The q-Theory of Investment

As another application of the methods developed in this chapter, we consider the canonical model of investment under adjustment costs, also known as the q-theory of investment. This problem is not only useful as an application of optimal control techniques, but it is one of the basic models of standard macroeconomic theory.

The economic problem is that of a price-taking firm trying to maximize the present discounted value of its profits. The only twist relative to the problems we have studied so far is that this firm is subject to “adjustment” costs when it changes its capital stock. In particular, let the capital stock of the firm be k (t) and suppose that the firm has access to a production function f (k (t)) that satisfies Assumptions 1 and 2. For simplicity, let us normalize the price of the output of the firm to 1 in terms of the final good at all dates. The firm is subject to adjustment costs captured by the function φ (i), which is strictly increasing, continuously differentiable and strictly convex, and satisfies φ (0) = φ0 (0) = 0. This implies that in addition to the cost of purchasing investment goods (which given the normalization of price is equal to i for an amount of investment i), the firm incurs a cost of adjusting its production structure given by the convex function φ (i). In some models, the adjustment cost is taken to be a function of investment relative to capital, i.e., φ (i/k) instead of φ (i), but this makes no difference for our main focus. We also assume that installed capital depreciates at an exponential rate δ and that the firm maximizes its net present discounted earnings with a discount rate equal to the interest rate r, which is assumed to be constant.

The firm’s problem can be written as

subject to

and k (t) ≥ 0, with k (0) > 0 given.

Clearly, both the objective function and the constraint function are weakly monotone, thus we can apply Theorem 7.14.Notice that φ (˛) does not contribute to capital accumulation; it is simply a cost. Moreover, since φ is strictly convex, it implies that it is not optimal for the firm to make “large” adjustments. Therefore it will act as a force towards a smoother time path of investment.

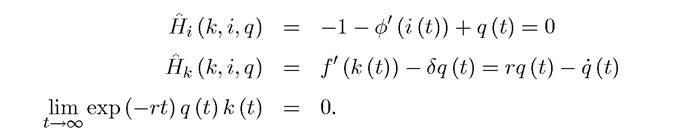

To characterize the optimal investment plan of the firm, let us write the current-value Hamiltonian:

where we used q (t) instead of the familiar μ (t) for the costate variable, for reasons that will be apparent soon.

The necessary conditions for this problem are standard (suppressing the “ë” to denote the optimal values in order to reduce notation):

The first necessary condition implies that

Differentiating this equation with respect to time, we obtain

Substituting this into the second necessary condition, we obtain the following law of motion for investment:

A number of interesting economic features emerge from this equation. First, as φ" (˛) tends to zero, it can be verified that i (t) diverges, meaning that investment jumps to a particular value. In other words, it can be shown that this value is such that the capital stock immediately reaches its state-state value (see Exercise 7.24). This is intuitive. tends to zero,

tends to zero,

φ0 (i) becomes linear.

In this case, adjustment costs simply increase the cost of investment linearly and do not create any need for smoothing. In contrast, when , there will

, there will be a motive for smoothing, i (t) will take a finite value, and investment will adjust slowly. Therefore, as claimed above, adjustment costs lead to a smoother path of investment.

We can now analyze the behavior of investment and capital stock using the differential equations (7.61) and (7.64). First, it can be verified easily that there exists a unique steadystate solution with k > 0. This solution involves a level of capital stock k* for the firm and investment just enough to replenish the depreciated capital, This steady-state level

This steady-state level

293

of capital satisfies the first-order condition (corresponding to the right-hand side of (7.64) being equal to zero):

This first-order condition differs from the standard “modified golden rule” condition, which requires the marginal product of capital to be equal to the interest rate plus the depreciation rate, because an additional cost of having a higher capital stock is that there will have to be more investment to replenish depreciated capital. This is captured by the term φ0 (δk*). Since φ is strictly convex and f is strictly concave and satisfies the Inada conditions (from Assumption 2), there exists a unique value of k* that satisfies this condition.

The analysis of dynamics in this case requires somewhat different ideas than those used in the basic Solow growth model (cf., Theorems 2.4 and 2.5). In particular, instead of global stability in the k-i space, the correct concept is one of saddle-path stability. The reason for this is that instead of an initial value constraint, i (0) is pinned down by a boundary condition at “infinity,” that is, to satisfy the transversality condition,

This implies that in the context of the current theory, with one state and one control variable, we should have a one-dimensional manifold (a curve) along which capital-investment pairs tend towards the steady state.

This manifold is also referred to as the “stable arm”. The initial value of investment, i (0), will then be determined so that the economy starts along this manifold. In fact, if any capital-investment pair (rather than only pairs along this one dimensional manifold) were to lead to the steady state, we would not know how to determine i (0); in other words, there would be an “indeterminacy” of equilibria. Mathematically, rather than requiring all eigenvalues of the linearized system to be negative, what we require now is saddle-path stability, which involves the number of negative eigenvalues to be the same as the number of state variables.This notion of saddle path stability will be central in most of growth models we will study. Let this now make these notions more precise by considering the following generalizations of Theorems 2.4 and 2.5 (see Appendix Chapter B):

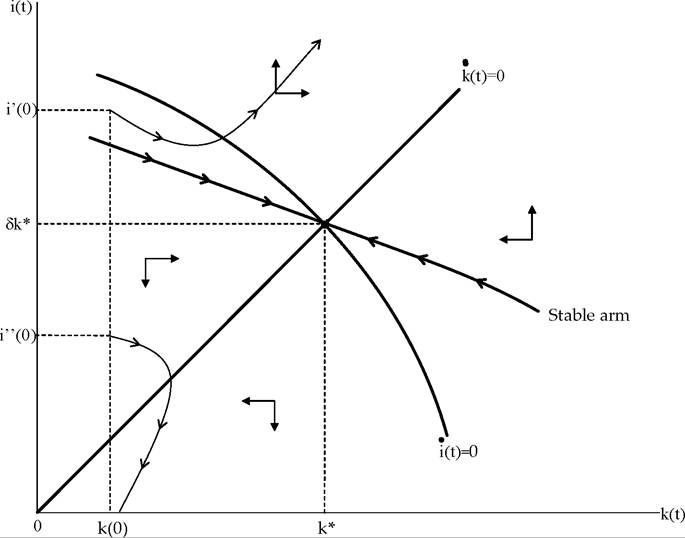

FIGURE 7.1. Dynamics of capital and investment in the q-theory.

Theorem 7.19. Consider the following nonlinear autonomous differential equation (7.66)

Put differently, these two theorems state that when only a subset of the eigenvalues have negative real parts, a lower-dimensional subset of the original space leads to stable solutions. Fortunately, in this context this is exactly what we require, since i (0) should adjust in order to place us on exactly such a lower-dimensional subset of the original space.

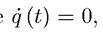

Armed with these theorems, we can now investigate the transitional dynamics in the q-theory of investment. To see that the equilibrium will tend to this steady-state level of capital stock it suffices to plot (7.61) and (7.64) in the k-i space.

This is done in Figure 7.1.295

The curve corresponding to k = 0, (7.61), is upward sloping, since a greater level of capital stock requires more investment to replenish the depreciated capital. When we are above this curve, there is more investment than necessary for replenishment, so that k > 0. When we are below this curve, then k < 0. On the other hand, the curve corresponding to i = 0, (7.64), can be nonmonotonic. Nevertheless, it is straightforward to verify that in the neighborhood of the steady-state it is downward sloping (see Exercise 7.24). When we are to the right of this curve, f' (k) is lower, thus i > 0. When we are to its left, i < 0. The resulting phase diagram, together with the one-dimensional stable manifold, is shown in Figure 7.1 (see again Exercise 7.24 for a different proof).

Starting with an arbitrary level of capital stock, k (0) > 0, the unique optimal solution involves an initial level of investment i (0) > 0, followed by a smooth and monotonic approach to the steady-state investment level of δk*. In particular, it can be shown easily that when k (0) < k*, i (0) > i* and it monotonically decreases towards i* (see Exercise 7.24). This is intuitive. Adjustment costs discourage large values of investment, thus the firm cannot adjust its capital stock to its steady-state level immediately. However, because of diminishing returns, the benefit of increasing the capital stock is greater when the level of capital stock is low. Therefore, at the beginning the firm is willing to incur greater adjustment costs in order to increase its capital stock and i (0) is high. As capital accumulates and k (t) > k (0), the benefit of boosting the capital stock declines and the firm also reduces investment towards the steady-state investment level.

violating the transversality condition. In contrast, if we start with i" (0) < i (0) as the initial level, i (t) would tend to 0 in finite time (as shown by the fact that the trajectories hit the horizontal axis) and k (t) would also tend towards zero (though not reaching it in finite time).

After the time where i (t) = 0, we also have q (t) = 1 and thus q (t) = 0 (from (7.62)). Moreover, by the Inada conditions, as k (t) → 0, f' (k (t)) → ∞. Consequently, after i (t) reaches 0, the necessary condition is necessarily violated. This

is necessarily violated. This proves that the unique optimal path involves investment starting at i (0).

We next turn to the “q-theory” aspects. James Tobin argued that the value of an extra unit of capital to the firm divided by its replacement cost is a measure of the “value of investment to the firm”. In particular, when this ratio is high, the firm would like to invest more. In steady state, the firm will settle where this ratio is 1 or close to 1. In our formulation, the costate variable q (t) measures Tobin’s q. To see this, let us denote the current (maximized) value of the firm when it starts with a capital stock of k (t) by V (k (t)). The same arguments as above imply that

(7.67)

so that q (t) measures exactly by how much one dollar increase in capital will raise the value of the firm.

In steady state, we have so that

so that , which is approximately

, which is approximately

equal to 1 when is small. Nevertheless, out of steady state, q (t) can be significantly greater than this amount, signaling that there is need for greater investments. Therefore, in this model Tobin’s q, or alternatively the costate variable q (t), will play the role of signaling when investment demand is high.

is small. Nevertheless, out of steady state, q (t) can be significantly greater than this amount, signaling that there is need for greater investments. Therefore, in this model Tobin’s q, or alternatively the costate variable q (t), will play the role of signaling when investment demand is high.

The q-theory of investment is one of the workhorse models of macroeconomics and finance, since proxies for Tobin’s q can be constructed using stock market prices and book values of firms. When stock market prices are greater than book values, this corresponds to periods in which the firm in question has a high Tobin’s q—meaning that the value of installed capital is greater than its replacement cost, which appears on the books. Nevertheless, whether this is a good approach in practice is intensely debated, in part because Tobin’s q does not contain all the relevant information when there are irreversibilities or fixed costs of investment, and also perhaps more importantly, what is relevant is the “marginal q,” which corresponds to the marginal increase in value (as suggested by equation (7.67)), whereas we can typically only measure “average q”. The discrepancy between these two concepts can be large.

7.9.