Problem Formulation

Let us now consider a discrete-time infinite-horizon economy and suppose that the economy admits a representative household. In particular, once again ignoring uncertainty, the representative household has the t = 0 objective function

with a discount factor of β ∈ (0,1).

In continuous time, this utility function of the representative household becomes

where p > 0 is now the discount rate of the individuals.

Where does the exponential form of the discounting in (5.16) come from? Discounting in the discrete-time case was already referred to as “exponential”, so the link should be apparent. To see it more precisely, imagine we are trying to calculate the value of $1 in T periods, and divide the interval [0,T] into T∕∆t equally-sized subintervals. Let the interest rate in each subinterval be equal to r∆t. It is important that the quantity r is multiplied by ∆t, otherwise as we vary ∆t, we would be changing the interest rate. Using the standard compound interest rate formula, the value of $1 in T periods at this interest rate is given by

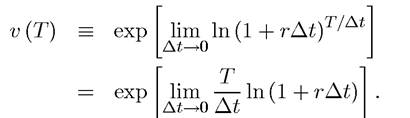

Next, let us approach the continuous time limit by letting ∆t → 0 to obtain

Since the limit operator is continuous,

However, the term in square brackets has a limit of the form 0/0 (or of the form ∞ ? 0). Let us next write this as

where the first equality follows from L’Hospital’s Rule (Theorem A.22 in Appendix Chapter A). Therefore,

Conversely, $1 in T periods from now, is worth exp (-rT) today. The same reasoning applies to discounting utility, so the utility of consuming c (t) in period t evaluated at time t = 0 is exp(-ρt) u (c (t)), where ρ denotes the (subjective) discount rate.

5.6.