The Demand for Money

The demand for money by households and firms depends on three main factors. The first factor is the price level. The higher the level of prices is, the higher will be the amount of money that households and firms want to hold for their current and future transactions.

For example, if the price level were to double, then for a household or a firm to buy the same amount of goods and services would require twice as much money. The demand for money is thus usually assumed to be proportional to the price level.The second factor is the volume of transactions. When the volume of transactions, usually measured by aggregate real output, increases, households and firms will need more money to carry out their increased transactions.

The third factor is the level of interest rates. Banknotes pay no interest. Demand deposits and current (checking) accounts, even when they pay interest, pay a very low rate compared to the yields of less-liquid assets, such as time deposits, treasury bills, or bonds. As interest rates rise, households and firms want to hold a smaller part of their assets in low- (or zero-) yielding money, in relation to assets that pay interest. Consequently, the demand for money will depend negatively on the nominal interest rate, as the nominal interest rate measures the opportunity cost of holding money.

The money demand function is usually expressed as

where Md denotes nominal money demand, P is the price level, Y is real aggregate income (GDP), i is the nominal interest rate, and m is a function increasing in real aggregate income and decreasing in the nominal interest rate. The demand for money is assumed to be proportional to the price level, in the sense that an increase in the price level requires an increase in the quantity of money by the same proportion to carry out the same volume of transactions.

Thus the demand for money is a demand for real money balances, that is, a given amount of purchasing power or liquidity.5Assuming that the demand for money function has a unitary elasticity with respect to real aggregate income, it takes the form of the quantity theory equation

where κ is a decreasing function of the nominal interest rate. The quantity theory equation is a special case of (12.4), in which the demand for real money balances is proportional to aggregate real income.6

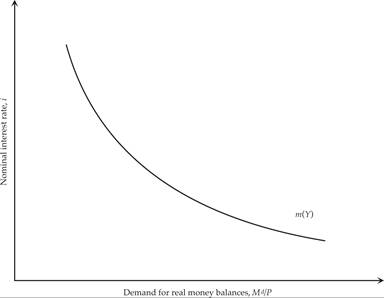

The demand for real money balances as a function of the nominal interest rate is depicted in figure 12.1. The relationship between real money demand and the nominal interest rate is negative, because holding money becomes more expensive as interest rates rise (recall that money does not pay interest). Therefore, households and firms reduce the amount of money holdings and increase holdings of securities and other interest-yielding assets.

Figure 12.1 The demand for money and the nominal interest rate.

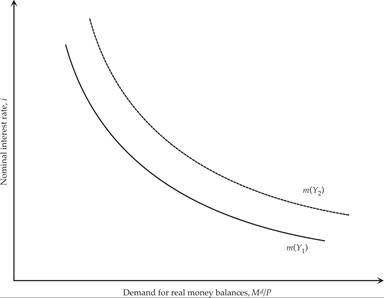

The position of the money demand function in figure 12.1 depends on the level of real income, which determines the volume of transactions in goods and services. For given nominal interest rates, an increase in real income will increase the demand for money as it will increase the amount of money required by households and firms to carry out their increased transactions. The money demand curve will move to the right, as shown in figure 12.2.

Figure 12.2 An increase in real income and the demand for money.

A similar shift may occur if there is an exogenous increase in liquidity preference on the part of households and firms.

For example, because of increased uncertainty or any other reason, if households and firms desire to hold more money for a given real income and nominal interest rate, then the demand for money will shift to the right, as in the case of an increase in real income depicted in figure 12.2.As already mentioned, households and firms hold money because of the liquidity it provides. How much money households and firms wish to hold depends proportionately on the price level. The demand for money is not a demand for a certain amount of nominal money but for a certain amount of purchasing power. This demand depends positively on the volume of economic transactions (as measured by aggregate real income) and negatively on the opportunity cost of holding money (as measured by the nominal interest rate). These three factors—the price level, the volume of economic transactions as measured by aggregate output and income) and the nominal interest rate—are the factors that affect the demand for money.

12.4

More on the topic The Demand for Money:

- The existence of money in a modern economy is usually taken for granted.

- Asset Market Equilibrium

- Money Growth and Inflation

- The Post-Keynesian Approach

- Article 6.8 Great Portland strikes with convertible bond

- Dynamics and the Business Cycle

- Zimbabwe Village Savings and Loan Associations

- SIMILARITIES BETWEEN CONFLICT RESOLUTION AND HUMAN RIGHTS

- Chapter 8 The Cossacks

- The golden age of gentlemanly imperialism in China: changing perspectives and changing realities