The Conduct of Monetary Policy: Rules Versus Discretion

Discuss whether monetary policy should be conducted by rules or discretion.

From this description of rules and discretion, you may have trouble understanding why many economists advocate the use of rules.

After all, why should anyone arbitrarily and unnecessarily tie the hands of the central bank? The idea that giving the central bank the option of responding to changing economic conditions as it sees fit is always better than putting monetary policy in a straitjacket dictated by rules is the essence of the Keynesian case for discretion.This basic argument for discretion is attractive, but a strong case also may be made for rules. Next we discuss the traditional monetarist argument for rules. We then consider a relatively new argument for rules: that the use of rules increases the credibility of the central bank.

The Monetarist Case for Rules

Monetarism emphasizes the importance of monetary factors in the macroeconomy. Although monetarists have included numerous outstanding economists, the dominant figure and leader of the group was Milton Friedman. For many years, Friedman argued that monetary policy should be conducted by rules, and this idea has become an important part of monetarist doctrine.[275]

Friedman's argument for rules may be broken down into a series of propositions.

Proposition 1. Monetary policy has powerful short-run effects on the real economy. In the longer run, however, changes in the money supply have their primary effect on the price level.

Friedman's research on U.S. monetary history (with Anna Schwartz) provided some of the earliest and best evidence that changes in the money supply can be nonneutral in the short run (Chapter 10). Friedman and other monetarists believe that fluctuations in the money supply historically have been one of the most sig- nificant—if not the most significant—sources of business cycle fluctuations.

On long-run neutrality, Friedman (along with Edmund Phelps) was one of the first to argue that, because prices eventually adjust to changes in the money supply, the effect of money on real variables can be only temporary (Chapter 12).Proposition 2. Despite the powerful short-run effect of money on the economy, there is little scope for using monetary policy actively to try to smooth business cycles.

Friedman backed this proposition with several points (several of which we discussed in connection with macroeconomic policy more generally in earlier chapters). First, time is needed for the central bank and other agencies to gather and process information about the current state of the economy. These information lags may make it difficult for the central bank to determine whether the economy actually is in a recession and whether a change in policy is appropriate.

Second, there is considerable uncertainty about how much effect a change in the money supply will have on the economy and how long the effect will take to occur (see Fig. 14.10). Friedman has emphasized that there are long and variable lags between monetary policy actions and their economic results. That is, not only does monetary policy take a relatively long time to work, but the amount of time it takes to work is unpredictable and can vary from episode to episode.

Third, wage and price adjustment, although not instantaneous, occurs rapidly enough that, by the time the Fed recognizes that the economy is in a recession and increases the money supply, the economy may already be heading out of the recession. If the expansion in the money supply stimulates the economy with a lag of about a year, the stimulus may take effect when output has already recovered and the economy is in a boom. In this case the monetary expansion will cause the economy to overshoot full employment and cause prices to rise. Thus the monetary increase, intended to fight the recession, may actually be destabilizing (causing more variability of output than there would have been otherwise), as well as inflationary.

Proposition 3. Even if there is some scope for using monetary policy to smooth business cycles, the Fed cannot be relied on to do so effectively.

One reason that Friedman didn't trust the Fed to manage an activist monetary policy effectively was political. He believed that despite its supposed independence, the Fed is susceptible to short-run political pressures from the President and others in the administration. For example, the Fed might be pressured to stimulate the economy during an election year. If timed reasonably well, an election- year monetary expansion could expand output and employment just before voters go to the polls, with the inflationary effects of the policy not being felt until after the incumbents were safely reelected.

More fundamentally, though, Friedman's distrust of the Fed arose from his interpretation of macroeconomic history. From his work with Anna Schwartz, Friedman concluded that for whatever reason—incompetence, shortsightedness, or bad luck—monetary policy historically has been a greater source of economic instability than stability. The primary example cited by Friedman is the 1929-1933 period, when the Fed was unable or unwilling to stop the money supply from falling by one-third in the wake of widespread runs on banks. Friedman and Schwartz argued that this monetary contraction was one of the main causes of the Great Depression. Thus Friedman concluded that eliminating monetary policy as a source of instability would substantially improve macroeconomic performance.

How could the Fed be removed as a source of instability? This question led to Friedman's policy recommendation, the last proposition.

Proposition 4. The Fed should choose a specific monetary aggregate (such as Ml or M2) and commit itself to making that aggregate grow at a fixed percentage rate, year in and year out.

For Friedman, the crucial step in eliminating the Fed as a source of instability was to get it to give up activist, or discretionary, monetary policy and to commit itself—publicly and in advance—to following some rule.

Although the exact choice of a rule isn't critical, Friedman believed that a constant-money-growth rule would be a good choice for two reasons. First, the Fed has considerable influence, though not complete control, over the rate of money growth. Thus if money growth deviated significantly from its target, the Fed couldn't easily blame the deviation on forces beyond its control. Second, Friedman argued that steady money growth would lead to smaller cyclical fluctuations than the supposedly "countercyclical" monetary policies utilized historically. He concluded that a constant money growth rate would provide a "stable monetary background" that would allow economic growth to proceed without concern about monetary instability.Friedman didn't advocate a sudden shift from discretionary monetary policy to a low, constant rate of money growth. Instead, he envisioned a transition period in which the Fed, by gradual preannounced steps, would steadily reduce the growth rate of money. Ultimately, the growth rate of the monetary aggregate selected would be consistent with an inflation rate near zero. Importantly, after the constant growth rate has been attained, the Fed wouldn't respond to modest economic downturns by increasing money growth but would continue to follow the policy of maintaining a fixed rate of money growth. However, in some of his writings Friedman appeared to leave open the possibility that the monetary rule could be temporarily suspended in the face of major economic crises, such as a depression.

Rules and Central Bank Credibility

Much of the monetarist argument for rules rests on pessimism about the competence or political reliability of the Federal Reserve. Economists who are more optimistic about the ability of the government to intervene effectively in the economy (which includes many Keynesians) question the monetarist case for rules. A "policy optimist" could argue as follows:

Monetary policy may have performed badly in the past.

However, as time passes, we learn more about the economy and the use of policy gets better. For example, U.S. monetary policy clearly was handled better after World War II than during the Great Depression. Imposing rigid rules just as we are beginning to learn how to use activist policy properly would be foolish. As to the issue of political reliability, that problem affects fiscal policymakers and indeed all our branches of government. We just have to trust in the democratic process to ensure that policymakers will take actions that for the most part are in the best interests of the country.For policy optimists this reply to the monetarist case for rules seems perfectly satisfactory. During the past three decades, however, a new argument for rules has been developed that applies even if the central bank knows exactly how monetary changes affect the economy and is completely public-spirited. Thus the new argument for rules is a challenge even to policy optimists. It holds that the use of monetary rules can improve the credibility of the central bank, or the degree to which the public believes central bank announcements about future policy, and that the credibility of the central bank influences how well monetary policy works.

One reason that the central bank's credibility matters is that people's expectations of the central bank's actions affect their behavior. For example, suppose that the central bank announces that it intends to maintain a stable price level by maintaining a stable money supply. If firms increase prices and the aggregate price level increases, the real money supply will fall, causing the LM curve to shift up and to the left. As a result output and employment will fall. If firms collectively believe the Fed will try to fight the drop in output and employment by increasing the nominal money supply—contrary to its stated intentions to maintain a stable money supply—they will go ahead and raise prices. However, if firms collectively believe that the central bank will abide by its stated intention to maintain a stable money supply, they will not increase their prices because they realize that the central bank will allow the drop in output and employment to occur and the firms will have to reduce prices in the future anyway.

Thus, if the central bank's statement that it intends to maintain stable prices and money is credible, firms won't raise prices; however, if the central bank's statement lacks credibility, prices will rise.Rules, Commitment, and Credibility. We have seen why central bank credibility is important. If a central bank is credible, it can maintain stable prices even if business firms threaten to raise prices. But how can a central bank achieve credibility?

One possibility is for the central bank to develop a reputation for carrying out its promises. Suppose that in the preceding example firms raise their prices, fully expecting the Fed to increase the money supply. However, the Fed holds the money supply constant, causing a recession. The next time, the firms may take the Fed's promises more seriously.

The problem with this strategy is that it may involve serious costs while the reputation is being established: The economy suffers a recession while the central bank establishes its reputation. Is there some less costly way to achieve credibility?

Advocates of rules suggest that, by forcing the central bank to keep its promises, rules may substitute for reputation in establishing credibility. Suppose that there is an ironclad rule—ideally, enforced by some outside agency—that the Fed must maintain a constant growth rate of the money supply. Observing the existence of this rule, the firms might well believe that money supply growth is going to be steady no matter what, and price stability can be achieved. Note that if it increases credibility, a rule improves central bank performance even if the central bank is competent and public-spirited. Hence this reason for monetary policy rules is different from the monetarists' argument presented earlier.

How do advocates of discretion respond to the credibility argument for rules? Keynesians argue that there may be a trade-off between credibility and flexibility. For a rule to establish credibility, it must be virtually impossible to change—otherwise, no one will believe that the Fed will stick to it. In the extreme, the monetary growth rule would be added as an amendment to the Constitution, which could then be changed only at great cost and with long delays. But if a rule is completely unbreakable, what happens (ask the Keynesians) if some unexpected crisis arises—for example, a new depression? In that case the inability of the Fed to take corrective action—that is, its lack of flexibility—could prove disastrous. Therefore, Keynesians argue, establishing a rule ironclad enough to create credibility for the central bank would, by eliminating policy flexibility, also create unacceptable risks.

The Taylor Rule

Advocates of the use of rules in monetary policy believe that the Fed should be required to follow a set of simple, prespecified, and publicly announced rules when setting policy instruments. Nothing in the concept of rules, however, necessarily prohibits the Fed from responding to the state of the economy, as long as those responses are built into the rule itself. An example of a monetary policy rule that allows the Fed to take economic conditions into account is the so-called Taylor rule, introduced by John Taylor[276] of Stanford University. The Taylor rule is given by

i = ∏ + 0.02 + 0.5y + 0.5(π - 0.02), (14.1)

where

i = the nominal fed funds rate (the Fed's intermediate target); π = the rate of inflation over the previous four quarters;

from full-employment output.

The Taylor rule requires that the real fed funds rate, i — π, respond to (1) the difference between output and full-employment output and (2) the difference between inflation and its target, here taken to be 2%, or 0.02. The Taylor rule fits in with the idea we discussed in Section 14.3 that many central banks target the real interest rate rather than the real money supply, as an intermediate target. Notice that if output is at its full-employment level and inflation is at its 2% target, the Taylor rule has the Fed setting the real fed funds rate at 2%, which is approximately its long-run average level. If the economy is "overheating," with output above its full-employment level and inflation above its target, the Taylor rule would have the Fed tighten monetary policy by raising the real fed funds rate above 2%. Conversely, if the economy shows weakness, with output below its full-employment level and inflation below its target, the Taylor rule indicates that the real fed funds rate should be reduced below 2%, thereby easing monetary policy. Both responses are consistent with standard Fed practice. Indeed, Taylor showed that, historically, his relatively simple rule describes actual Fed behavior quite accurately.

Since Taylor first wrote about the rule in 1993, economists all over the world have studied its properties, and it has become common to assume that a central bank follows some type of rule that is similar to the Taylor rule. In practice, economists at central banks often show what policy should be used to follow the Taylor rule and then make an argument for why they might want to deviate from the rule. Recently, Taylor himself has suggested an even stronger role for his rule, advocating legislation requiring the Fed to follow the rule and to justify to Congress any deviations from the rule. Such a requirement would face many operational difficulties, however, such as defining the output gap in real time and dealing with the fact that the rule would sometimes require a negative nominal interest rate, which would be difficult to achieve.

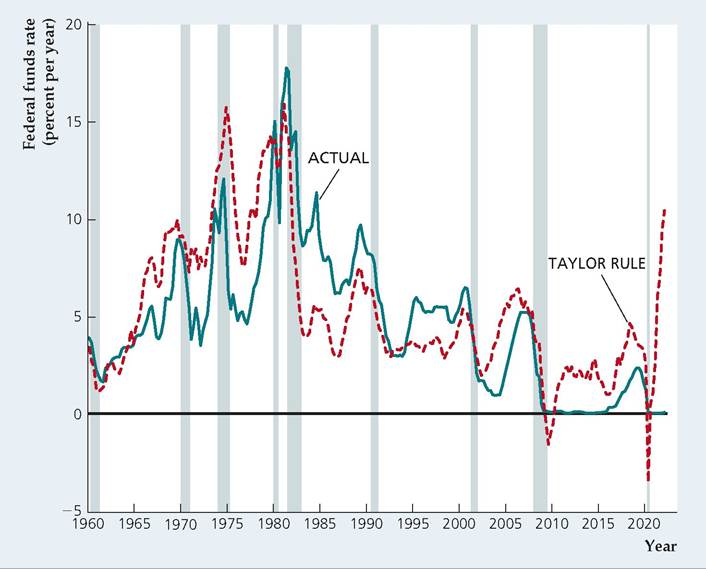

Figure 14.11 illustrates the actual federal funds rate over time and what the federal funds rate would have been if the original Taylor rule had been followed.[277] The Fed set the federal funds rate well below the level suggested by the Taylor rule in the late 1960s and throughout the 1970s. In that period, the inflation rate rose from about 1% in 1963 to more than 10% by 1975, averaging 2.4% in the 1960s and 6.7% in the 1970s. In the 1980s, the Fed set the federal funds rate above the level suggested by the Taylor rule, causing inflation to decline from 10% in 1981 to 3.5% in 1989; it averaged 4.5% over the decade. In the 1990s, the federal funds rate was set close to or slightly above the level suggested by the Taylor rule, and the inflation rate averaged just 2.1% over the decade. From 2000 to 2020, the federal funds rate was frequently lower than the level suggested by the Taylor rule, though the inflation rate averaged 2.0%. But inflation began rising in 2021, and the Federal Reserve was very slow in raising interest rates and tightening monetary policy, as Figure 14.4 shows. The Taylor rule suggested that the federal funds rate should have been nearly 10% by the end of 2021, while the Fed kept the rate near zero.

For the past 50 years, the Taylor rule seems to have performed about as expected. When the Fed has set the federal funds rate below the level suggested by the Taylor rule, inflation has often risen, and when the fed funds rate has been above the level suggested by the Taylor rule, inflation has often fallen. One

FIGURE 14.11

Taylor rule and actual federal funds rate, 1960-2022

The Fed set the federal funds rate well below the level suggested by the Taylor rule in the late 1960s and 1970s, leading to increased inflation. In the 1980s, the Fed set the federal funds rate above the level suggested by the Taylor rule, causing inflation to decline. In the 1990s, the federal funds rate was set fairly close to that suggested by the rule. In the 2000s, the federal funds rate has mainly been lower than the level suggested by the Taylor rule. The shaded bars in the figure represent recessions.

Source: Author's calculations based on Eq. (14.1) and data from 1960 to the first quarter of 2022, downloaded from Federal Reserve Bank of St. Louis FRED database, fred. stlouisfed.org. GDP price index and nominal output from Bureau of Economic Analysis, FRED variables GDPCTPI and GDP, respectively. Fullemployment output from Congressional Budget Office, FRED variable GDPPOT. Federal funds rate from Federal Reserve Board of Governors, FRED variable FEDFUNDS.

exception has been from 2000 to 2020, when inflation did not rise, even though the Fed seems to have set the federal funds rate below the level suggested by the Taylor rule for a substantial part of the period. Clearly, in the financial crisis of 2008, with a potentially catastrophic breakdown in credit markets, the Fed could justify its actions. But even in the early 2000s, when the economy was in a recession followed by a period of slow growth, the Fed indicated concerns about the possibility of deflation, which justified keeping the federal funds rate below the level suggested by the Taylor rule. However, inflation began rising sharply in 2021, consistent with the fed funds rate being far below that suggested by the Taylor rule.

The Taylor rule in Eq. (14.1) has been the subject of extensive research in the past 20 years. Economists have discovered that the rule may work better if formulated in terms of forecasts for the future values of inflation and the deviation of output from full-employment output rather than looking at past inflation and the current level of output relative to full-employment output. Economists have also experimented with different coefficients on the terms of the rule (alternatives to Taylor's initial 0.5 coefficients on the output term and the inflation term) and examined targets other than 2% inflation. Experience with the Taylor rule has shown that uncertainty about the output term in the Taylor rule is large because output is revised significantly at times and because the level of potential output is sometimes very different than what policymakers and economists thought it was in real time.[278] Nonetheless, for central banks all over the world, the Taylor rule has become a focal point of policy discussions.

Other Ways to Achieve Central Bank Credibility

Besides announcing targets for money growth or inflation, are there other ways to increase the central bank's credibility and thus improve the performance of monetary policy?

One way to increase a central bank's credibility is by enhancing its reputation as an inflation fighter. A central bank's reputation can be improved when it announces specific goals and shows that it can meet them. Another way to enhance the central bank's reputation is by appointing a tough central banker. For example, the President could appoint a Fed chairman who strongly dislikes inflation and who people believe is willing to accept increased unemployment if necessary to bring inflation down. Thus when President Jimmy Carter faced a serious inflation problem in 1979, he appointed Paul Volcker—an imposing individual with a strong anti-inflation reputation—to be chairman of the Fed. In appointing a "tough" central banker, Carter hoped to convince the financial markets and the public that he was serious about reducing inflation. Volcker succeeded in getting rid of inflation, but because unemployment

Application

continent have adopted inflation targeting, including Canada (1991), the United Kingdom (1992), Sweden (1993), Finland (1993), Australia (1994), Spain (1994), South Africa (2000), India (2015), and Ghana (2007). Some advanced economies' central banks such as the European Central Bank and the U.S. Federal Reserve, though not officially "inflation targeters," adopt many elements of inflation targeting and pursue a modified inflation targeting approach. Some countries, including Finland and Spain, gave up their own targets with their adoption of the euro.

Advocates of inflation targeting argue that commitment to an explicit numerical target increases central banks' accountability and potentially increases the likelihood that they will focus on long-run policies while resisting pressures to pursue short-run expansionary policies that are inconsistent with the long-run goal of price stability. Critics, however, caution that the central banks' focus on inflation targeting may allow unsustainable speculative bubbles and other economic distortions to thrive unchecked until it is too late, when the inflation trickles down from asset prices to retail consumer prices, as was the case in the 2008 financial crisis.[279] Moreover, inflation is known to respond to policy with a long lag.

For inflation targeting to succeed, fiscal policy considerations should not dictate monetary policy. Although inflation-targeting central banks may not be entirely independent of governments' influence, they must have the freedom to decide the instruments to use to achieve the target. They must commit to not target other indicators, such as wages, employment levels, or the exchange rate. In many countries, these commitments are difficult, and unsurprisingly, many consistently fall outside their target bands.

33See Willem Buiter and Paolo Pesenti, "Rational Speculative Bubbles in an Exchange Rate Target Zone,” NBER Working Paper 3467,1990, https://www.nber.org/papers/w3467.

►