The Provision of Public Goods: Weak Versus Strong States

The analysis so far has emphasized the distortionary effects of taxation and expropriation. This paints a picture whereby the major determinants of poor economic performance are high taxes or some type of expropriation, and political economy does (or should) focus on the determination of the incentives for redistributive taxation.

While the disincentive effects of taxation cannot be denied, whether or not taxes are high is only one of the dimensions of policy that might affect economic growth. For example, in many of the endogenous growth models appropriate R&D or industrial policy might encourage faster growth (even if it involves some taxation of capital and labor). More generally, public good provision, investment in infrastructure and provision of law and order are important roles of a government, and the failure of the government to perform these roles may also have negative consequences for economic performance. In fact, existing evidence does not support the view that growth (or high levels of output) are strongly associated with taxation. On the contrary, poor economies typically have lower levels of tax revenues and government spending. This is most stark if we compare the OECD to sub-Saharan Africa. Consequently, the political economy of growth must also pay attention to whether governments perform the roles that they are supposed to. The standard non-political-economy (for example the traditional public finance) approach to this question starts by positing the existence of a benevolent government and looks for policy combinations that would maximize social welfare. Once we incorporate political economy considerations, however, we recognize that the political elite that control the government may not have an interest in investing in public goods. If public good investments (or investments in infrastructure or law and order) are an important determinant of the growth performance of an economy, it then becomes essential to investigate under what circumstances governments will undertake such investments.In this section, I present the simplest model that can shed light on this topic, which is based on Acemoglu (2005). The economy consists of a political elite controlling the government and a set of citizens with access to production opportunities. Productivity depends on public good investments by the government. The government, on the other hand, will only undertake these investments, if these are beneficial to the political elite. In this section, I therefore investigate the conditions under which a greater amount of investment in public good will be undertaken in a well-defined political equilibrium. Not surprisingly, the extent of public good provision will depend on the future returns that the political elite can secure by undertaking such investments, which is related to the issue of weak versus strong states. If the state is very weak, the elite will be unable to raise taxes in the future and reap the benefits of their investments. Anticipating this, they will be unwilling to invest in public goods. On the other hand, if there are no checks on the ability of the elite to impose taxes on the population, then the state is too “strong,” and private investment will be stifled. Thus states that have intermediate levels of strength are most conducive to economic growth.

This model will also enable us to discuss the potential distinction between expropriation and taxes, an issue raised at the beginning of this chapter.

22.8.1. The Model. All agents have again linear preferences given in (22.1). The population consists of a set of yeoman-entrepreneurs (citizens), with mass normalized to 1, and a political elite. The elite do not engage in production but control the government and thus will decide the levels of taxation and public good provision. Without loss of any generality, we also normalize the size of the political elite to 1.

Each citizen i has access to the following Cobb-Douglas production technology to produce the unique final good in this economy:

which only differs from (22.17) because here A (t) is time-varying.

We will assume that A (t) will be determined by the public good investments of the government. Given the assumption that citizens correspond to yeoman-entrepreneurs, Li (t) = 1 for all i ∈ [0,1] and for all t.The timing of events is similar to the baseline model with holdup, in that taxes on output are set at time t, whereas capital investments for time t are decided at t — 1. There is again a maximum tax rate τ. However, instead of the constitutional limits on taxation, here we suppose that this maximum tax rate arises from the possibility that producers might hide their output (or move to the informal sector) if they face very high taxes. For example, if they do so, they lose a fraction τ of their output, so that with a tax rate above τ, all producers would move to the informal sector and tax revenues would be equal to zero. Consequently, the tax rate at any point in time has to be τ (t) ∈ [0,T]. With this interpretation, T corresponds to the (economic) strength of the state. When T is high, we have a strong state, which can raise high taxes. When it is low, the state is unable to raise high taxes.

As usual, given a tax rate τ (t) ∈ [0, T], tax revenues are

where Y (t) is total output. Naturally, if the tax rate is above τ, tax revenues are equal to zero, because all production shifts to the informal economy.

The government (the political elite) at time t decides how much to spend on public goods for the next date, thus on A (t + 1). I assume that

(22.58)

where G (t) denotes government spending on public goods, and φ > 1, so that there are decreasing returns in the investment technology of the ruler (a greater φ corresponds to greater decreasing returns). The term is included as a convenient normalization.

is included as a convenient normalization.

addition, (22.58) implies full depreciation of A (t), which simplifies the analysis below. The consumption of the elite is given by whatever is left over from tax revenues after expenditure and transfers, thus is equal to Ce (t) = Tax(t) — G (t).

Let us first characterize the first-best level of public good provision, where there are no distortionary taxes on entrepreneurs and the level of public good provision is chosen to maximize the net present discounted value of a representative entrepreneur. Given the production function and the timing of events here, which corresponds to that of the canonical elite-dominated model with Cobb-Douglas technology, the equilibrium capital-labor ratio of an entrepreneur is the same as in (22.18) above. Consequently, the first-best level of public good investment can be computed as

and the first-best levels of the capital-labor ratio and output are

Let us next focus on the Markov Perfect Equilibrium (MPE) of this game. As usual, a MPE is defined as a set of strategies at each date t, such that these strategies only depend on the current (payoff-relevant) state of the economy, A (t), and on prior actions within the same date according to the timing of events above. Thus, a MPE can be represented by (r (A (t)), [ki (A (t))]i∈[o i],G (A (t))^, where, by definition of a MPE, the key actions, which consist of the tax rate on output, τ, the capital-labor ratio decision of each entrepreneur [ki]i∈[o i], and the government expenditure on public good, G, are conditioned on the current payoff-relevant state variable, A (t). Clearly, since each yeoman-entrepreneur employs only himself, the capital-labor ratio, ki, and the total capital stock, Ki, of each entrepreneur are identical.

It is clear that in any MPE, the unique equilibrium tax rate for the political elite will be  since investment decisions are already sunk at the time the elite set the taxes.

since investment decisions are already sunk at the time the elite set the taxes.

Next, the capital-labor ratio of entrepreneurs is again given by (22.18), and thus can be written as

1003

Combining this expression with (22.56) and (22.57), we obtain equilibrium tax revenue as a function of the level of public goods as:

Finally, the elite will choose public investment, G (t) to maximize his consumption. To characterize this, let us write the discounted net present value of the elite as

which simply follows from writing the discounted payoff of the elite recursively, after substituting for their consumption, Ce (t), as equal to taxes given by (22.62) minus their spending on public goods from equation (22.58).

Since, for φ > 1, the instantaneous payoff of the elite is bounded, continuously differentiable and concave in A, so Theorems 6.3, 6.4 and 6.6 in Chapter 6 imply that the value function Vĺ (∙) is concave and continuously differentiable. Hence, the first-order condition of the ruler in choosing A (t + 1) can be written as:

where (Ve)0 denotes the derivative of the value function of the elite. This equation links the marginal cost of greater investment in public goods to the greater value that will follow from this. To make further progress, I use the standard envelope condition, which is obtained by differentiating (22.63) with respect to A(t):

The value of greater public goods for the elite is the additional tax revenue that this will generate, which is given by the expression in (22.65).

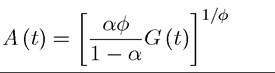

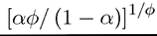

Combining these conditions, we obtain the unique Markov Perfect Equilibrium choice of the elite as:

The second term in (22.67) follows since the level of public with spending implied by (22.66) is equal to a fraction 1∕φ of tax revenue. The value of the elite naturally depends on the current state of public goods, A (t), inherited from the previous period, and from this point on, the equilibrium involves investment levels given by (22.61) and (22.66).

Proof. See Exercise 22.36.

?

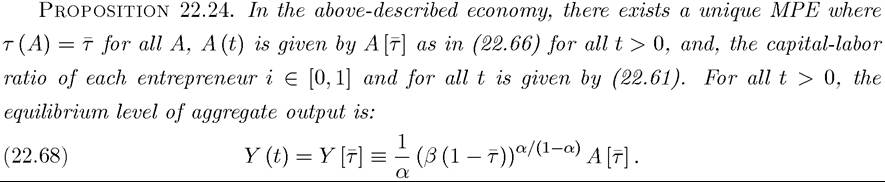

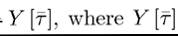

Note that because of linear preferences and full depreciation of public goods, the economy reaches the steady-state level of output in one period (and Y (0) is not given by (22.68), but instead depends on the initial value of the public goods, G (0)).

22.8.2. Weak Versus Strong States. The first result implied by Proposition 22.24 is the importance of the strength of the state as parameterized by T, its ability to raise revenues. When T is high, the state is “economically powerful”—citizens have little recourse against high rates of taxes. In contrast, when T is low, the state is “economically weak” (and there is “limited government”), since it is unable to raise taxes. With this interpretation, we can now ask whether greater economic strength of the state leads to worse economic outcomes. The answer is ambiguous, as it can be seen from the fact that when T = O, i.e., when the state is extremely weak, the elite will choose G (t) = 0, while with T = I, the citizens will choose zero investments. In both cases, output will be equal to zero.

It is straightforward to determine the level of T that maximizes output in the society at all dates after the initial one, i.e., Y (t) for t > 0. It is given by maxτ is

is

given by (22.68). Exercise 22.36 shows that the solution to this program, denoted T*, is

If the economic power of the state is greater than T*, then the state is too powerful, and taxes are too high relative to the output-maximizing benchmark. This corresponds to the standard case on which the political economy models we have studied so far have focused. In contrast, if the economic power of the state is less than T*, then the state is not powerful enough for there to be sufficient rents in the future to entice the elite to invest in public goods. This corresponds to the case, where contrary to what we have emphasized so far, the state is not too powerful, but too weak. Consequently, the elite do not have the correct incentives to invest in productivity-enhancing public goods. Therefore, we have another example of non-growth-enhancing institutions/policies, but this time resulting from the weakness of the state.

There is an interesting parallel to the theory of the firm here. In the theory of the firm, the optimal structure of ownership and control gives ex post bargaining power to the parties that have more important investments. The same principle applies to the allocation of economic 1005

strength as captured by the parameter T; greater power for citizens is beneficial when their investments matter more. When it is the state’s investment that is more important for economic development, a higher T is required (justified).

The above discussion focused on the output-maximizing value of the parameter T. Equally relevant is the level of T, say Te, which maximizes the beginning-of-period payoff to the elite and Tc, which maximizes the beginning-of-period payoff to the citizens. One might also define a tax rate τwm that maximizes the beginning-of-period payoff to a fictitious social planner weighing the elite and the citizens equally. The next proposition shows how these tax rates compare to the output-maximizing tax rate T* :

Proof. See Exercise 22.36. ?

The main conclusion from this analysis is that when both the state and the citizens make productive investments, it is no longer necessarily true that limiting the rents that accrue to the state is always good for economic performance. Instead, there needs to be a certain degree of balance of powers between the state and the citizens. When the political elite controlling the power of the state expect too few rents in the future, they have no incentive to invest in public goods. Consequently, excessively weak states are likely to be as disastrous for economic development as the unchecked power and expropriation by excessively strong states.

A number of shortcomings of the analysis in this section should be noted at this point. The first is that it relied on economic exit options of the citizens in the informal sector as the source of their control over the state, whereas, in practice, political controls may be more important. The second is that it focused on the MPE, without any possibility of an implicit agreement between the state and the citizens, whereby the state raises sufficient tax revenue to both finance public good investments and also distribute some of it to the elite, and the citizens are willing to put up with this high level of taxation because of the benefits that they receive from public good provision, and the elite prefer not to deviate to higher levels of taxes. Acemoglu (2005) generalizes the results presented here in these directions. First, similar results can be obtained when the constraints on the power of the state are not economic, but political. In particular, we can envisage a situation in which citizens can (stochastically) replace the government if taxes are too high. In this case, when citizens are politically powerful, this will limit the extent of taxation, but also the amount of public good provision. Second, using a model with variable political checks on the state, 1006

one can analyze the SPE, where there might be an implicit agreement between the state and the citizens to allow for some amount of taxation and also correspondingly high levels of public good provision. In Acemoglu (2005), I referred to this equilibrium configuration as a “consensually-strong state,” since the citizens allow the economic power of the state to be high (partly because they believe they can politically control the state). The configuration with the consensually-strong state might provide an insight into why many OECD countries have higher tax rates and higher levels of public good provision than many less-developed economies.

This perspective also suggests a useful distinction between taxation and expropriation. As we have seen so far, high taxes have similar effects on investment and economic performance as expropriation. One difference between expropriation and taxes might be uncertainty. It can be argued that producers know exactly at what rate they will be taxed, while expropriation is riskier. In the presence of risk aversion, expropriation could be considerably more costly than taxation. However, the analysis here suggests another useful distinction, which comes not from the revenue side but from the expenditure side; expropriation might correspond to the government taking a share of the output the producers for its own consumption, while taxation, along-the-equilibrium path, involves some of the revenues being spent for public goods, which are useful for the producers. If this distinction is important, one of the reasons why taxation is viewed as fundamentally different from expropriation may be because taxation is often associated with some of the proceeds being given back to the citizens in the form of public goods.

Perhaps the most important implication of the analysis in this section is to emphasize different aspects of growth-enhancing institutions. Economic growth not only requires secure property rights and low taxes, but also complementary investments, often most efficiently undertaken by the government. Provision of law and order, investment in infrastructure and public goods are obvious examples. Thus growth-promoting institutions need to provide some degree of security of property rights to individuals, but also incentivize the government to undertake the appropriate public good investments. In this light, excessively weak governments might be as costly as the unchecked power of the government.

22.9.