Nominal Interest Rates and Short-Run Equilibrium in the Money Market

Equilibrium in the money market means that the existing money supply is willingly held by households and firms. Thus, the equilibrium condition in the money market is for the money supply to be equal to money demand:

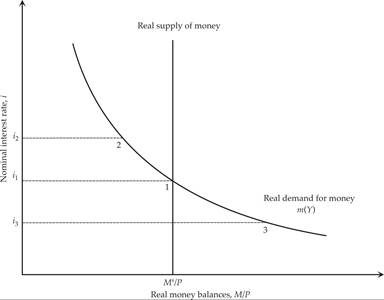

Short-run equilibrium in the money market is depicted in figure 12.3.

It is assumed that the central bank controls the money supply and fixes it at some constant level, and that aggregate real income and the price level are given. Therefore, in the short run, the only variable that can adjust to equilibrate the money market is the nominal interest rate. The money market equilibrates at the nominal interest rate at which, for given aggregate real income and the price level, the demand for money becomes equal to the supply of money by the central bank.

Figure 12.3 Short-run equilibrium in the money market.

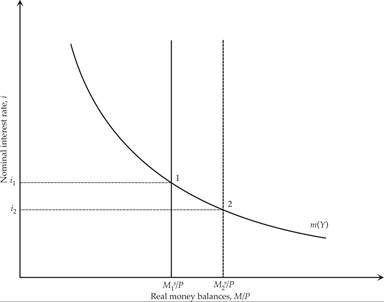

As shown in figure 12.4, an increase in the money supply causes a reduction in the nominal interest rate, because an increase in the money supply creates excess liquidity in the domestic money market. Households and firms shift this excess liquidity to interest-bearing assets, raising their prices and reducing their yield. This reduces the level of nominal interest rates. In the new equilibrium, given the price level and real income, households and firms voluntarily hold the increased supply of money, as the opportunity cost of holding money (i.e., the nominal interest rate) has fallen.

Figure 12.4 The short-run effects of a rise in the money supply: the liquidity effect.

The negative short-term effect of the money supply on the level of nominal interest rates is often referred to as the liquidity effect.

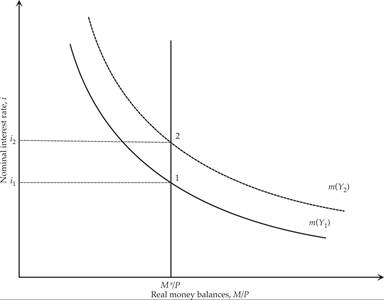

The more liquidity the central bank injects into the money market in the form of increasing the money supply, the lower the nominal interest rate will be. Conversely, a decrease in the money supply would reduce liquidity and cause an increase in the nominal interest rate.Figure 12.5 shows the impact of an increase in money demand. This can be either autonomous (increased demand for liquidity on the part of households and firms) or due to an increase in real income. The latter case is the one shown in figure 12.5.

Figure 12.5 The short-run effects of an exogenous rise in real income.

An increase in real income from Y1 to Y2 raises money demand because of the increase in transactions that have to be financed. Given the money supply and the price level, this creates an excess demand for money for transaction purposes. As households and firms try to move out of interest-yielding assets by liquidating them (to acquire greater liquidity for transaction purposes), the prices of these assets fall, leading to higher nominal interest rates. The money market will equilibrate at higher nominal interest rates, which will reduce the excess demand for money arising from the increased transactions.

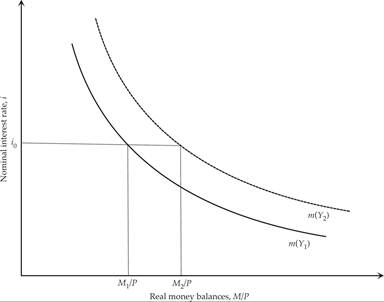

Similar effects also apply to the case of an autonomous increase in the price level or an autonomous increase in liquidity preference by households and firms. Given the nominal money supply, an autonomous increase in the price level reduces real money balances, requiring an increase in the nominal interest rate for money demand to adjust to the lower supply of real money balances. The same would apply if liquidity preference by households or firms increased, say, because of a shift in preferences or an increase in uncertainty.

Finally, suppose that the central bank follows a policy of pegging the nominal interest rate rather than fixing the money supply. The central bank stabilizes the nominal interest rate at the level i0, by committing to lend (supply) any quantity of money demanded at this nominal interest rate. In this case, the money supply in the economy is determined by money demand. An increase in the price level or real income (or liquidity preference) causes an increase in the money supply, because the central bank is prepared to provide unlimited liquidity at the nominal interest rate i0. As shown in figure 12.6, when the central bank follows a policy of stabilization of the nominal interest rate, an increase in money demand automatically leads to a higher money supply and vice versa.

Figure 12.6 Equilibrium in the money market with interest rate pegging.

12.5