As already discussed, financial contracts contain rules used to sufficiently extract the financial events given the actual and assumed market and counterparty conditions.

There are some contractual rules, however, which may give an additional degree of freedom, and which may change the expected financial events. Think for instance of a loan where a borrower has the option to prepay the loan at any time before the maturity.

Moreover, a counterparty could always decide to terminate the contract and/or default. In this case the expected cash flows will change according to the time and amount of prepayment or default; additionally, other cash flows will rise, e.g., possible fees, recoveries, etc. All these are financial events, which are driven by the behavior analysis element.Behavior is a very special type of risk as it reflects the decisions made by the counterparties. Such decisions are mainly driven by idiosyncratic as well as external factors such as market conditions. In the above mentioned example a counterparty could decide to prepay or default due to unfavorable market conditions, e.g., a loan of high fixed interest rates at the times where the market interest rate is very low. Behavior also refers to strategies, e.g., getting liquidity from selling the financial contracts/instruments. Nevertheless, decisions do not always make economic sense; counterparties may exercise their options by following other people or due to some “rational” behavior which sometimes is against their own interest.1

As already mentioned, behavior risk is one of the main input analysis elements, and thus impacts the value, income and expected liquidity of the financial contracts. In behavior risk analysis we are mainly considering the counterparty idiosyncratic characteristics but also the market-related risk factors. However, it is impossible or impractical to identify those characteristics and factors at individual counterparty and contract levels. On the other hand, counterparties with similar descriptive characteristics tend, in many instances, to behave in a similar manner for certain contract types and market conditions.

Therefore, it is more than reasonable to apply our behavior assumptions at aggregated level.Statistics could provide a good overview of past behaviors and could assist in approximating future assumptions. Thus, historic statistical information plays an important role in behavior risk analysis. Empirical research shows that, under normal conditions, counterparties behave in stable and predictable ways, whereas under stress conditions their behavior can become unexpected, and follow certain uncharted paths. When a critical mass of counterparties collectively follows an unexpected behavior, this can introduce great uncertainties into the financial system. Thus, deterministic and/or stochastic scenarios should be made and applied, to identify and measure the behavior risk. Even though there is no universal function to form

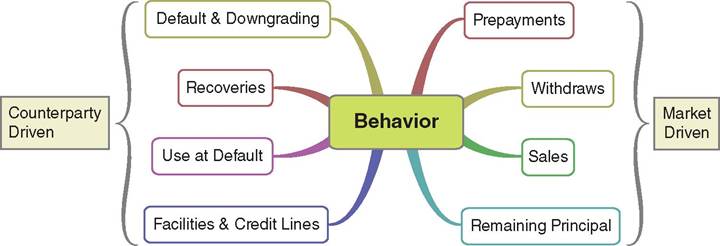

FIGURE 8.1 Classifying the main behavior analysis elements based on market and counterparty credit risk

the behavior element their effect on the cash flows must be clearly calculated. The default and prepayment behavior events, for instance, change future cash flows.

The number of behavior risk elements is not fixed; however we classify them as behavior driven by market risk and counterparty credit risk factors as illustrated in Figure 8.1. In banking financial instruments, typical market risk driven behavior elements are the prepayments of the loans, withdrawals of current and saving accounts, and the use/drawings of principal amount in loan contracts such as the ones used in a project development. Behavior of counterparty credit risks are the use of credit lines/facilities, the decision to default, reflected by the change of default probability, the expected recovery after the default event, and the use of credit lines to avoid the default event. Prepayment, default and downgrading, use at default and recoveries are behavior elements that should also be considered in the instruments provided in marketplace lending.

The pattern of the behavior is discussed in Chapter 5 (5.3.5 Behavior patterns).

8.1