Physical and Human Capital with Imperfect Labor Markets

In this section, I analyze the implications of labor market frictions that lead to factor prices different from the ones used so far (in particular, in terms of the model of the last section, deviating from the competitive pricing formulea (10.32)).

The literature on labor market imperfections is vast and my purpose here is not to provide an overview. For this reason, I adopt the simplest representation. In particular, imagine that the economy is identical to that described in the previous section, except that there is a measure 1 of firms as well as a measure 1 of individuals at any point in time, and each firm can only hire one worker. The production function of each firm is still given bywhere yj (t) refers to the output of firm j, kj (t) is its capital stock (equivalently capital per worker, since the firm is hiring only one worker), and hi (t) is the human capital of worker i that the firm has matched with. This production function again satisfies Assumptions 1 and 2. The main departure from the models analyzed so far is the structure for the labor market, which is summarized next.

(1) Firms choose their physical capital level irreversibly (incurring the cost R (t) kj (t), where R(t) is the market rate of return on capital), and simultaneously workers choose their human capital level irreversibly.

(2) After workers complete their human capital investments, they are randomly matched with firms. Random matching here implies that high human capital workers are not more likely to be matched with high physical capital firms.

(3) After matching, each worker-firm pair bargains over the division of output between themselves. We assume that they simply divide the output according to some prespecified rule, and the worker receives total earnings of

for some λ ∈ (0,1).

This is admittedly a very simple and reduced-form specification. Nevertheless, it will be sufficient to emphasize the main economic issues. A more detailed game-theoretic justification for a closely related environment is provided in Acemoglu (1996).

Let us also introduce heterogeneity in the cost of human capital acquisition by modifying

where ai differs across dynasties (individuals). A high-value of ai naturally corresponds to an individual who can more effectively accumulate human capital.

An equilibrium is defined similarly except that factor prices are no longer determined by (10.32). Let us start the analysis with the physical capital choices of firms. At the time each firm chooses its physical capital it is unsure about the human capital of the worker he will be facing. Therefore, the expected return of firm j can be written as

This expression takes into account that the firm will receive a fraction 1 — λ of the output produced jointly by itself and by the worker that it is matched with. The integration takes care of the fact that the firm does not know which worker it will be matched with and thus we are taking the expectation of F (kj (t),hi (t)) over all possible human capital levels available in the market (given by The last term is the cost of making irreversible capital

The last term is the cost of making irreversible capital

investment at the market price R (t). This investment is made before the firm knows which worker it will be matched with. The important observation is that the ob jective function in (10.39) is strict concave in kj (t) given the strict concavity of F (∙, ∙) from Assumption 1.

Proposition 10.3.

In the open economy version of the model described here, there exists a unique positive level of capital per worker k given by (IO.4O) such that the equilibrium

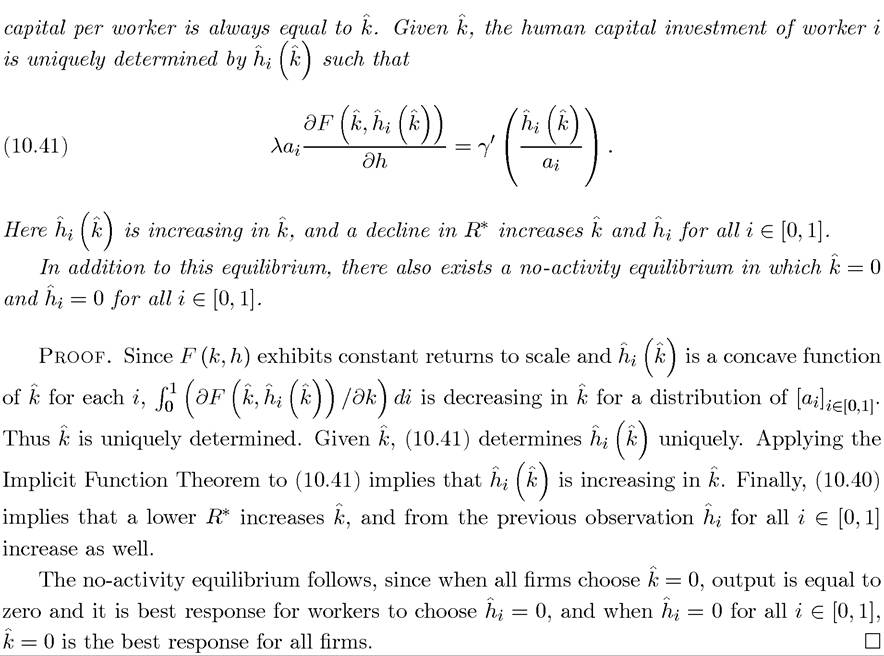

Observe that there is underinvestment both in human capital and physical capital (this refers to the positive activity equilibrium; clearly, there is even a more severe underinvestment in the no-activity equilibrium). Consider a social planner wishing to maximize output (or one who could transfer resources across individuals in a lump-sum fashion). Suppose that the social planner is restricted by the same random matching technology, so that she cannot allocate workers to firms as she wishes. A similar analysis to above implies that the social planner would also like each firm to choose an identical level of capital per firm, say k. However, this level of capital per firm will be different than in the competitive equilibrium and she will also choose a different relationship between human capital and physical capital investments. In particular, given k, she would make human capital decisions to satisfy

which is similar to (10.41), except that λ is absent from the left-hand side. This is because each worker takes into account only his share of output, λ, when undertaking his human capital investment decisions, while the social planner considers the entire output. Consequently, as long as λ < 1,

412

id="Picutre 1245" class="lazyload" data-src="/files/uch_group77/uch_pgroup317/uch_uch7365/image/image1244.jpg">

Proposition 10.4. In the equilibrium described in Proposition 10.3, there is underinvestment both in physical and human capital.

More interesting than the underinvestment result is the imbalance in the physical to human capital ratio of the economy, which did not feature in the previous two environments we discussed.

The following proposition summarizes this imbalance result in a sharp way:

Proof. See Exercise 10.20.

they do not take these external effects into consideration. Pecuniary external effects are also present in competitive markets (since, for example, supply affects price), but these are typically “second order,” because prices are such that they are equal to both the marginal benefit of buyers (marginal product of firms in the case of factors of production) and to the marginal cost of suppliers. The presence of labor market frictions causes a departure from this type of marginal pricing and is the reason why pecuniary externalities are not second order.

Perhaps even more interesting is the fact that pecuniary externalities in this model take the form of human capital externalities, meaning that greater human capital investments by a group of workers increase other workers’ wages. Notice that in competitive markets (without externalities) this does not happen. For example, in the economy analyzed in the last section, if a group of workers increase their human capital investments, this would depress the physical to human capital ratio in the economy, reducing wages per unit of human capital and thus the earnings of the rest of the workers. Interestingly, the opposite may happen in the presence of labor market imperfections. To illustrate this point, let us suppose that there are two types of workers, a fraction of workers χ with ability ai and 1 — χ with ability a2 < a i. Using this specific structure, the first-order condition of firms, (10.40), can be written as

while the first-order conditions for human capital investments for the two types of workers take the form

group of workers have increased the earnings of the remaining workers. In fact, human cap

Proposition 10.3 that there exists a unique equilibrium with positive activity. This discussion is summarized in the following result:

Proposition 10.6. The positive activity equilibrium described in Proposition 10.3 exhibits human capital externalities in the sense that an increase in the human capital investments of a group of workers raises the earnings of the remaining workers.

10.7.