinflation is a disequilibrium phenomenon. It arises when a government tries to raise seigniorage that exceeds the maximum that can be raised in the steady state.

Let us assume that a government needs to raise seigniorage that, as a proportion of total output, is higher than the maximum that can be raised in the steady state. We assume sE > smax. Obviously, there can be no balanced growth path in which the government can raise revenues from seigniorage that exceeds smax. However, for a time, and as the economy adjusts toward the balanced growth path, the government may be able to raise seigniorage revenues greater than smax. For example, this could happen if there is gradual adjustment in the demand for money or gradual adjustment in inflationary expectations.

Assume that the demand for money does not adjust immediately to its steady state level after a change in the nominal interest rate, but only gradually.

Thus, when the nominal interest rate increases, money demand is temporarily higher than in the steady state. In this case, during the adjustment, the monetary base on which the inflationary tax is imposed is higher than the steady state monetary base. Consequently, during the adjustment, as μ increases, seigniorage revenues will exceed smax temporarily, because real money balances are higher than on the balanced growth path. As the demand for money decreases gradually, the government should constantly increase the rate of monetary growth and the consequent inflation, to ensure the required high revenues from seigniorage. This can lead to an explosive path for the growth rate of the money supply and result in hyperinflation.Let us then assume that (12.81) defines the steady state money demand function and that actual money demand adapts to its steady state level only gradually. We shall continue to assume that real output and the real interest rate are on their exogenous balanced growth paths. From (12.81), the steady state money demand as a percentage of total output m* depends negatively on the growth rate of the money supply:

In the short run, real money demand is assumed to adjust gradually toward its steady state value according to

where 0 < ψ < 1/η.

The concept behind the assumed gradual adjustment is that it is difficult for economic agents to adapt their habits regarding the financing of their transactions or to use alternative means of payment in the short run. Hence, the demand for real money balances adjusts gradually over time. The particular log-linear functional form is chosen for convenience. The parameter ψ, which measures the speed of adjustment, is assumed to be positive but less than 1/η. We thus assume that adjustment is positive but not too fast.

Substituting (12.85) in (12.86) yields

This describes the evolution of the short-run demand for money. Note that in (12.87), the growth rate of the money supply μ depends on time.

Let us now turn to the government’s financing needs. Assume that the government needs revenues from seigniorage that may exceed the maximum that can be raised on the balanced growth path (i.e., sE > smax). Although such revenues cannot be raised on the balanced growth path, they can be raised along the adjustment path (i.e., before money demand has fully adjusted to its steady state level). We shall see that if indeed sE > smax, then this requires an ever-increasing rate of growth in the money supply and ever-increasing inflation.

For the government to achieve its seigniorage target sE, the following relation must hold continuously:

Equation (12.88) with a constant sE implies that

Equation (12.89) can be written as

This suggests that to keep revenues from seigniorage constant as a percentage of total income at the level sE, the growth rate of the money supply must keep increasing continuously, at the same rate as the decline of real money demand relative to output. Substituting (12.90) and (12.88) in (12.87), we get

From the differential equation (12.91), for the growth rate of the money supply to be eventually stabilized, a necessary and sufficient condition is

If sE > smax, then the right-hand side of (12.91) is positive for all rates of growth of the money supply. Taking the first derivative of (12.91) with respect to μ(t), we can see that after a point, a higher growth rate of the money supply leads to a higher rate of change in the growth of the money supply. This results in an explosive path for the growth rate of the money supply and inflation.

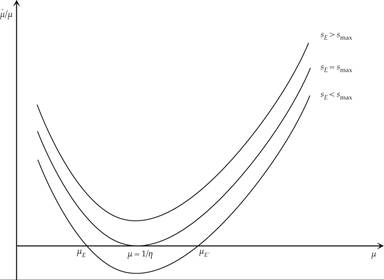

The relationship between the percentage change in the growth rate of the money supply and the rate of change in the money supply provided from (12.91), for different financing requirements from seigniorage, is depicted in figure 12.10.

Figure 12.10 Equilibria with high inflation and the transition to hyperinflation.

When the financing needs of the government from seigniorage are less than or equal to the maximum possible on the balanced growth path, then the growth rate of the money supply is eventually stabilized at a equilibrium rate that may indeed be high, but inflation does not continue evolving into hyperinflation.

However, if the financing needs of government exceed the maximum that is sustainable on the balanced growth path, then, as the government tries to raise the necessary revenue from seigniorage, the growth rate of the money supply gradually accelerates to keep up with the declining monetary base, and the economy falls into a state of hyperinflation. Inflation gradually reduces the demand for money relative to total output, and the government needs an ever-increasing growth rate of the money supply to be able to collect the needed seigniorage revenue.

Our analysis of the link between the needs of a government to raise seigniorage to finance government expenditure and the rate of growth of the money supply can thus help explain episodes of high inflation and even hyperinflation.

12.9.5 How Can High Inflation and Hyperinflation Be Tackled?

Our basic analysis explains why, in many cases, inflation may be driven to very high levels. This is due to the inability of a government to finance its spending from other revenue sources, such as taxation or borrowing from the markets, and its need to use seigniorage (i.e., revenue from money creation).

The analysis also explains why, even though inflation may reach very high levels, it might not evolve into hyperinflation. For hyperinflation to happen, the financing needs of the government must be so high that they exceed the maximum level that can be financed through seigniorage on the balanced growth path.

Finally, the analysis emphasizes the central role of fiscal problems as the main causes of both high inflation and hyperinflation. A significant precondition for tackling high equilibrium inflation rates or hyperinflation is to pursue reforms that address the underlying fiscal problems (Sargent [1982]).

12.10