PREPAYMENTS

Prepayment is an option of the obligor counterparty to prepay the remaining principal, partially or fully, before the contractual maturity date. In terms of liquidity, such behavior will cancel out all expected cash flows just after the prepayment option is exercised.

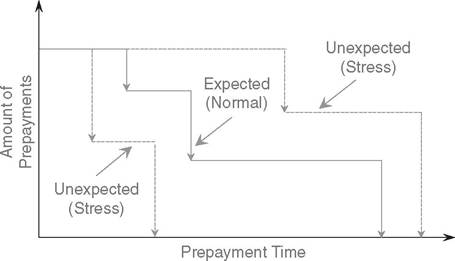

Both exposure and value of the contract will be changed accordingly. To model prepayment, historical data and assumptions can give a good approximation of such behaviors. For instance, as illustrated in Figure 8.2 under stress conditions, counterparties are expected to change the prepayment, e.g., if interest rates deteriorate, counterparties tend to prepay more, and earlier than expected, of the fixed rated contracts and replace them with variable ones and vice versa.The parameters considered in such behaviors are the PITs of prepayment date, the prepayment speed as a percentage that is paid back at each prepayment PIT, the payback value as the decrease in the outstanding notional amount, the valuation rule applied to remaining principal after the prepayment, the fees that may be paid and the payback rule.

Marketplace lending platforms have to communicate to lenders that borrowers might prepay their loans. In fact, prepayment comes with few repercussions for borrowers on most marketplace lending platforms. For example, when a prepayment option is exercised but no

FIGURE 8.2 Pattern that illustrates the prepayment under statistically normal and stress financial risk conditions

charges, such as fees and penalties, are applied. The loser in this equation is the lender who will miss out on the promised interest and will have to look for alternative sources of fixed income. When loans at similar interest rates are abundant, this hardly matters. Lenders can simply select new loans and invest the capital they received prematurely from borrowers in these other loans. However, this may not be the case for an institutional investor with a large portfolio of marketplace loans who has carefully predicted and timed the liquidity in his exposure. When borrowers prepay, these liquidity predictions cease to be valid. Depending on the size of the portfolio, it might also be more complex to find new investments for a large amount of capital. This can be a headache when interest rates have significantly declined in the meantime. In any event, prepaid loans are something that lenders wish to discourage. This is why they should at least consider that borrowers may prepay, and they should adjust their investment strategy accordingly.

8.2

More on the topic PREPAYMENTS:

- UNDERLYING ASSUMPTIONS OF THE ANALYSIS

- Hare C., Neo D. (eds.). Trade Finance: Technology, Innovation and Documentary Credit. Oxford University Press,2021. — 417 p., 2021

- To understand marketplace lending better, we apply a banking risk-management approach to a portfolio of marketplace loans.

- Appendices

- DYSPHAGIA

- Article 15.2 Recent deals signal market’s reopening in the same old style

- HYPERTHERMIA

- Summary and Open Issues

- RASHTRiYA KISHOR SWASTHYA Karyakram (rksk)

- APPENDIX