The Savings Rate and the Golden Rule

One can prove that a rise in the savings rate results in an increase in steady state capital and output, in both aggregate and per capita terms. It can also be shown that the rate of growth of the aggregate capital stock, output, and income rise temporarily above the steady state or long-run rate of economic growth g + n.

Similarly, following a rise in the savings rate, the rate of growth of the per capita capital stock and per capita output and income rise temporarily above the rate of technical progress g, which determines the steady state growth rate of per capita magnitudes. The relevant analysis is presented in figure 3.4.

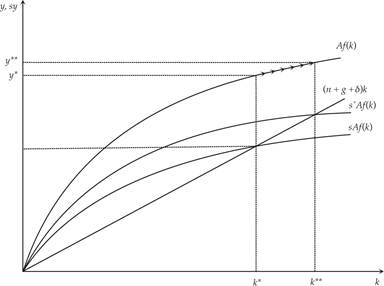

Figure 3.4 Implications of a rise in the savings rate.

3.3.1 The Savings Rate and the Balanced Growth Path

Assume that the initial balanced growth path is at (y*, k*) in figure 3.4. A rise in the savings rate from s to s′ leads to an increase in savings and investment that initiates a process of capital accumulation, which gradually causes an increase in output and income per efficiency unit of labor. The economy starts converging to a new balanced growth path ( y**, k**), which is characterized by both higher capital and higher income. During the adjustment process, savings and investment exceed equilibrium investment, and the rate of growth exceeds the long-run growth rate g + n.

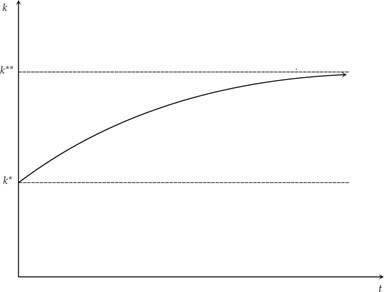

The process of convergence toward the new balanced growth path over time is depicted in figure 3.5, which shows the so-called impulse response function of the Solow model to a change in the savings rate.6

Figure 3.5 Impulse response function of a rise in the savings rate.

The rise in the savings rate leads to investment that exceeds the level required to maintain the capital stock per effective unit of labor at its initial steady state level k*. Capital starts accumulating at a faster rate, leading to parallel rises in output and income per effective unit of labor, and the process continues until the economy gradually converges to the new balanced growth path k**. This process of convergence is asymptotic.7

3.3.2 The Savings Rate, the Golden Rule, and Dynamic Inefficiency

Capital and income increase definitely and unequivocally following a rise in the savings rate. What happens to consumption is more uncertain, as a rise in the savings rate reduces consumption for any given level of income. Initially, as capital, output, and income are given, a rise in the savings rate causes a temporary fall in consumption. Capital output and income gradually rise, and so does consumption. Whether consumption per capita on the new balanced growth path will be higher or lower than on the original balanced growth path depends on the difference between the marginal product of capital and n + g + δ. The latter is the marginal increase in steady state investment. Consumption will be higher on the new balanced growth path if the marginal product of capital is higher than n + g + δ, and it will be lower in the opposite case.

To see this, recall that steady state consumption is given by

It follows that the change in steady state consumption following a rise in the savings rate is given by

Because the last term on the right-hand side of (3.21) has been shown to be positive, the impact of the change in the savings rate on steady state consumption per effective unit of labor depends on the difference between the marginal product of capital Af′(k*) and the equilibrium investment rate n + g + δ.

Another way to express this is to say that the change in steady state consumption depends on the difference between the net (of depreciation) marginal product of capital Af′(k*) − δ and the long-run growth rate g + n.If the net marginal product of capital is lower than the long-run growth rate, then the extra product from the accumulation of capital will not be sufficient to fund the higher equilibrium investment rate, and consumption will have to go down. If the net marginal product of capital is higher than the long-run growth rate, then the extra product from the accumulation of capital will be more than sufficient to fund the higher equilibrium investment rate, and consumption will also increase.

In the special case where the net marginal product of capital on the original balanced growth path is exactly equal to the long-run growth rate, equilibrium consumption will remain unchanged following an infinitesimally small rise in the savings rate. In this case, equilibrium consumption is at its highest possible level, and the value of k* that corresponds to this case is referred to as the golden rule capital stock.8

The golden rule savings rate is defined as the savings rate that implies a steady state capital stock (per effective unit of labor) that maximizes steady state consumption (per effective unit of labor). Because the welfare of households is usually assumed to depend on consumption, the maximization of steady state consumption per effective unit of labor is a proxy for the maximization of steady state consumer welfare.

From (3.20), the first-order conditions for the maximization of steady state consumption require

From (3.22), the steady state capital stock that maximizes steady state consumption is the one that results in a net marginal product of capital equal to the long-run growth rate.

This is what determines the golden rule capital stock. Because the net marginal product of capital is equal to the real interest rate in a competitive equilibrium, the golden rule capital stock is the one for which the real interest rate is equal to the steady state growth rate:

If the savings rate is such that the steady state capital stock is higher than the golden rule capital stock, then the economy is said to be characterized by dynamic inefficiency. Steady state consumption and presumably, consumer welfare could be increased by reducing the savings rate, consuming more, and accumulating less capital. By reducing the savings rate, households will be able to enjoy higher steady state consumption, despite the reduction in steady state capital and output.

Thus, an increase in the savings rate is not necessarily always desirable in the Solow model, even though it results in an increase in steady state capital and income. It is only desirable as long as the savings rate is below the golden rule rate (i.e., the rate that maximizes steady state consumption per efficiency unit of labor). In such a case, an increase in the savings rate increases steady state consumption.

A major problem with the Solow model is that, because the savings rate is assumed exogenous, there is nothing in the model that can help exclude the possibility of dynamic inefficiency (that is, a suboptimally high savings rate). It is therefore worth keeping in mind than an increase in the savings rate is not necessarily desirable from the point of view of consumer welfare. It is only desirable in the case of dynamic efficiency, that is, when the real interest rate exceeds the steady state growth rate.9

Exercise 3.4 Assuming a Cobb-Douglas production function, as in exercise 3.1, derive and discuss the condition determining the golden rule capital stock in the Solow model. What should be the objective of policy with regard to the savings rate if the economy is characterized by dynamic inefficiency?

3.3.3 The Elasticity of Steady State Output with Respect to the Savings Rate

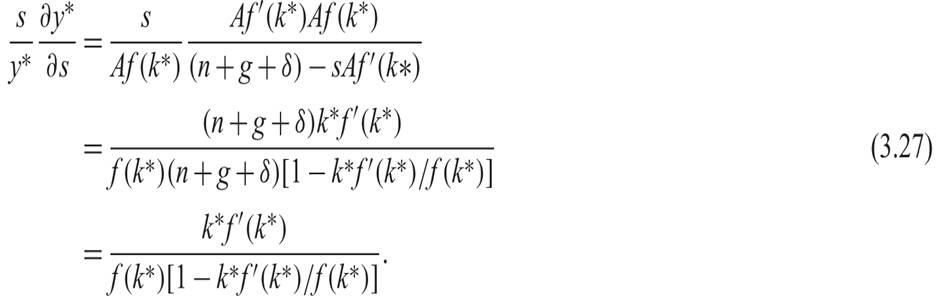

One can show that in the Solow model, the long-run elasticity of output with respect to the savings rate is equal to the ratio of the share of capital to the share of labor in total output.

To prove this, we start from the change in steady state output following a change in the savings rate. This is equal to

where k* is defined by,

Differentiating (3.24) with respect to s, we get

Substituting (3.25) into (3.23) results in

From (3.26) and (3.24), the long-run elasticity of output with respect to the savings rate is given by

Equation (3.27) can be rewritten as

where αK(k*) is the elasticity of total output with respect to capital at the steady state. With competitive markets, factor incomes are equal to their marginal products. In such a case, the elasticity of total output with respect to capital is equal to the ratio of the share of capital to the share of labor in total output. A commonly accepted estimate of the share of capital in total output is about 1/3. Using this estimate, the long-run elasticity of total output with respect to the savings rate is equal to 1/2.

3.4