Making Monetary Policy in Practice

Discuss the difficulties of making monetary policy.

The IS-LM or AD-AS analysis of monetary policy suggests that using monetary policy to affect output and prices is a relatively simple matter: All that the Fed needs to do is change the money supply enough to shift the LM curve or the AD curve to the desired point.

In reality, however, making monetary policy is a complex, ongoing process. Two important practical issues that policymakers have to deal with are the lags in the effects of monetary policy on the economy and how to deal with uncertainty about the state of the economy, economic models, and expectations.Lags in the Effects of Monetary Policy

If changes in the money supply led to immediate changes in output or prices, using monetary policy to stabilize the economy would be relatively easy. The Fed would simply have to adjust its policy instruments until the economy attained full employment with stable prices. Unfortunately, most empirical evidence suggests that changes in monetary policy take a fairly long time to affect the economy, which is the impact lag that we discussed in the section "Should Fiscal Policy Be Used to Dampen the Cycle?" in Chapter 10.

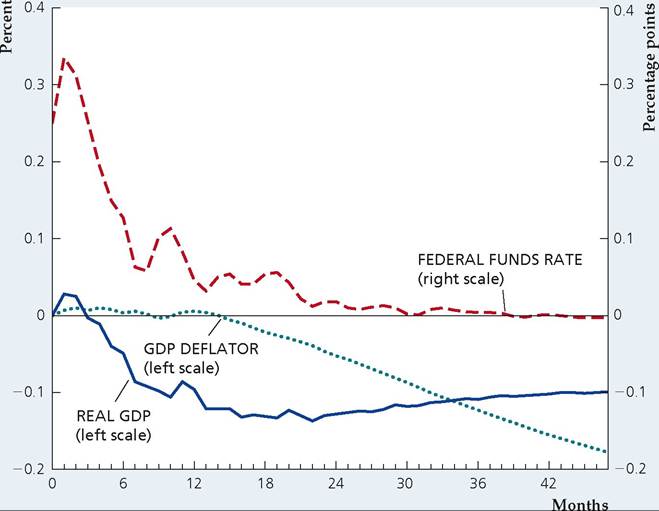

FIGUREJ4.10

Responses of output, prices, and the fed funds rate to a monetary policy shock

Shown are the estimated changes in the fed funds rate, real GDP, and the GDP deflator during the first 48 months following an unanticipated tightening of monetary policy by the Fed. The fed funds rate and other interest rates respond quickly to monetary policy changes, but output (real GDP) and the price level (the GDP deflator) respond much more slowly. The long impact lags in the responses of output and prices illustrate the difficulty of using monetary policy to stabilize the economy.

Some empirical estimates of how long it takes monetary policy to work are presented in Figure 14.10, adapted from an article by former Federal Reserve Chairman Ben Bernanke and Mark Gertler[266] of New York University.

Shown are the estimated behaviors of three important variables during the first 48 months after an unanticipated tightening of monetary policy by the Fed. The variables shown are the fed funds rate (described in Section 14.2), real GDP (a measure of output), and the GDP deflator (a measure of the price level).[267] The left vertical axis measures the changes in real GDP and the GDP deflator that occur after the policy change, in percent; the right vertical axis measures the change in the federal funds rate that occurs after the policy change, in percentage points.Note that interest rates (here, the fed funds rate) react quickly to monetary policy changes. Following a tightening of monetary policy, the fed funds rate rises by more than 0.3 percentage point (for example, from 5.0% to 5.3%) within a month. However, the effect of the policy change on interest rates is transitory; the fed funds rate starts falling quickly, and six to twelve months after the monetary policy tightening it has nearly returned to its original value.

In contrast, output and (especially) the price level take much longer to respond to the change in monetary policy. Real GDP barely responds to the policy change during the first four months or so. (Figure 14.10 actually shows a slight rise in GDP during the first two months rather than the expected drop; this "wrong" response probably reflects statistical uncertainty in the estimates rather than actual economic behavior.) After about four months GDP begins to decline sharply, but the full effect on output isn't felt until 16 to 20 months after the initial policy change.

The response of prices to the policy change is even slower than that of output. The price level remains essentially unaffected for more than a year after the monetary policy action! Only after this long delay does the tightening of monetary policy cause prices to begin to fall.

The long impact lags in the operation of monetary policy make it difficult to use this policy instrument with precision.[268] Because of the long impact lag as well as the recognition lag, the FOMC can't base its decisions on current levels of output and inflation alone.

Instead, it must try to forecast what the economy will be doing six months to two years in the future—and make policy based on those forecasts. Because economic forecasts are often inaccurate, monetary policymaking has sometimes been likened to trying to steer a ship in a dense fog.An illustration of the problems raised by the delayed effects of monetary policy is a debate about how aggressive the Fed should be in its anti-inflationary policies. The FOMC has on several occasions engaged in what were called preemptive strikes on inflation, raising the fed funds rate (that is, tightening monetary policy) even though the current inflation rate was low. Critics of the Fed asked why tightening monetary policy was necessary when inflation wasn't currently a problem. The FOMC responded that they weren't reacting to current inflation but rather to forecasts of inflation a year or more into the future. They were correct in asserting that, because of lags in monetary policy, trying to anticipate future inflation, rather than reacting only to current inflation, is necessary. Because of the difficulties in forecasting inflation, however, there was plenty of room for debate about how tight monetary policy needed to be to prevent future inflation.

Conducting Monetary Policy Under Uncertainty

In practice, conducting monetary policy is much more difficult than our models suggest because policymakers face uncertainty in three dimensions: (1) They are uncertain about the current state of the economy; (2) their models of the economy are incomplete; and (3) they are unsure about how the expectations of the public will be affected by economic shocks and policy actions.[269]

Policymakers try to discern the overall state of the economy by examining data on hundreds of different economic variables, which often give conflicting signals about the current strength of the economy. Complicating the matter further, data are often revised, and the initial releases of the data are much less accurate than later releases of the data.[270] Recent research has shown that one way to get a handle on the current state of the economy is to combine the information from many different variables in a dynamic factor model such as the CFNAI or ADS index, as we saw in Chapter 8, "In Touch with Data and Research: Coincident and Leading Indexes."[271]

A second source of uncertainty that affects policymaking is uncertainty about the structure of the economy.

Is the economy best described by the classical model or the Keynesian model, and which variation of each is the best? What are the slopes and locations of each of the curves in each model? What are the levels of full-employment output and the natural rate of unemployment?[272] No one knows the answers to these questions precisely. In the face of such uncertainty about the structure of the economy, early research suggested that policymakers should respond less to shocks to the economy than if they knew the structure of the economy for sure.[273] However, research suggests that if there is a possibility of a particularly bad outcome, such as a deflation leading to a severe recession, then stronger action by monetary policy is warranted. Another aspect of uncertainty about the structure of the economy is uncertainty about the predominant source of shocks to the economy. For instance, in Fig. 14.5, we showed that in the face of nominal shocks to the economy, which cause the LM curve to shift, the central bank can stabilize output by targeting the interest rate. On the other hand, as we showed in Fig. 14.6, if shocks cause shifts of the IS curve, then output will be more stable if the Fed maintains an unchanged nominal money supply than if it maintains an unchanged interest rate. In fact, the economy is hit by both types of shocks. The Taylor Rule (discussed later in this chapter) is a flexible interest rate target that is designed to provide good outcomes under a wide variety of circumstances and in response to various types of shocks.A third major source of uncertainty facing policymakers comes from the impact of economic shocks and policy changes on people's expectations. In the rational-expectations revolution in the 1980s, macroeconomists learned that people's expectations have a major effect on the economy's response to shocks and to policy, as we discussed in Section 10.5 "The Misperceptions Theory and the Nonneutrality of Money" in Chapter 10.

Recent research has shown that if the public is not sure of the central bank's motives, then the central bank should work hard to keep the inflation rate as stable as possible, so that people's expectations can become anchored. In addition, the research suggests that there are large benefits to informing people about the central bank's plans and forecasts. This idea has been put into practice recently by the Federal Reserve, which has explained its actions much more clearly than previously, by providing more detailed minutes of its meetings, announcing its own forecasts four times a year, and holding press conferences after FOMC meetings four times per year.Uncertainty makes monetary policymaking much more difficult than it would be if we knew everything about the economy. As Fed Chairman Ben Bernanke noted in a 2007 speech, "Uncertainty—about the state of the economy, the economy's structure, and the inferences that the public will draw from policy actions or economic developments—is a pervasive feature of monetary policy making.... Most fundamentally, our discussions of the pervasive uncertainty that we face as policymakers is a powerful reminder of the need for humility about our ability to forecast and manage the future course of the economy."[274]

14.5

More on the topic Making Monetary Policy in Practice:

- Making Monetary Policy in Practice

- Central Bank: Credibility, Accountability, and Social Responsibility

- THE THEORY AND PRACTICE OF EMPIRE-BUILDING

- Abel A.B., Bernanke B., Croushore D.. Macroeconomics. 10th Edition, Global Edition. — Pearson,2021. — 690 pp., 2021

- The Conduct of Monetary Policy: Rules Versus Discretion

- Coronavirus monetary policy

- References

- The Demand for Money

- DIRECT INTERVENTIONS IN MODERN TIMES

- 12 Supply of Money