Stationary Dynamic Programming Theorems

Let us start with a number of assumptions on Problem A1. Since these assumptions are only relevant for this section, I number them separately from the main assumptions used throughout the book.

Consider first a sequence {x* (t)}∞=0 ∈ X∞ which attains the supremum in Problem A1. Our main purpose is to ensure that this sequence will satisfy the recursive equation of dynamic programming, written here as by substituting in for the sequence (instead of the “max” operator),

(instead of the “max” operator),

and that any solution to (6.2) will also be a solution to Problem A1, in the sense that it will attain its supremum. In other words, we are interested in establishing equivalence results between the solutions to Problem A1 and Problem A2.

To prepare for these results, let us define the set of feasible sequences or plans starting with an initial value x (t) as:

Intuitively, Φ(x (t)) is the set of feasible choices of vectors starting from x (t). Let us denote a typical element of the set Our first assumption

Our first assumption

is:

This assumption is stronger than what is necessary to establish the results that will follow. In particular, for much of the theory of dynamic programming, it is sufficient that the limit in Assumption 6.1 exists. However, in economic applications, we are not interested in optimization problems where households or firms achieve infinite value. This is for two obvious

208

reasons.

First, when some agents can achieve infinite value, the mathematical problems are typically not well defined. Second, the essence of economics, tradeoffs in the face of scarcity, would be absent in these cases. In cases, where households can achieve infinite value, economic analysis is still possible, by using methods sometimes called “overtaking criteria,” whereby different sequences that give infinite utility are compared by looking at whether one of them gives higher utility than the other one at each date after some finite threshold. None of the models in this book require these more general optimality concepts.

This assumption is also natural. We need to impose that G (x) is compact-valued, since optimization problems with choices from non-compact sets are not well behaved (see Appendix Chapter A). In addition, the assumption that U is continuous leads to little loss of generality for most economic applications. In all the models we will encounter in this book, U will be continuous. The most restrictive assumption here is that the state variable lies in a compact set—that X is compact. Most results in this chapter can be generalized to the case in which X is not compact, though this requires additional notation and somewhat more difficult analysis. The case in which X is not compact is important in the analysis of economic growth, since most interesting models of growth will involve the state variable, e.g., the capital stock, growing steadily. Nevertheless, in many cases, with a convenient normalization, the mathematical problem can be turned in to one in which the state variable lies in a compact set. One class of important problems that cannot be treated without allowing for non-compact X are those with endogenous growth. However, since the methods developed in the next chapter do not require this type of compactness assumption and since I will often use continuous-time methods to study endogenous growth models, I simplify the discussion here by assuming that X is compact.

Note also that since X is compact, G (x) is continuous and compact-valued, Xg is also compact. Since a continuous function on a compact domain is also bounded (Corollary A.1 in Appendix Chapter A), Assumption 6.2 also implies that U is bounded, which will be important for some of the results below.

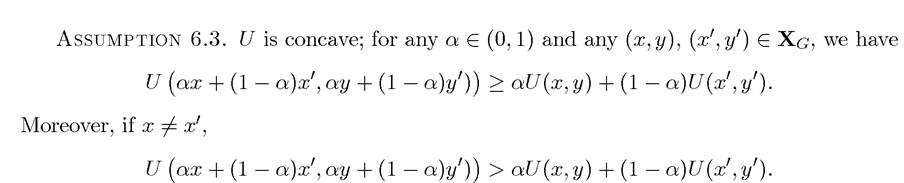

Many (but not all) economic problems impose additional structure on preferences and technology, for example, in the form of concavity or monotonicity of the instantaneous payoff function U and convexity of the constraints. These properties enable us to establish additional structural results. I now introduce these assumptions formally.

In addition, G is convex; for any α ∈ [0,1], and such that y ∈ G(x) and

such that y ∈ G(x) and

we have

we have

This assumption imposes conditions similar to those used in many economic applications: the constraint set is assumed to be convex and the objective function is concave or strictly concave.

The next assumption puts some more structure on the objective function, in particular it ensures that the objective function is increasing in the state variables (its first K arguments), and that greater levels of the state variables are also attractive from the viewpoint of relaxing the constraints; i.e., a greater x means more choice.

The final assumption is that of differentiability and is also common in most economic models. This assumption will enable us to work with first-order necessary conditions.

Assumption 6.5. U is continuously differentiable on the interior of its domain Xg.

Given these assumptions, the following sequence of results can be established. The proofs for these results are provided in Section 6.5.

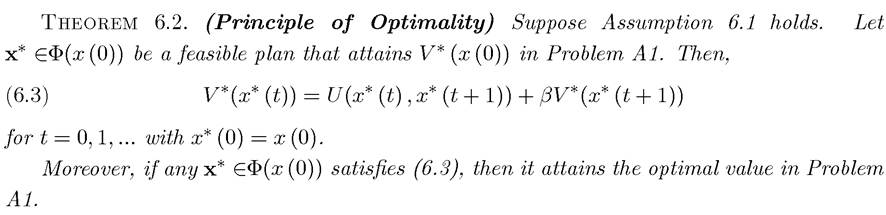

Therefore, both the sequence problem and the recursive formulation achieve the same value. The next theorem establishes the more important result that solutions to Problems A1 and A2 coincide.

This theorem is the major conceptual result in the theory of dynamic programming. It states that the returns from an optimal plan (sequence) x* ∈Φ(x (0)) can be broken into two parts; the current return, U(x* (t),x* (t + 1)), and the continuation return βV*(x* (t + 1)), where the continuation return is given by the discounted value of a problem starting from

210

the state vector from tomorrow onwards, x* (t + 1). In view of the fact that V * in Problem A1 and V in Problem A2 are identical (cf. Theorem 6.1), (6.3) also implies

Notice also that the second part of Theorem 6.2 is equally important. It states that if any feasible plan x* starting with x (0), that is, x* ∈Φ(x (0)), satisfies (6.3), then x* attains V * (x (0)). Therefore, this theorem states that we can go from the solution of the recursive problem to the solution of the original problem and vice versa. Consequently, as long as Assumption 6.1 is satisfied there is no risk of excluding solutions when the problem is formulated recursively.

The next results summarize certain important features of the value function V in Problem A2. These results will be useful in characterizing qualitative features of optimal plans in dynamic optimization problems without explicitly finding the solutions.

Theorem 6.3. (Existence of Solutions) Suppose that Assumptions 6.1 and 6.2 hold.

Then, there exists a unique continuous and bounded function V : X → R that satisfies (6.1). Moreover, an optimal plan x* ∈Φ(x (0)) exists for any x (0) ∈ X.This theorem establishes two major results. The first is the uniqueness of the value function (and hence of the Bellman equation) in dynamic programming problems. Combined with Theorem 6.1, this result naturally implies that an optimal policy function (correspondence) achieving the supremum V* in Problem A1 exists and also that like V, V* is continuous and bounded. The optimal plan or the policy function corresponding to Problem A1 or A2 may not be unique, however, even though the value function is unique. This may be the case when two alternative feasible sequences achieve the same maximal value. As in static optimization problems, non-uniqueness of solutions is a consequence of lack of strict concavity of the objective function. When the conditions are strengthened by including Assumption 6.3, uniqueness of the optimal plan is guaranteed.

Theorem 6.4. (Concavity of the Value Function) Suppose that Assumptions 6.1, 6.2 and 6.3 hold. Then, the unique V : X → R that satisfies (6.1) is strictly concave.

In addition, it is straightforward to verify that if Assumption 6.3 is relaxed so that U is concave, then a weaker version of Theorem 6.4 applies and implies that V is concave. Combining the previous two theorems:

COROLLARY 6.1. Suppose that Assumptions 6.1, 6.2 and 6.3 hold. Then, there exists a unique optimal plan x* ∈Φ(x (0)) for any x (0) ∈ X. Moreover, the optimal plan can be expressed as x* (t + 1) = π (x* (t)), where π : X → X is a continuous policy function.

The important result in this corollary is that the “policy function” π is indeed a function, not a correspondence. This is a consequence of the fact that x* is uniquely determined. This result also implies that the policy mapping π is continuous in the state vector.

Moreover, if 211there exists a vector of parameters z continuously affecting either the constraint correspondence Φ or the instantaneous payoff function U, then the same argument establishes that π is also continuous in this vector of parameters. This feature will enable qualitative analysis of dynamic macroeconomic models under a variety of circumstances.

Our next result shows that under Assumption 6.4, the value function V is also strictly increasing.

Theorem 6.5. (Monotonicity of the Value Function) Suppose that Assumptions

6.1, 6.2 and 6.4 hold and let V : X → R be the unique solution to (6.1). Then, V is strictly increasing in all of its arguments.

Finally, our purpose in developing the recursive formulation is to use it for characterizing the solution to dynamic optimization problems. As with static optimization problems, this is often made easier by using differential calculus. The difficulty in using differential calculus with (6.1) is that the right-hand side of this expression includes the value function V, which is endogenously determined. We can only use differential calculus if we know from more primitive arguments that this value function is indeed differentiable. The next theorem ensures that this is the case and also provides an expression for the gradient of the value function, which corresponds to a version of the familiar Envelope Theorem (Theorem A.32 in Appendix Chapter A). Recall that IntX denotes the interior of the set X, Dxf denotes the gradient of the function f with respect to the vector x, and Df denotes the gradient of the function f with respect to all of its arguments (see Appendix Chapter A).

Theorem 6.6. (Differentiability of the Value Function) Suppose that Assumptions

6.1, 6.2, 6.3 and 6.5 hold. Let π (∙) be the policy function defined above and assume that x ∈IntX and π (x) ∈IntG (x), then V (∙) is differentiable at x, with gradient given by

(6.4) DV (x) = DχU (x,π (x)).

These results will us to use dynamic programming techniques in a wide variety of dynamic optimization problems. Before doing so, I discuss how these results are proved. The next section introduces a number of mathematical tools from basic functional analysis necessary for proving some of these theorems and Section 6.5 provides the proofs of all the results stated in this section.

6.4.